By Pam Martens and Russ Martens: April 23, 2020 ~

(This article has been updated from one that originally ran in 2012. Please consider emailing it to friends and family members who have given up hope on their ability to create change in America.)

~~~

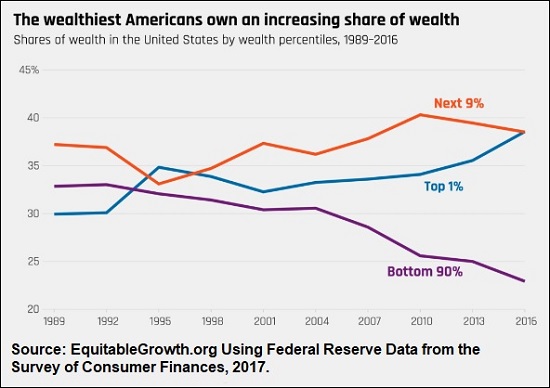

Income Inequality Graph from Robert Reich’s Film, “Inequality for All”

The late 1920s and the early 2000s had two things in common. There was an unprecedented level of wealth and income inequality in the United States and there was no federal legislation to prevent giant Wall Street trading houses from owning deposit-taking banks filled with the savings of moms and pops across America. In both eras, those Wall Street trading houses used bank deposits to make wild bets in risky markets and pay themselves obscene amounts of money.

The 1920s wild west on Wall Street ended in a staggering stock market crash from 1929 to 1932 that rendered thousands of banks insolvent and shut down. At that time, there was no federal insurance on bank deposits so millions of Americans lost all of their savings or received only pennies on the dollar.

The epic Wall Street crash of 2008, the worst since 1929, was not accompanied by moms and pops losing one cent in their bank deposits because the banks had become federally-insured in 1933. But it did require a secret $29 trillion bailout of those banks by the Federal Reserve which has, to this day, grotesquely distorted the U.S. banking system along with the structure of Wall Street.

President Franklin Delano Roosevelt Signing the Glass-Steagall Act on June 16, 1933

The U.S. Senate Banking Committee of the earlier era had guts. They held three years of intense hearings that made a deep, forensic examination of the structure of banking and Wall Street and found that it could never be allowed to combine again. In 1933, Congress passed the Glass-Steagall Act (also known as the Banking Act of 1933) which created federal deposit insurance for the first time while simultaneously outlawing Wall Street trading houses from combining with banks holding federally-insured deposits. That legislation prevented another Wall Street crash from taking down the U.S. economy for the next 66 years.

President Bill Clinton Laughs It Up as He Signs the Repeal of the Glass-Steagall Act, November 12, 1999

In 1999, a big Wall Street trading house, Citigroup, bullied and lobbied and got the Glass-Steagall Act repealed during the Bill Clinton administration. Just nine years later, the Wall Street “universal banks” crashed and took down the U.S. economy. The nation has had 2 percent or less GDP growth ever since along with the greatest wealth inequality since 1928.

Tragically, unlike the Senate of the early 1930s, after the 2008 Wall Street crash, Congress did little intrinsic examination of the structure of Wall Street. The rigged trading, the Dark Pools, the derivatives casinos, the Credit Default Swaps, the Collateralized Debt Obligations, the pay-to-play credit ratings on toxic debt – all of that was left in place under the legislation that resulted in 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act.

And most egregious of all, Dodd-Frank did not separate Wall Street trading houses from federally-insured banking – thus leaving in place the inevitability of more crashes and more trillions in bailouts for Wall Street. That’s where we find ourselves again today.

Writing in his book, “The Worldly Philosophers,” Robert Heilbroner explained the situation leading up to the Great Depression of the 1930s:

“The national flood of income was indubitably imposing in its bulk, but when one followed its course into its millions of terminal rivulets, it was apparent that the nation as a whole benefited very unevenly from its flow. Some 24,000 families at the apex of the social pyramid received a stream of income three times as large as 6 million families squashed at the bottom — the average income of the fortunate families was 630 times the average income of the families at the base…And then there was the fact that the average American had used his prosperity in a suicidal way; he had mortgaged himself up to his neck, had extended his resources dangerously under the temptation of installment buying, and then had ensured his fate by eagerly buying fantastic quantities of stock – some 300 million shares, it is estimated – not outright, but on margin, that is, on borrowed money.”

Both then and now Wall Street had ceased to be a prudent allocator of capital to worthy enterprises and had become an institutionalized wealth transfer system to the top 1 percent.

