By Pam Martens and Russ Martens: July 13, 2020 ~

Imagine if every bank customer was greeted this week with a big sign just inside their Chase Bank branch that said this:

Imagine if every bank customer was greeted this week with a big sign just inside their Chase Bank branch that said this:

“Dear Customers: We lost $3.2 billion trading stocks and credit derivatives in the first quarter. We did that using your bank deposits. But don’t worry, that pales in comparison to the $6 billion we lost in 2012 in the London Whale mess.”

JPMorgan Chase is the largest bank in the United States. Each and every week, millions of Americans write out a check on their account at one of the more than 5,000 branches of Chase Bank; or drop into a branch to open a savings account for a grandchild; or to put money into their own retirement account; or to seek financial advice.

Everything looks very crisp, clean, consumer friendly and professional inside that individual bank branch. But there is a frightening picture serially occurring in the unaccountable management of this sprawling financial behemoth.

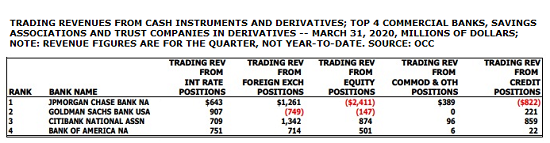

According to the latest quarterly report from the Office of the Comptroller of the Currency (OCC), JPMorgan Chase lost $2.4 billion trading stocks (equities) and $822 million trading credit derivatives, giving it a net loss among all of its trading in cash instruments and derivatives of $940 million. This is not what happened in the whole sprawling trading octopus of JPMorgan Chase, it’s just what happened in the taxpayer-backstopped, federally-insured bank.

If you are new to Wall Street On Parade, you are probably thinking that it is an outrage that a bank could use federally-insured deposits to gamble for the house. And it is an outrage. But if you had been reading our reporting on the Wall Street mega banks for the past decade, you would realize that it is simply one more brick in a giant wall of outrage.

There are so many bricks to choose from in the JPMorgan Chase wall of outrage that it’s hard to know how to prioritize them. But we’ll give it a shot.

For starters, Jamie Dimon was the Chairman and CEO of this bank during the financial crisis when there was an insider whistleblower holding a law license, Alayne Fleischmann, that testified to the U.S. Department of Justice that she had observed “a massive criminal securities fraud” inside the bank involving the bogus mortgages the bank had sold in the billions of dollars to investors. But instead of using that first-hand evidence to prosecute the bank, Obama’s Justice Department under Eric Holder used that information to extract a large fine from the bank with no charges brought.

Dimon is caught on camera on September 26, 2013 strolling into the offices of Eric Holder to personally negotiate the terms of the settlement. Less than two months later, the Justice Department announced the toothless settlement on behalf of itself and other regulators. Holder said this at the time:

“The size and scope of this resolution should send a clear signal that the Justice Department’s financial fraud investigations are far from over. No firm, no matter how profitable, is above the law, and the passage of time is no shield from accountability.”

But there was no accountability at all. Nobody went to jail and Jamie Dimon kept his job as Chairman and CEO.

The Justice Department’s settlement with JPMorgan Chase for what was clearly fraudulent conduct came just eight months after the U.S. Senate’s Permanent Subcommittee on Investigations had released a 300-page report on the bank’s use of depositor money inside its federally-insured bank to gamble in exotic derivatives in London, leading to losses of at least $6.2 billion.

At the time of the London Whale report, Senator Carl Levin was Chair of the Subcommittee. He said this: “Our findings open a window into the hidden world of high stakes derivatives trading by big banks. It exposes a derivatives trading culture at JPMorgan that piled on risk, hid losses, disregarded risk limits, manipulated risk models, dodged oversight, and misinformed the public.”

The late Senator John McCain was Ranking Member of the Subcommittee at the time. He made this statement on the matter: “This case represents another shameful demonstration of a bank engaged in wildly risky behavior. The ‘London Whale’ incident matters to the federal government because the traders at JPMorgan were making risky bets using excess deposits, portions of which were federally insured. These excess deposits should have been used to provide loans for main-street businesses. Instead, JPMorgan used the money to bet on catastrophic risk.”

Once again, federal regulators settled the matter against the bank with fines. Jamie Dimon kept his job.

We broke the story that the woman that Dimon had put in charge of overseeing this sprawling London trading operation, Ina Drew, didn’t even hold a securities license. (See Jamie Dimon’s Top Women and Their Missing Licenses.)

The very next year, 2014, Dimon’s bank was charged with two criminal felony counts for its role in handling the business account of Ponzi schemer Bernie Madoff for decades, looking the other way at glaring red flags of money laundering. Because of evidence uncovered by an independent trustee for a victims’ restitution fund, the Justice Department had little choice but to bring the charges. The bank pleaded guilty to both charges. Jamie Dimon kept his job as Chairman and CEO.

The very next year, 2015, the Justice Department brought another criminal felony charge against the bank, this time for engaging with other banks in rigging foreign exchange markets. The bank pleaded guilty and – of course – Jamie Dimon kept his job as Chairman and CEO.

On September 16 of last year, the Justice Department indicted two current and one former precious metal traders at JPMorgan Chase. As far as anyone on Wall Street can remember, it was the first time a trading desk at a big Wall Street bank was charged with running it as a racketeering enterprise and having its traders charged under the RICO statute, which is typically used to prosecute organized crime.

According to Bloomberg News, the bank itself is now under a criminal probe in the matter, making it at least the fourth criminal probe in the last seven years.

On top of an unprecedented criminal past under the tenure of Jamie Dimon, last November we reported that the bank has the dubious distinction of being called out as the riskiest bank in the U.S. by one of its federal regulators. (See It’s Official: JPMorgan Chase Is the Riskiest Big Bank in the U.S.)

If this sounds more like the description of a bank in a banana republic rather than a U.S. bank holding $1.9 trillion in deposits for average Americans, public pension funds, as well as sophisticated investors, you are correct to be concerned.

Two trial lawyers, Helen Davis Chaitman and Lance Gotthoffer, wrote a book in 2016, JPMadoff: The Unholy Alliance Between America’s Biggest Bank and America’s Biggest Crook, comparing the bank to the Gambino crime family. They wrote:

“In Chapter 4, we compared JPMC to the Gambino crime family to demonstrate the many areas in which these two organizations had the same goals and strategies. In fact, the most significant difference between JPMC and the Gambino Crime Family is the way the government treats them. While Congress made it a national priority to eradicate organized crime, there is an appalling lack of appetite in Washington to decriminalize Wall Street. Congress and the executive branch of the government seem determined to protect Wall Street criminals, which simply assures their proliferation.”

Until tens of millions of Americans personally engage in demanding campaign finance reform, federal government reform, and the complete separation of banks holding deposits from the Wall Street casino banks, we’re all just one step away from the next banking collapse.