By Pam Martens and Russ Martens: June 26, 2024 ~

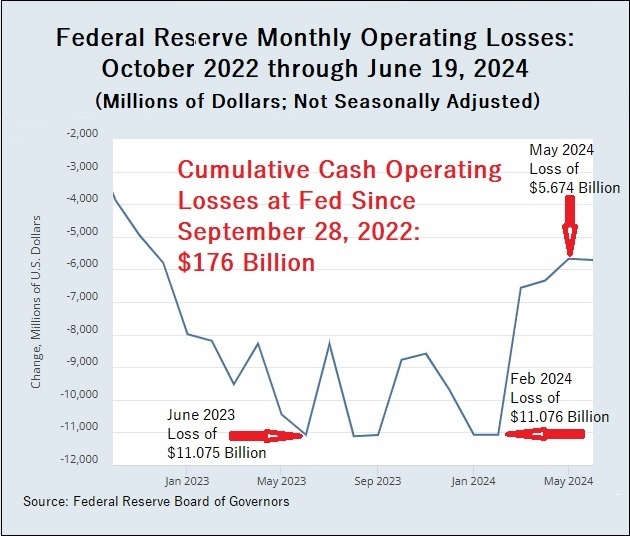

According to Federal Reserve data, for the first time in its history, the Fed has been losing money on a consistent monthly basis since September 28, 2022. As of the last reporting date of June 19, 2024, those losses add up to a cumulative $176 billion. As the chart above using Fed data shows, the losses thus far in 2024 have ranged from a monthly high of $11.076 billion in February to a low of $5.674 billion in May.

These losses are separate and distinct from the unrealized losses the Fed is experiencing on the debt securities it holds on its balance sheet. It does not mark those losses to market since it intends to hold the securities to maturity and their principal is guaranteed at maturity by the U.S. government.

The losses shown in the above chart are actual cash operating losses that result from the fact that the Fed is earning significantly less interest on its debt securities than the high rates of interest the Fed is paying out to depository banks on their reserves held at the Fed; to mutual funds on its reverse repo operations; and in dividend payments to the banks that are shareowners of the 12 regional Fed banks.

Interest on Reserve Balances (IORB): 5.40 Percent

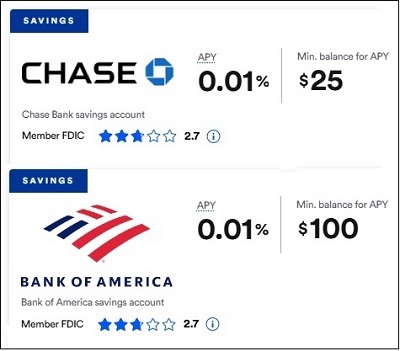

Since July 27 of last year, or one month shy of a year, the Fed has been paying 5.40 percent interest on reserve balances held by banks at the Fed. A significant part of that generous payout has been going to megabanks like JPMorgan Chase and Bank of America. The graphic below, taken from BankRate.com this morning, shows that these megabanks aren’t passing along that generosity to their customers’ savings accounts, since those savings accounts continue to pay the preposterously low rate of 0.01 percent interest, despite 11 rate hikes by the Fed since 2022.

Interest Rate Paid on Savings Accounts, as Shown at BankRate.com on June 26, 2024

A detail that goes missing in mainstream media reports on this generous payout by the Fed is that the Fed and banking system were able to survive for 95 years without the Fed paying any interest on bank reserves. The Fed began paying interest on reserves at a time when the megabanks on Wall Street were in the process of imploding during their self-inflicted financial crisis of 2008 and needed every handout they could conjure up from the Fed. The Fed explains the origination of this policy as follows on one of its website pages from 2008:

“The Financial Services Regulatory Relief Act of 2006 originally authorized the Federal Reserve to begin paying interest on balances held by or on behalf of depository institutions beginning October 1, 2011. The recently enacted Emergency Economic Stabilization Act of 2008 accelerated the effective date to October 1, 2008.”

At the time Congress was pressured into passing this legislation by Wall Street sycophants, it was unaware that the Fed would be conducting three years of secret backroom bailout programs (2007-2010) that would eventually tally up to a cumulative $29 trillion, according to a detailed analysis by the Levy Economics Institute using data the Fed was eventually forced to release.

Reverse Repurchase (Repo) Agreement Operations (RRPs): 5.30 Percent

In addition to paying out 5.40 percent interest on bank reserve balances, the Fed has been paying the hefty rate of 5.30 percent on its reverse repo operations since July 28, 2023. (To track the interest rate the Fed has paid on its reverse repos, put your cursor on any point on the graph linked here.)

Dividend Rate to Bank Shareholders of Federal Reserve Regional Banks: 6 Percent

The highest interest rate of all paid by the Fed is the 6 percent dividend that the Fed pays to the member shareholder banks that own the 12 regional Fed banks. If those banks have assets of $10 billion or less, they receive the 6 percent dividend. Shareholder banks with assets larger than $10 billion receive a dividend which is the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment. How long has the 6 percent dividend rate been in effect? Since the creation of the Fed in 1913. In other words, during busts and bailouts, when the Fed has also been shoveling trillions of dollars in secret loans to its member banks, that 6 percent dividend has been protected.

Think Tank Fallout

In January, two researchers, Paul Kupiec and Alex Pollock, put the cash operating losses at the Fed into broader perspective with a detailed report published at the think tank, American Enterprise Institute (AEI). The researchers wrote:

“Notwithstanding the claims made by current and former Federal Reserve officials, the Fed’s cash operating losses and unrealized interest rate losses have already changed the way the Fed conducts monetary policy. In the past, when the Fed wanted to raise rates or shrink member bank reserve balances, it would sell SOMA [System Open Market Account] securities. But today, with the market value of its SOMA securities approximately $1 trillion less than their book value, selling these securities would immediately turn huge unrealized mark-to-market losses into actual cash losses. To avoid reporting such embarrassing losses, the Fed has committed to hold these securities until they mature to ‘avoid’ a loss, thus constraining its monetary policy options.

“The Fed’s official plan is to shrink the size of its balance sheet by letting its SOMA securities mature over time. But if interest rates stay elevated, the Fed’s unrealized market value losses will systematically turn into cash operating losses because the Fed will keep paying more to finance its securities than the yield it earns on SOMA securities. FRBs’ [Federal Reserve Banks’] operating losses could continue for a long time.”

Kupiec and Pollock further suggest that the Fed is engaged in a dangerous confidence game:

“As long as the public and financial market participants retain confidence in the FRB’s unsecured deposits, FRBs [Federal Reserve Banks] can continue to pay banks billions in interest and dividend payments while operating at a loss, deeply technically insolvent, and with asset shortfalls. Aided by an implicit guarantee, taxpayers will bear the burden of accumulating Federal Reserve losses that are hidden by Federal Reserve accounting policies and not included in reported government deficit statistics.”

For how the U.S. taxpayer is on the hook for the Fed’s losses, see our May 2020 report: Taxpayers Are on the Hook for 98 Percent of the Fed’s $6.98 Trillion Balance Sheet. (As of June 19 of this year, the Fed’s balance sheet was $7.3 trillion.)