By Pam Martens and Russ Martens: May 18, 2023 ~

Martin Gruenberg, Chair, Federal Deposit Insurance Corporation (FDIC)

On Wednesday, March 8 of this year, the holding company for the federally-insured Silvergate Bank announced it was winding down the bank. It had little choice but to do so. It was experiencing a bank run and had incinerated its reputation by focusing on deposits from crypto companies, including those majority-owned by indicted crypto kingpin, Sam Bankman-Fried.

According to testimony from the Chairman of the Federal Deposit Insurance Corporation (FDIC), Martin Gruenberg, before the Senate Banking Committee on March 28, “in the fourth quarter of 2022, Silvergate Bank experienced an outflow of deposits from digital asset customers that, combined with the FTX deposits, resulted in a 68 percent loss in deposits – from $11.9 billion in deposits to $3.8 billion.”

Silvergate Bank’s primary regulator was the San Francisco Fed.

Two days later, on Friday, March 10, Silicon Valley Bank was put into receivership at the FDIC following an unprecedented bank run that saw $42 billion in deposits leave the bank on just the day of March 9, with another $100 billion in deposits queued up to leave the next day – which would have represented the vast majority of its deposits taking flight in 48 hours. That testimony was delivered to the Senate Banking Committee on March 28 by the Vice President for Supervision at the Fed, Michael Barr.

Silicon Valley Bank’s primary regulator was also the San Francisco Fed.

Two more bank failures followed in short order: Signature Bank on March 12 and First Republic Bank on May 1. Both were experiencing bank runs as a result of a loss of confidence by their customers. The primary regulator of both was the FDIC.

First Republic Bank, Silicon Valley Bank, and Signature Bank were the second, third and fourth largest bank failures in U.S. history, respectively. The largest failure was Washington Mutual during the financial crisis of 2008. JPMorgan Chase, officially the riskiest U.S. bank, was allowed by its regulators to take over Washington Mutual in 2008 and First Republic Bank on May 1 of this year.

Senator Elizabeth Warren at May 17, 2023 Hearing on Fed Accountability

Yesterday, the Senate Banking Subcommittee on Economic Policy, which is chaired by Senator Elizabeth Warren (D-MA), held a hearing on the lack of accountability at the Fed and proposals to reform its structure. Senator Warren said this in her opening remarks:

“The rapid collapse of three banks — Silicon Valley Bank, Signature Bank and First Republic Bank — was a shock. These three bank failures together put more assets at risk than the 25 bank failures in the 2008 crash.

“Silicon Valley Bank’s failure was another symptom of what has become a predictable string of failures in the governance of the Federal Reserve. SVB’s collapse and other bank failures it triggered forced the FDIC, the Treasury Department, and other regulators to rush to the rescue to avoid implosion of our banking system. So far, the FDIC Insurance Fund has suffered billions of dollars of losses, and, as a result of the bailouts, America’s biggest too-big-to-fail bank just got $200 billion bigger.” (Senator Warren is referring to JPMorgan Chase’s takeover of First Republic Bank.)

During yesterday’s hearing, the Fed’s support of 2018 legislation that resulted in the rollback of prudential regulation on banks with assets under $250 billion was examined as contributing to the recent bank collapses. In written testimony, Dr. Peter Conti-Brown, Associate Professor of Financial Regulation, Associate Professor of Legal Studies and Business Ethics at The Wharton School of the University of Pennsylvania, offered this analysis:

“In 2018, after many months of debate, President Trump signed the Economic Growth, Regulatory Relief, and Consumer Protection Act. In an era of omnibus bills, often hundreds or thousands of pages long, one of the most impressive feats of the EGRRACPA (or S. 2155, as it is more commonly known), is its length: the entire bill is just 75 pages long. The part that is relevant to the present banking crisis, Title IV of that act, is just five pages long. In those five pages, entitled ‘Tailoring Regulations for Certain Bank Holding Companies,’ Congress changed the $50 billion [asset] threshold [for prudential regulation of banks] to $250 billion [in assets]…

“Over the last two months, three of the twenty banks within that band of $100 billion to $250 billion have failed. (In the somewhat absurd vernacular of banking, we call these banks ‘regional banks.’). We do not know how many of the remaining seventeen would have failed but for the emergency declarations and concomitant liquidity support that the federal government’s extraordinary actions facilitated thereafter.

“Thus, while the focus is often on Silicon Valley Bank, the fact is that we have had an intolerable failure of a market segment – when 15% of banks fail within the very class that Congress deregulated in 2018, we have enough smoke to inquire about the presence of fire.”

Another key focus of the hearing was on what Senator Warren calls a “culture of corruption at the Fed.” Over the past two years, under Fed Chair Jerome Powell, the Fed has experienced a string of scandals, including the unprecedented trading scandal by Fed officials, where they were trading in their own brokerage accounts in stocks and other instruments while sitting on confidential market moving information at the Fed.

