By Pam Martens and Russ Martens: November 25, 2019 ~

The National Information Center is a little-known repository of bank data collected by the Federal Reserve. It is part of the Federal Financial Institutions Examination Council (FFIEC), which was created by federal legislation to create uniformity in the examination of U.S. financial institutions by the numerous federal regulators of banks.

Quietly, the National Information Center has done something that has likely made Jamie Dimon hopping mad. Dimon is the Chairman and CEO of JPMorgan Chase who has bragged perpetually in his annual letter to shareholders about how the bank he leads has a “fortress balance sheet.” But now the National Information Center has created a graphic profile of JPMorgan Chase versus its peer banks. The graphics crunch a series of important financial metrics at JPMorgan Chase, showing it to be the riskiest bank in the United States.

The data used to create these graphics come from what is known as the “Systemic Risk Report” or form FR Y-15 that banks have to file with the Federal Reserve. To measure the systemic risk that a particular bank poses to the stability of the U.S. financial system, the data is broken down into five categories of system risk: size, interconnectedness, substitutability, complexity, and cross-jurisdictional activity. Those measurements consist of 12 pieces of financial information that banks have to provide on their Y-15 forms. That data shows that in 7 out of 12 financial metrics, JPMorgan Chase has the riskiest footprint among its peer banks.

One of the 12 financial metrics measures the Intra-Financial System Liabilities of each bank. This shows how much money a particular bank has at risk at other banks by using inputs such as how much of its funds it has on deposit with, or has lent to, other financial institutions; the unused portion of any credit lines it has committed to other financial institutions; and its holdings of debt, equity, commercial paper, etc. of other financial institutions. The idea, obviously, is to understand if another Citigroup or Lehman Brothers were to occur, could it bring your bank down.

JPMorgan Chase looks particularly dicey in this regard. The Y-15 data shows that it has $377.9 billion in Intra-Financial System Liabilities which is more than $100 billion larger than the next two largest banks in this category, Bank of New York Mellon and Citigroup.

Source: National Information Center; Compiled from Federal Reserve Y-15 Financial Data from JPMorgan Chase

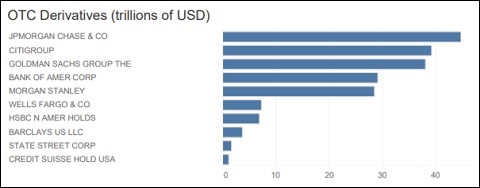

Another scary category is OTC Derivatives. OTC (over-the-counter) means derivatives that are not traded on an exchange and are not being cleared by a central clearing house. In effect, it means a private contract between your bank and some potentially non-credit worthy financial institution. (Recall how the giant life insurer, AIG, blew itself up in 2008 because it was holding tens of billions of dollars in derivative contracts for the biggest banks on Wall Street that it could not make good on. The situation was so dire that the Federal Reserve actually allowed AIG to secretly borrow billions of dollars from its Discount Window, even though it was an insurance company, not a bank. AIG had to be eventually nationalized by the U.S. government for a time during the financial crisis – all because it got involved with Wall Street’s derivatives.)

Among the biggest banks on Wall Street, JPMorgan Chase has the largest exposure to derivatives, with $45.2 trillion exposure, according to the National Information Center graphic. Yes, we said “trillion.” The Office of the Comptroller of the Currency, however, which is the federal regulator of national banks and reports the derivative exposures of the biggest banks on a quarterly basis, shows that as of June 30 of this year, JPMorgan Chase’s notional derivatives (face amount) stood at an even larger $55.7 trillion. (See Table 1 in the Appendix here.) In other words, while JPMorgan Chase is backing away from lending in the repo market, forcing the Federal Reserve to effectively bail out Wall Street’s lack of liquidity in overnight lending, that hasn’t stopped JPMorgan Chase from increasing its systemic risk footprint in other areas.

Source: National Information Center; Compiled from Federal Reserve Y-15 Financial Data from JPMorgan Chase

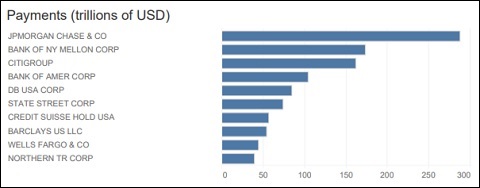

But the scariest data point by far is the graph showing where JPMorgan Chase stands in the “Payments” system of the U.S. banking system. According to its own data submitted on its December 31, 2018 Y-15 filing, it was responsible for $320.65 trillion in payments in the prior four quarters. That’s 95 percent larger than the next largest peer bank in the Payments category, Bank of New York Mellon, which is responsible for $163.23 trillion in payments.

Source: National Information Center, Compiled from Federal Reserve Y-15 Financial Data from JPMorgan Chase

It is perhaps no coincidence that the one thing the federal regulators are not compiling in this breakdown of what constitutes systemic risk to the U.S. financial system is how many criminal activities a bank has been engaged in. On that front, JPMorgan Chase also ranks as the scariest big bank in the United States. It is the only U.S. bank in history to have survived three criminal felony charges, to which it pleaded guilty, while keeping the same Chairman and CEO in place, Jamie Dimon. In September, JPMorgan Chase scored another first in the crime category. As far as anyone on Wall Street can remember, it was the first time a trading desk at a big Wall Street bank was charged with running it as a racketeering enterprise and had its traders charged under the RICO statute, which is typically used to prosecute organized crime.

We suspect the reason that the Federal Reserve does not want to see criminal activity at banks evaluated as a source of systemic risk to the U.S. financial system is because that might suggest that the Federal Reserve should not be wearing three hats simultaneously. It’s currently the U.S. central bank in charge of U.S. monetary policy while it is also the primary regulator to the most dangerous and largest bank holding companies — while it is also the lender-of-last resort that can magically conjure up hundreds of billions of dollars each week to bail out the New York mega banks it has negligently supervised.

Editor’s Note: The bar graphs appear to be slightly off from the actual financial data reported by JPMorgan Chase on its December 31, 2018 Y-15. We believe that is because the bar graphs were compiled from more current Y-15 data.