By Pam Martens and Russ Martens: August 23, 2017

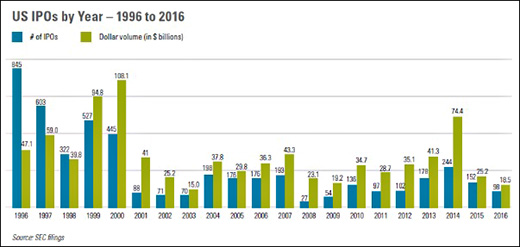

In 1996 the U.S. had 845 Initial Public Offerings. Last year, after twenty passing years of research and budding new technologies should have fueled growth in the IPO market, the U.S. had a paltry 98 IPOs. According to a study by the law firm, Wilmer Cutler Pickering Hale and Dorr, gross proceeds from IPOs in 2016 were $18.54 billion while the “average annual gross proceeds for the 12-year period preceding 2016 were $35.73 billion — 93 percent higher than the corresponding figure for 2016.”

Not only has the U.S. seriously lost ground in IPOs but the total number of publicly traded companies in the U.S. is down by almost half in the same 20 year span. Last September, Jim Clifton, the Chairman and CEO of Gallup, the polling company, explained why he thinks this is happening. Clifton wrote:

“The number of publicly listed companies trading on U.S. exchanges has been cut almost in half in the past 20 years — from about 7,300 to 3,700. Because firms can’t grow organically — that is, build more business from new and existing customers — they give up and pay high prices to acquire their competitors, thus drastically shrinking the number of U.S. public companies. This seriously contributes to the massive loss of U.S. middle-class jobs.”

Let’s also not forget that quite a number of those 7,300 companies that were listed in 1996 failed in the great dot.com crash of 2000 because Wall Street’s minions pumped out bogus buy recommendations on new companies that didn’t have a prayer of making it as an ongoing business. The real motive behind the listing was to fuel fat bonuses for themselves. The largest investment banks were calling the startups they were peddling to the public “dogs” and “crap” behind closed doors while lauding their virtues in “research” released to entice the public to buy.

Writing in the New York Times in 2001, Ron Chernow precisely analyzed how the Nasdaq stock market, Wall Street’s primary market for tech startups, had functioned. Chernow wrote:

“Concern has centered on the misery of small investors maimed in the tech wreckage. But what happened to all the money they squandered in the I.P.O.’s? Think of the stock market in recent years as a lunatic control tower that directed most incoming planes to a bustling, congested airport known as the New Economy while another, depressed airport, the Old Economy, stagnated with empty runways. The market has functioned as a vast, erratic mechanism for misallocating capital across America.”

At the time of Chernow’s article, $4 trillion had been erased from the stock market.

Those who have taken a long, hard, honest look at Wall Street understand that it is in critical need of deep structural change: that America cannot begin to heal economically until Wall Street’s invisible hand is removed from our pocket.

The decline in both the quantity and quality of IPOs began around the same time that the Wall Street mega banks acquired the Four Horsemen — four boutique investment banks: Alex. Brown & Sons, Robertson Stephens, Montgomery Securities, and Hambrecht & Quist. As we previously reported:

“Alex Brown’s roots dated back to 1808. It was involved in the IPO of Microsoft and Oracle Systems. It was acquired by Bankers Trust in 1997 and two years later merged into the German behemoth Deutsche Bank.

“Robertson Stephens was a much younger firm, starting out in 1978. The firm was involved in the IPOs of Sun Microsystems, Excite and Chiron. Before being sold to BankAmerica for $540 million in 1997, the company was lead or co-manager on 10 of the top 25 best IPO performers in 1997. (The firm was resold several times after that, each time to a large commercial bank and eventually liquidated.)

“Montgomery Securities, heavily involved in high-tech issues, was sold to Nationsbank for $1.2 billion in 1997. Nationsbank would acquire BankAmerica the following year, but keep the name BankAmerica as the legal entity. In 2008, during the financial crisis, BankAmerica purchased the large retail brokerage firm, Merrill Lynch, which was teetering near insolvency.

“Boutique investment bank, Hambrecht & Quist, was the final of the Four Horsemen. The firm was founded by Bill Hambrecht and George Quist in 1968. The firm was the underwriter of the following well known firms: Apple Computer, Genentech, Adobe Systems, Netscape, and Amazon.com. In September 1999, Chase Manhattan Bank acquired the firm for $1.35 billion. The firm is now part of the largest U.S. bank, JPMorgan Chase…”

“There is no question that the current structure of Wall Street is both unsustainable and a critical head wind to ramping up economic growth in America. The pivotal role played by the previous independent boutique investment firms and investment bank partnerships which had their own money on the line when they invested in startups, must be thoroughly investigated by Congress before it makes any sweeping decisions on restructuring Wall Street.”

Another critical Wall Street reform that must be addressed is restoring the Glass-Steagall Act that would separate banks that hold taxpayer-backed, insured deposits from the gambling casinos on Wall Street. It’s not just that taxpayers should never be put on the hook again for another massive Wall Street bailout. It’s equally critical that five mega banks on Wall Street stop controlling the destiny of the nation through their unprecedented concentration of deposits, derivatives, credit cards, mortgage and commercial loans, hedge fund financing and control of the electoral process through their campaign financing.

And finally, Wall Street’s perpetual invisible hand in our pocket is facilitated by the lack of transparency for its crimes as a result of it setting up its own private justice system which bars the public and the press from these private adjudications which are rigged by their very structure of limiting discovery, selecting arbitrators from a limited pool completely unlike jury pool selection, and ignoring case law and legal precedent in deciding the case. Known as mandatory arbitration, the process has been shown time after time to be as bogus as the dot.coms Wall Street was peddling during the illusory tech boom.

The nation’s courts need to be reopened immediately to hear Wall Street’s crimes against both its customers and its employees. The Seventh Amendment to the U.S. Constitution guarantees this right:

“In Suits at common law, where the value in controversy shall exceed twenty dollars, the right of trial by jury shall be preserved, and no fact tried by a jury, shall be otherwise re-examined in any Court of the United States, than according to the rules of the common law.”

Darkness, fraud and a rigged wealth transfer system currently constitute the business model of Wall Street. Until critical structural reforms are made to Wall Street, all that the Trump followers have is a meaningless slogan on a red hat growing tattered and dusty with age.