By Pam Martens and Russ Martens: March 27, 2020 ~

The New York Fed supervises four of the most dangerous banks in America: Citigroup, JPMorgan Chase, Goldman Sachs and Morgan Stanley. That opinion is not just ours but is documented by data from federal agencies. All four of these banks own federally-insured commercial banks that are backstopped by the U.S. taxpayer while also gambling in the stock market through their own Dark Pools and in trillions of dollars of derivatives.

All four of these banks received tens of billions of dollars in bailout money during the 2007-2010 financial crash, which was brought on by their greed and corrupt activities in the derivatives and subprime market. Citigroup’s losses were of such magnitude that it became insolvent, turned into a 99 cent stock, and yet secretly received the largest bailout in global banking history from the same regulator who had allowed it to become a derivatives fireworks factory and blow up: the New York Fed.

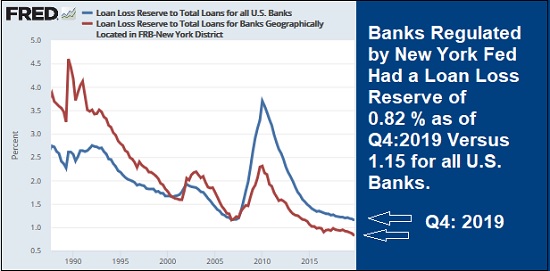

Using data and graphing capability from the Federal Reserve Bank of St. Louis, we compiled the above chart. It shows that as of the first quarter of 2008, heading into the worst financial crisis since the Great Depression, the loan loss reserves to total loans at all U.S. banks stood at 1.55 percent versus those regulated by the New York Fed at 1.41 percent. That’s not too bad a disparity. Clearly, however, since all of the banks supervised by the New York Fed had to be propped up, those reserves were inadequate.

Now look at where the banking system of the United States stands today. As of the fourth quarter of 2019, all banks had loan loss reserves to total loans of 1.15 percent versus banks supervised by the New York Fed – some of the most dangerous banks in America – had a preposterous 0.82 percent loan loss reserve.

The reason that these politically-connected banks don’t want to take proper loan loss reserves is that it eats into the earnings they can report. It’s those earnings that allow the CEOs to justify their obscene pay packages and stock buybacks. Good earnings also prop up the stock price of the banks’ shares, which allow the CEOs to cash out their stock option grants at a huge windfall. Jamie Dimon, Chairman and CEO of JPMorgan Chase has become a billionaire from his stock grants and bank compensation.

To show just how politically-connected these banks are, the stimulus bill that was just passed by the U.S. Senate and is expected to go for a House vote today, contains relief from a new accounting measure that would have forced these banks to take proper loan loss reserves. The measure is called Current Expected Credit Losses or CECL (pronounced Cecil) and Wall Street-funded members of Congress have been arguing against its enactment for months in hearings. They and the behemoth banks on Wall Street finally got their wish. The stimulus bill contains this passage:

“(b) TEMPORARY RELIEF FROM CECL STANDARDS.—Notwithstanding any other provision of law, no insured depository institution, bank holding company, or any affiliate thereof shall be required to comply with the Financial Accounting Standards Board Accounting Standards Update No. 2016–13 (‘Measurement of Credit Losses on Financial Instruments’), including the current expected credit losses methodology for estimating allowances for credit losses, during the period beginning on the date of enactment of this Act and ending on the earlier of— (1) the date on which the national emergency concerning the novel coronavirus disease (COVID–19) outbreak declared by the President on March 13, 2020 under the National Emergencies Act (50 16 U.S.C. 1601 et seq.) terminates; or (2) December 31, 2020.”

Accounting firm Deloitte reported previously that the accounting rule that the Senate just waived “covers all financial assets and not just loans.” So this was, perhaps literally, a get out of jail free card for some of these banks.

Speaking of a get out of jail free card, JPMorgan Chase, which has already pleaded guilty to three criminal felony counts brought by the U.S. Department of Justice since 2014, is currently under a criminal investigation for turning its precious metals trading desk into a racketeering enterprise, according to the DOJ. Goldman Sachs is also under a DOJ criminal investigation for its role in a bribery and embezzlement scandal in Malaysia known as 1MDB. Don’t expect the DOJ to move forward with these charges while these banks are bleeding capital and making hollow promises to be good Samaritans to their credit card and home mortgage customers.

The stimulus bill is another perfect example of the 1 percent getting bailed out and the 99 percent getting sold out. The promise of $1200 checks in the mail are hardly going to level or end this corrupt and tilted playing field that is perpetually overseen by the New York Fed. (See Bernie Sanders Hasn’t Quite Captured What Wall Street Does: It’s Actually a Fraud-Monetization System with a Money-Printing Unit Called the New York Fed.)

Related Articles:

These Are the Banks that Own the New York Fed and Its Money Button

The Man Who Advises the New York Fed Says It and Other Central Banks Are “Fueling a Ponzi Market”

Is the New York Fed Too Deeply Conflicted to Regulate Wall Street?

Here’s Why the New York Fed Doesn’t Want You to See a Photo of Its Wall Street-Esque Trading Floor

The New York Fed Is Keeping JPMorgan’s Secrets Close to Its Chest

Dangerous Liaisons: New York Fed and JPMorgan’s Incestuous Relationship