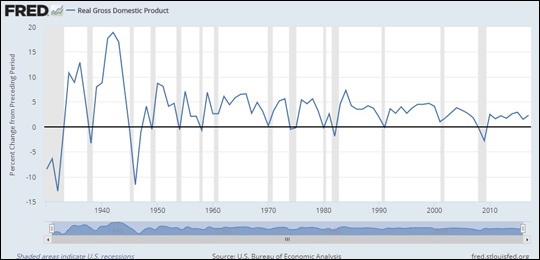

Real Gross Domestic Product (GDP) in the United States from 1930 to 2018 (St. Louis Fed)

By Pam Martens and Russ Martens: July 12, 2018 ~

According to a statistical release from the Federal Reserve, as of March 31, 2018 there were 1,812 commercial banks in the United States holding consolidated assets of $300 million or more. Of those 1,812 banks, just four banks (JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank) held 45 percent of the consolidated assets of those 1,812 banks.

But looking at data at the Federal Deposit Insurance Corporation (FDIC) the situation is even more extreme. The FDIC shows there are 5,606 insured banks in total holding $17.531 trillion in assets. JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank are holding 40.42 percent of the assets of all the insured banks in the country.

Let us put it another way. Those four banks represent 0.07 percent of all banks in the U.S. but they have somehow managed to control 40.42 percent of the assets.

These same four banks also hold the majority of deposits on which they pay a minuscule amount of interest and outsized positions in the credit card market, where, thanks to their lobbyists repealing state usury laws, they can charge double digit interest rates that run into the high teens in some cases.

On top of burying the country under an unprecedented amount of household debt by pushing their credit cards on the struggling middle class, Wall Street banks manage an outsized share of 401(k) plans and retirement plans. As Frontline reported in 2013, if you work for 50 years and receive the typical long-term return of 7 percent on your 401(k) plan and your fees are 2 percent, almost two-thirds of your account will go to Wall Street. (You can check the math in our report here.)

Wall Street is holding the U.S. economy hostage. Consumers represent almost 70 percent of Gross Domestic Product in the U.S. A tapped-out consumer means a tapped out economy – no matter how much spin the current resident of the Oval Office attempts to put on it.

Look at the Real Gross Domestic Product chart above from the St. Louis Fed. From the 1950s into the 1990s, the U.S. experienced many periods when GDP spiked above 5 percent. But in 2000 Wall Street brought us the great dot.com bust and in 2008 it brought us the greatest financial crash since the Great Depression because of a corrupt business model that remains in place today. Since 2008, an entire decade, the U.S. has been stuck in a range of an annual 2 percent or less rate of growth.

In 2015 Steve Ricchiuto, Chief U.S. Economist at Mizuho Securities USA, boldly explained to a CNBC audience what was really happening to the U.S. economy. Ricchiuto said:

“…there’s also this wrong concept that I keep hearing over and over again in the financial press about this acceleration in economic growth. That isn’t happening. Last month we had a horrible retail sales number. We had a horrible durable goods number. We’re likely to have a very disappointing retail sales number coming forward. This month we’ve had a strong payroll number – we say everything’s great. It’s not great. It’s running where it’s been. It’s been the same thing for the last five years. There’s no improvement in the economy.”

It’s time to admit what experts have been telling us for a long time. We have a big structural problem in our financial system that is concentrating wealth in the hands of too few people.

Three decades ago Lester Thurow, an MIT economist who passed away in 2016, explained today’s problem in a forward to the book by Ravi Batra, The Great Depression of 1990. Although Batra was a decade ahead of the 2000 financial meltdown, Thurow nailed the problem that was in store for the U.S. Thurow wrote:

“Depression is seen as a product of systematic tendencies for the distribution of wealth to become concentrated among a few. When this happens, demand eventually sags relative to supply and long cyclical downturns commence. Unlike some cyclical analysts, Batra believes that such cycles are not inevitable and can be controlled with social policies essentially designed to stop undue concentration of wealth from developing.

