Senator Elizabeth Warren

By Pam Martens and Russ Martens: May 6, 2019 ~

In May 2012 when New York Times reporter Andrew Ross Sorkin wrote his severely factually-challenged analysis of whether the repeal of the Glass-Steagall Act had led to the Wall Street collapse in 2008, he seemed to have an agenda of undermining Elizabeth Warren, then running for her first U.S. Senate seat from Massachusetts, in her push to restore the Glass-Steagall Act. That legislation, which was formally known as the Banking Act of 1933, created Federal insurance on deposits held in commercial banks while barring those banks from being under the same roof with the Wall Street casino – that is, high risk securities underwriting and trading firms known as investment banks and broker-dealers.

The legislation grew out of two intense years of Senate investigations from 1932-1934 which concluded that the “unsavory and unethical” practices by Wall Street securities trading firms had played the dominant role in the financial collapse of the 1930s. The Glass-Steagall legislation had protected the U.S. financial system from any catastrophic collapse for 66 years until its repeal under President Bill Clinton in 1999. (Clinton’s administration was heavily influenced by Wall Street figures.) Just nine years after the repeal, Wall Street would collapse in a replay of the early 1930s.

Sorkin wrote the following in his 2012 article, attempting to show that separating banks would not have prevented the collapse:

“The first domino to nearly topple over in the financial crisis was Bear Stearns, an investment bank that had nothing to do with commercial banking. Glass-Steagall would have been irrelevant. Then came Lehman Brothers; it too was an investment bank with no commercial banking business and therefore wouldn’t have been covered by Glass-Steagall either. After them, Merrill Lynch was next — and yep, it too was an investment bank that had nothing to do with Glass-Steagall.

“Next in line was the American International Group, an insurance company that was also unrelated to Glass-Steagall.”

The problem with Sorkin’s premise is that it is built on a mountain of errors. Lehman Brothers owned two Federally-insured banks — Lehman Brothers Bank, FSB and Lehman Brothers Commercial Bank. Lehman was brokering Federally-insured CDs all over Wall Street to retail customers through its bank. Lehman Brothers Commercial Bank, as of September 30, 2008, had $6.4 billion in assets and $5.65 billion in notional derivatives according to the Federal Deposit Insurance Corporation.

Merrill Lynch owned three Federally-insured banks and one of them, Merrill Lynch Bank USA, had assets of $61.6 billion and notional derivatives of $94.3 billion as of September 30, 2008 according to the Office of the Comptroller of the Currency. Merrill Senior VP, John Qua, stated in 2003 that “the combined balance sheet of our global banks is approximately $100 billion.” Merrill collapsed into the arms of Bank of America on September 14, 2008, the day before Lehman Brothers filed for bankruptcy protection.

Bear Stearns owned Bear Stearns Bank Ireland, which became part of JPMorgan Chase after its takeover of Bear with bailout support from the government. The bank was renamed JPMorgan Bank (Dublin) PLC. According to a previous statement from JPMorgan, “It is the only EU passported bank in the non-bank chain of JPMorgan and provides the firm with direct access to the European Central Bank repo window. It has also been added to the JPMorgan Jumbo issuance programs to issue structured securities for distribution outside the United States.” Structured securities is code for the instruments that blew up the U.S. financial system in 2008.

When Sorkin uses American International Group (AIG) in an attempt to undermine Elizabeth Warren’s continuing efforts to restore the Glass-Steagall Act, he is like the dumb tourist in a debate with Albert Einstein. Warren chaired the Congressional Oversight Panel that delivered its exhaustive report on June 10, 2010 on the failure and $185 billion government bailout of AIG.

At the time of the Wall Street collapse in 2008, AIG owned the Federally-insured AIG Federal Savings Bank. On June 30, 2008, it held $1 billion in assets. AIG also owned 71 U.S.-based insurance entities and 176 other financial services companies throughout the world, including AIG Financial Products (AIGFP) which blew up the whole company selling credit default derivatives and engaging in specious securities lending activities with Wall Street banks. What this has to do with Glass-Steagall is that the same deregulation legislation, the Gramm-Leach-Bliley Act that repealed Glass-Steagall in 1999, also amended the 1956 Bank Holding Company Act and allowed insurance companies and securities firms to be housed under the same umbrella in financial holding companies.

