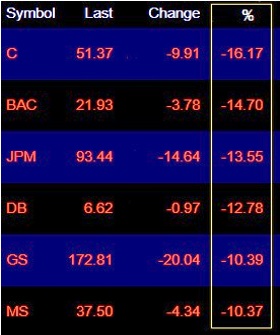

Wall Street Banks, Closing Prices on Monday, March 9, 2020

By Pam Martens and Russ Martens: March 10, 2020 ~

President Donald Trump is bringing a pea shooter to a gunfight. If you look carefully at the charts on this page from yesterday’s trading bloodbath, it’s clear that there is a deep financial crisis playing out. The idea that this can be remedied with a payroll tax cut is the stuff of tooth fairies.

And this crisis didn’t begin with the coronavirus. Headlines about the virus did not start appearing in the U.S. until January of this year. But the Federal Reserve began making hundreds of billions of dollars each week in cheap loans to Wall Street’s banks on September 17, 2019 — the first time it had done this since the 2008 financial crisis. You can earmark September 17, 2019 as the actual date that this Financial Crisis II got underway.

All of the toothless financial reforms of the Dodd-Frank legislation of 2010, together with the rollback of reforms since then, are now coming home to roost — as it was inevitable that they would.

Federal regulators may have their head in the sand about the heavy interlocking relationship between the Wall Street banks and insurance companies that turns into systemic contagion during a financial crisis, but the markets left no doubt about that yesterday. Every major Wall Street bank fell by double digits yesterday as did the insurance companies that are counterparties to Wall Street’s derivative trades.

To give you a snapshot idea of just how grave the situation was yesterday, JPMorgan Chase, the largest federally-insured bank in the U.S. which also holds tens of trillions of dollars of derivatives, fell by a larger percentage yesterday than on September 15, 2008 – the day that Lehman Brothers filed bankruptcy at the height of the 2008 financial crisis. JPMorgan Chase fell 13.55 percent yesterday versus just 10.13 percent on September 15, 2008.

Citigroup led the declines among the mega Wall Street banks yesterday with a stunning loss of 16.17 percent. This is the same bank that received the largest government bailout in global banking history in 2008. Why it was even resuscitated by the government in 2008 remains a nagging question and there would be political upheaval if a repeat performance was suggested. Bank of America, parent of the sprawling retail brokerage firm, Merrill Lynch, declined by 14.70 percent while Deutsche Bank, which has a heavy derivatives footprint on Wall Street, shed 12.78 percent – erasing equity capital it desperately needs right now to stay afloat. Goldman Sachs and Morgan Stanley, which have the ability to trade in their own Dark Pools to protect their share price, closed down 10.39 percent and 10.37 percent, respectively.

Among the insurers with derivative exposure to Wall Street, Lincoln National (LNC) led the declines losing 16.82 percent. It is now down by 47 percent in less than a month. MetLife (MET), which sued the government to get removed from the SIFI list (Systemically Important Financial Institution), certainly appeared to be a SIFI yesterday: it lost 16.64 percent and traded as part of the mega bank/insurer derivatives herd. Prudential Financial (PRU), Ameriprise Financial (AMP), and AIG also experienced deep double-digit losses. Not to put too fine a point on it, but AIG received a $185 billion bailout by the government in the 2008 financial crash. It’s not likely there is going to be the political will for a replay of that either – especially given President Trump’s large libertarian voter base that doesn’t believe in government handouts.

Losses in Insurance Stocks, Monday, March 9, 2020

As we previously reported in April 2016:

AIG received a taxpayer backstop of $185 billion and had to be taken over [temporarily] by the Federal government. But the bailout of AIG was in reality a backdoor bailout of the biggest Wall Street banks and their foreign big bank kin who had used AIG as a counterparty on their casino-like derivative bets and for securities loans that AIG could not make good on.

It was eventually revealed that major Wall Street banks, foreign banks and hedge funds received more than half of AIG’s bailout money ($93.2 billion). Public pressure eventually forced AIG to release a chart of these payments, but the chart showed just a narrow window of disbursements from September to December 2008. How vast the full total of payments were to the big banks is yet to see the light of day.

The chart shows that Goldman Sachs received $12.9 billion of the funds; Societe Generale received $11.9 billion; Merrill Lynch and its U.S. banking parent, Bank of America, received a combined $11.5 billion; the British bank, Barclays, received $8.5 billion; Citigroup got another backdoor bailout of $2.3 billion from AIG, to name just a few of the big banks.

Today, Wall Street banks also have heavy exposure to the debt of energy-related companies and some of those traded like basket cases yesterday. Two oil companies, ExxonMobil and Chevron, are in the Dow Jones Industrial Average and helped to drag it down yesterday. ExxonMobil (XOM) lost 12.22 percent while Chevron (CVX) shed 15.37 percent. But that was a walk in the park compared to the devastation to other energy names: Occidental Petroleum (OXY) lost a stunning 52.01 percent while Apache Corp. (APA) gave up 53.86 percent. Marathon Oil (MRO) sold off by 46.85 percent while Halliburton was down 37.64 percent by the closing bell.

Energy Related Companies Experience Huge Losses on Monday, March 9, 2020

It’s highly likely that we’re going to be hearing about a lot more than payroll tax cuts in the coming days.