Powell referred the trading scandal investigation to the Inspector General of the Federal Reserve, Mark Bialek, on October 4, 2021. It took Bialek just nine months to clear Powell and former Fed Vice Chair Richard Clarida of violating “the laws, rules, regulations, or policies” of the Fed. Bialek has remained mum for the past 19 months on the biggest suspect in the trading scandal, former Dallas Fed President Robert Kaplan. (See our reports: Robert Kaplan Was Trading Like a Hedge Fund Kingpin for Five Years while President of the Dallas Fed; a Dozen Legal Safeguards Failed to Stop Him and Dallas Fed President Kaplan Was Making Bold, Market-Moving Statements to Media During 2020 Crisis; the Same Year He Traded Tens of Millions of Dollars in Stocks and S&P 500 Futures.)

Kaplan apparently feels he has nothing to fear from Bialek. Kaplan appeared on Bloomberg TV on May 3, actually giving advice to the Fed on monetary policy.

Mark Bialek, Inspector General, Federal Reserve Board

Under questioning from Senator Warren, Bialek revealed that his salary as Inspector General is $377,800. Warren said that this is the highest salary for any employee of the Federal Reserve Board. It is not higher, however, than what Presidents of the 12 privately-owned Federal Reserve regional banks make. For example, John Williams, the President of the New York Fed – where the Federal Reserve Board serially outsources its bailouts of Wall Street’s mega banks – was making $506,300 in 2020 according to the Fed’s 2020 Annual Report. Williams got a bump up in salary to $513,400 according to the Fed’s 2021 Annual Report. (See Table G.12 at this link.) The President of the United States and Commander in Chief, who is elected by the people, makes $400,000.

Senator Warren and Senator Rick Scott (R-FL) suggested that perhaps Bialek is getting this high salary as an incentive to perpetually wear a blindfold about wrongdoing at the Fed. Scott said this during his questioning of Bialek:

Senator Rick Scott at Senate Hearing May 17, 2023

“There’s 23,000 people I think that work at the Federal Reserve. There’s not a report you’ve done since 2011 that you know of any person that’s been fired; there’s nobody on the Board that’s ever done anything wrong; we don’t have any information – good information – on what happened on these stock trades; and you think that we should be happy that we don’t have an independent, presidentially-appointed Inspector General. This doesn’t make any sense. And it [the Federal Reserve] has a balance sheet of $8.6 trillion…Name another agency that has that big a balance sheet in the federal government.”

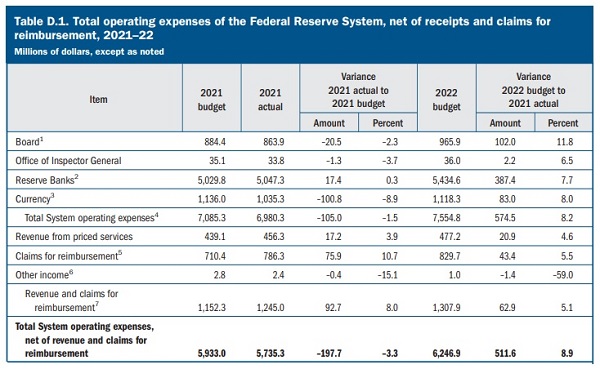

The Fed has a balance sheet of $8.6 trillion, which has resulted from its serial Quantitative Easing (QE) programs where it buys up trillions of dollars of government-backed debt securities, creating demand that would not otherwise exist, in order to drive down interest rates to prop up an economy crippled by serial bank crises.

While the Fed has a balance sheet of $8.6 trillion, it actually has an expense budget of $6.2 billion. (See Table D.1 below from the Fed’s 2021 Annual Report. Notes for the chart are available in the 2021 Annual Report.)

That $6.2 billion budget (combined for both the 12 regional banks and the Fed Board of Governors) includes the tiny amount of $36 million to run the Office of Inspector General that is expected to police the activities of 23,000 people.

Bialek testified at yesterday’s hearing that he has a total staff of 130 people to investigate wrongdoing at the Fed. The Fed’s 2022 budget is offering to let him hire three more people.

There is no better insight into the culture of corruption at the Fed than the 2018 tome by one of its own former bank examiners, Carmen Segarra. Her book, Noncompliant: A Lone Whistleblower Exposes the Giants of Wall Street, describes the culture inside the largest of the Fed’s regional banks — the New York Fed – as follows:

“…nothing I had seen during my decade of legal work had prepared me for what I witnessed in just a few short months at the New York Fed.

“In those months I discovered a disorienting world full of hidden clues, where people said one thing but meant another. Beneath the public face of the Fed laid a web of incompetence, corruption, rampant mismanagement, secrets, and lies. In the ‘fake work’ culture of the Fed, where supervision was a job title, not a job, the most important thing was to control the process to serve the ultimate master. The New York Fed was not simply failing to stop the banks; it was actually enabling their bad behavior.”