Not only did AIG own U.S. based deposit-taking banks but it owned Banque AIG, a bank it registered in France. Banque AIG was part of AIG Financial Products, the unit that blew up the giant insurer. Warren’s Congressional Oversight Panel reported the following regarding the dubious role of Banque AIG as a “balance sheet rental” facility:

“The regulatory capital swaps allowed financial institutions that bought credit protection from AIGFP to hold less capital than they would otherwise have been required to hold by regulators against pools of residential mortgages and corporate loans. A hypothetical example helps illustrate how this worked. According to the international rules established under Basel I, which generally applied to European banks prior to AIG’s collapse, a bank that held an unhedged pool of loans valued at $1 billion might be required to set aside $80 million, or 8 percent of the pool’s value. But if the bank split the pool of loans, so that the first losses were absorbed by an $80 million junior tranche, and AIGFP provided credit protection on the $920 million senior tranche, the bank could significantly reduce the amount of capital it had to set aside. Importantly, AIG’s regulatory capital swaps were sold by an AIGFP subsidiary called Banque AIG, which was a French-regulated bank.

“Under Basel I, claims on banks such as Banque AIG were assigned a lower risk weighting in the calculation of required capital reserves than the loans for which the counterparties were buying credit protection would have been assigned. This formula worked to the advantage of the counterparties, which could then use some of their regulatory capital savings to pay for the credit protection from AIGFP, and could use the remaining amount to make more loans, increasing their own leverage and risk. Because these swaps allowed banks to take on greater risk by shifting their liabilities to AIGFP, former AIG CEO Edward Liddy has referred to the deals as a ‘balance sheet rental.’ This business grew to become the largest portion of AIGFP’s CDS exposure, reflecting the demand for regulatory capital savings among European banks.”

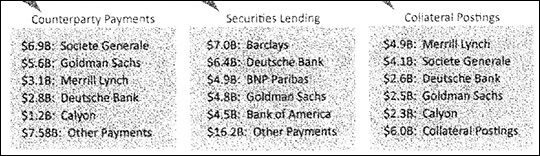

The chart below shows how government bailout money came in the front door of AIG and went out the back door to bail out Wall Street banks and their foreign counterparts who had entangled themselves in derivative trades with AIG and securities lending. Those figures, by the way, refer to billions of dollars:

Where a Large Part of AIG’s Government Bailout Money Went. Figures are in Billions. Source: Congressional Oversight Panel

Senator Warren, now running for President, is viewed as a threat by Wall Street because of her institutional knowledge of how it perpetrated the crimes that led to the greatest financial collapse since the Great Depression. The Federal Reserve Bank of New York, which implemented the majority of the $29 trillion bailout program, is also nervous about a potential President Warren.

In addition to knowing the grainy details of what led to the crash, Warren also knows where the money went and why. At a March 3, 2015 Senate hearing on Federal Reserve Accountability and Reform, Warren had this to say:

“During the financial crisis, Congress bailed out the big banks with hundreds of billions of dollars in taxpayer money; and that’s a lot of money. But the biggest money for the biggest banks was never voted on by Congress. Instead, between 2007 and 2009, the Fed provided over $13 trillion in emergency lending to just a handful of large financial institutions. That’s nearly 20 times the amount authorized in the TARP bailout.

“Now, let’s be clear, those Fed loans were a bailout too. Nearly all the money went to too-big-to-fail institutions. For example, in one emergency lending program, the Fed put out $9 trillion and over two-thirds of the money went to just three institutions: Citigroup, Morgan Stanley and Merrill Lynch.

“Those loans were made available at rock bottom interest rates – in many cases under 1 percent. And the loans could be continuously rolled over so they were effectively available for an average of about two years.”

Warren is talking about the Fed’s Primary Dealer Credit Facility (PDCF) and her math is spot on.

The obscene and unprecedented nature of secretly loaning trillions of dollars to miscreant banks has not been lost on Warren. This was the first time since 1936 that the Federal Reserve had used its Section 13(3) emergency lending powers. In the 1930s the loans amounted to $1.5 million or $27.3 million in today’s dollars. That’s a pretty far cry from $29 trillion.

Wall Street is also edgy over Warren because of her knowledge that the Financial Crisis Inquiry Commission, that also investigated the collapse under a statutory mandate, clearly thought some Wall Street executives should have gone to jail or at least been criminally prosecuted. On September 15, 2016, Warren sent a detailed, 20-page letter to the Inspector General of the Department of Justice asking for a review of those FCIC referrals. When only silence on the matter ensued from the Justice Department, Wall Street On Parade filed a Freedom of Information Act request in October 2017. (You can read the full response we received and our reporting on the matter here.) The DOJ is effectively denying the public any accountability for its actions in what was the second greatest financial crash in U.S. history.

Keep all of this in mind if you begin to read more snarky commentary from Andrew Ross Sorkin or others closely linked to Wall Street about Senator Warren or her efforts to restore the Glass-Steagall Act.