The January 21, 2010 Supreme Court decision to allow corporations to have staggering financial influence in our elections (Citizens United v. Federal Election Commission) should send a bone chilling message. Help is not on the way. The end game of this massive wealth concentration is economic misery for the 99 percent and multiple generations who will look back on us as their feckless ancestors who couldn’t stop the Wall Street greed machine from destroying a 244-year old democracy.

Below we offer ten ideas to get started on the first course of taming the Wall Street beast.

(1) Shorten Your Home Mortgage: Former Supreme Court Justice Louis Brandeis summed it up: “We can have democracy in this country, or we can have great wealth concentrated in the hands of a few, but we can’t have both.” The Wall Street beast is thriving on interest on our debt and using it to hire lobbyists and fund politicians who will work for their interests, not ours.

Seek your accountant and/or financial advisor’s advice about converting your 30- year mortgage to a 15-year to move wealth from the bank’s shareholders’ pockets to yours. Rates have never been more favorable for such a move. Typically, over the life of the loan, you will save tens of thousands of dollars of interest. You can look at the savings for your specific situation by clicking on the mortgage calculator at www.bankrate.com. (We are not endorsing any of the bank loans offered at this site since we haven’t done any research in that area. We’re just suggesting the use of the mortgage calculator.)

Talk to your adult children before they buy a home about the interest differential between a 30-year and 15-year mortgage over the life of the loan. Show them how to use the mortgage calculator.

If at all possible, get your home mortgage from your local credit union or a local community bank so that you are supporting your local economy.

(2) Think Local: Consider moving money as it becomes liquid out of the big Wall Street banks that have an iron grip on your Congress and moving it into FDIC insured accounts at your community bank (being careful not to exceed the insurance limits). Again, you should consult with your accountant and/or financial advisor. This will also help provide loans to local businesses and residential housing in your area.

(3) Start a Business: Be proactive. Start a business. Do well by doing good: what products or services can you provide that a struggling consumer wants and can afford. (Ideas might include: debt counseling, low cost child care, home staging services to help with faster resales.)

(4) Invest Wisely: Get smart with your 401(k). Investing the bulk of your money in the S&P 500 is simply feeding the beast – the beast that’s using your cheap capital to hire lobbyists, create PACs and separate you from representative government. Some 401(k) plans allow you to roll over 50 percent or more to your own IRA after reaching a certain age. Call your benefits office and find out what your options are. Speak to your accountant and/or financial advisor before making any move. You may also want to consider opening an IRA at a community bank and buying FDIC insured CDs as an alternative to putting more funds in the 401(k). Always ladder maturities on CDs so that you are never locked in to one interest rate environment.

(5) Check Out Credit Union Membership: Do you have a family member that belongs to a Credit Union? Chances are they can get you an account there. Some credit unions have opened up their membership to anyone in their local area. If you need to use a credit card, try to get one through the credit union at a reasonable rate and then cut up any high-rate card. It’s an outrage that some of the Wall Street banks getting a taxpayer bailout for the second time in 12 years are still charging struggling Americans upwards of 17 percent on their credit cards.

(6) Don’t Use Credit Cards from Corporations That Abuse You: All of the following have one thing in common: Home Depot, Exxon Mobil, Shell, Macy’s, Sears, Zales. At some point, they have all extended credit to their customers on a Citigroup (a/k/a Citibank) credit card. Millions of customers are helping to prop up Citigroup and its serial history of taxpayer bailouts and crimes by using these cards.

(7) Brand Attacks: Chances are high that your local store owners don’t have a PAC and lobbyists on K Street working against your interests? Reward them with your business and starve the biggest, anti-consumer corporations until they get the message: if you want me to honor your brand, honor my right to representative government.

(8) Return the Courts to Workers: Many of the largest corporations force workers to sign away their rights to the nation’s courts as a condition of employment. It’s called mandatory arbitration and it’s an unfair process that is rigged to favor the corporation. If you interview for a new job, ask if the company has such a policy and walk away if they do. (See Judicial Apartheid: Wall Street’s Kangaroo Courts: Part I and Part II.)

(9) Complain Loudly: Call your Senators and House Representative and demand the restoration of the Glass-Steagall Act. Ask your family members to do the same. Write a Letter to the Editor to your local newspaper explaining why Glass-Steagall is so important to the economic future of America. Stage a protest in front of the local office of your Senator as soon as the need to practice social distancing passes.

(10) Run for Office: If we want to take back our democracy, we’ll need a front row seat. The political office you run for can be local, state or federal – but good people of good conscience must engage in politics to get a different outcome from the faux democracy that currently exists.