By Pam Martens and Russ Martens: August 11, 2020 ~

Randal Quarles, Vice Chairman for Supervision, Federal Reserve, Testifying before the Senate Banking Committee on May 12, 2020

On January 31 of this year, researchers for the Federal Reserve released a study that showed that the largest banks operating in the U.S. have been gaming their stress test results by intentionally dropping their exposure to over-the-counter derivatives in the fourth quarter. The fourth quarter data is the information used by the Federal Reserve to determine surcharges on capital for Global Systemically Important Banks, or G-SIBs.

The report, “How Do U.S. Global Systemically Important Banks Lower Their Capital Surcharges?,” was written by Jared Berry, Akber Khan, and Marcelo Rezende.

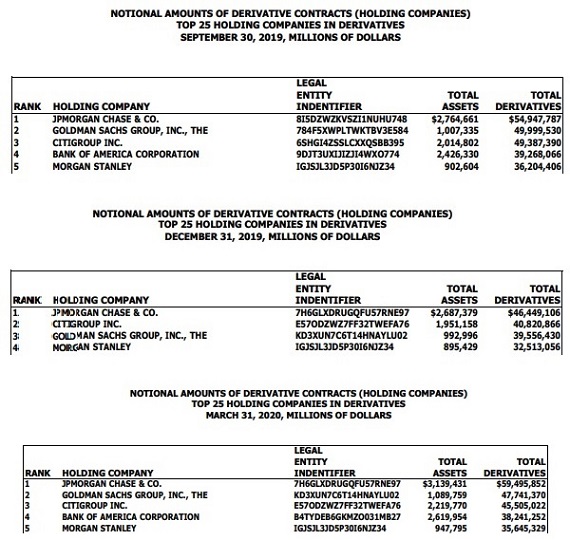

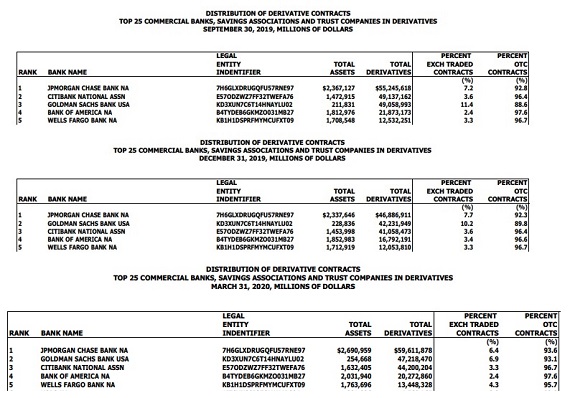

We decided to evaluate this claim for ourselves, using the quarterly derivative reports provided by the Office of the Comptroller of the Currency (OCC), the regulator of national banks. The data was appalling. The largest Wall Street banks not only dropped their level of derivatives by trillions of dollars in the fourth quarter, but they restored those derivatives by the end of the following first quarter. (See first OCC chart below which shows the largest of the top 25 banks by derivative exposure.)

In the case of JPMorgan Chase, it dropped its total derivatives from $55 trillion notional (face amount) in the third quarter to $46.9 trillion in the fourth quarter of 2019, a decline of $8 trillion in one quarter or 15 percent. But by the end of the first quarter of 2020, JPMorgan had pushed those derivatives back up to $59.6 trillion.

The Federal Reserve seems to be accepting this behavior from JPMorgan Chase as a legitimate means of reducing its capital requirements. Yesterday, the Federal Reserve announced the new capital requirements for the largest, Global Systemically Important Banks, or G-SIBs. We fully expected JPMorgan Chase to be slapped with the highest capital requirement since its Systemic Risk Report last year showed it to be the riskiest bank in the U.S. and, clearly, based on the above research that appears on the Fed’s own website, it’s aware of JPMorgan’s “window dressing,” the term used by its own researchers.

But instead of JPMorgan Chase getting slapped with the highest Common Equity Tier 1 (CET1) capital requirement of all 34 banks that underwent the stress test, it was given a relatively tame 11.3 percent CET1. The banks hit with the highest CET1 capital requirements were Goldman Sachs at 13.7 percent and Morgan Stanley at 13.4 percent. (See the Fed’s full chart of capital requirements here.)

Morgan Stanley does not show up on the first OCC chart below because it holds its huge derivatives book at its bank holding company, rather than at its federally-insured commercial banks. The second OCC chart below suggests that Morgan Stanley was also window-dressing its derivatives book, dropping it from $36.2 trillion in the third quarter of 2019 to $32.5 trillion in the fourth quarter; then back to $35.6 trillion in the first quarter of 2020.

Goldman Sachs and Morgan Stanley came away with a higher CET1 capital requirement than even Deutsche Bank’s U.S. entity, DB USA, which was assigned a CET1 capital requirement of 12.3 percent. That’s really saying something. Deutsche Bank has lost money in four of the last five years, including a whopping $5.8 billion last year. Its stock price has evaporated 90 percent of its value since 2007 and it has been repeatedly hit with large fines by regulators for money laundering.

All of this is just further evidence that Congress needs to take away the supervisory powers over banks from the Federal Reserve; strip it of its ability to bail them out; and restrict the Fed to setting monetary policy. Those restrictions can’t arrive soon enough.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~