“Essentially, the economic problem is like that of the wolf and the caribou. If the wolves eat all the caribou, the wolves also vanish. Conversely, if the wolves vanish, the caribou for a time multiply but eventually their numbers become too great and they die for lack of food. Producers need consumers, and if producers deprive workers of their fair share of production income they essentially deprive themselves of the affluent consumers they need to make their facilities profitable. One could think of Batra’s argument as a kind of economic ecology where there is a ‘right’ environmental balance.”

Another economist, Michael Hudson, brilliantly explained in his 2015 book Killing the Host: How Financial Parasites and Debt Bondage Destroy the Global Economy that Wall Street’s parasitic banks have tricked society into accepting them as a productive part of the U.S. economy. Hudson writes that “Any given development crisis is said to be a natural product of market forces, so that there is no need to regulate and tax the rentiers.”

Think about that for a moment. The very banks that brought the country to the edge of financial collapse have been allowed to grow exponentially larger and more dangerous today. The Federal regulator that failed to rein in the abuses on Wall Street in the lead up to the 2008 crash – the Federal Reserve – was the very regulator that was given more authority over the banks by Congress in the Dodd-Frank financial reform legislation that was passed in 2010. Today, the Fed is still wearing blinders and effectively giving the big Wall Street banks the okay to shore up their stock prices through unprecedented amounts of stock buybacks.

One chapter in Hudson’s book begins with a quote from John Maynard Keynes: “When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.” Hudson writes further:

“Instead of warning against turning the stock market into a predatory financial system that is de-industrializing the economy, [business schools] have jumped on the bandwagon of debt leveraging and stock buybacks. Financial wealth is the aim, not industrial wealth creation or overall prosperity. The result is that while raiders and activist shareholders have debt-leveraged companies from the outside, their internal management has followed the post-modern business school philosophy viewing ‘wealth creation’ narrowly in terms of a company’s share price. The result is financial engineering that links the remuneration of managers to how much they can increase the stock price, and by rewarding them with stock options. This gives managers an incentive to buy up company shares and even to borrow to finance such buybacks instead of to invest in expanding production and markets.”

These trends have resulted in the current authoritarian dystopia we call the Trump administration for lack of a better phrase. The billionaires and the billionaires-in-waiting have effectively mounted a hostile takeover with Wall Street’s lawyers and lobbyists and the Charles Koch Big Money Network pulling the levers from behind a dark curtain.

One needs no greater proof than what has happened to the Environmental Protection Agency, the U.S. withdrawal from the Paris Climate Accord, the inhumane treatment of immigrant children at our southern border, the U.S. withdrawal from the UN Human Rights Council in June, the efforts to gut the Consumer Financial Protection Bureau, the stacking of the Federal courts with corporate friendly judges, and the President of the United States cozying up to dictators and human rights abusers while humiliating our country’s strongest allies.

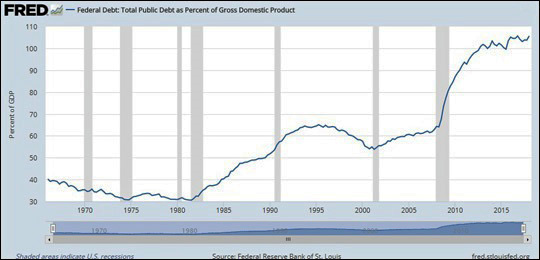

And, even more dangerous to getting our fiscal house in order, the President delivered a tax cut for the corporations and the wealthy that will explode our national debt at a time when it is already at a dangerous level. (See chart below.)

Americans can no longer pretend any of this is normal. Citizens are facing the fight of their lifetimes to restore representative government to America while there is still time to do so. That fight begins with breaking up the big Wall Street banks and restoring the Glass-Steagall Act. It next requires a meaningful overhaul of political campaign financing; election of the President by popular vote; term limits on Federal judges; elimination of the power of the President to fire U.S. Attorneys; restoration of state usury laws; and the elimination of Wall Street’s private justice system where it has impunity to loot customers and then charge them thousands of dollars in fees to hear their case before a rigged panel of arbitrators.

Public Debt as a Percent of GDP