Retail Sales for Past Year (Courtesy of Trading Economics and Census Bureau.)

By Pam Martens and Russ Martens: September 22, 2016

Yesterday the Federal Open Market Committee (FOMC) of the Federal Reserve released its policy statement, which included its announcement to stand pat on interest rates at this meeting. The third sentence of this policy statement went like this: “Household spending has been growing strongly….” To use the parlance of Wall Street, the Fed was putting lipstick on a pig.

The average American might read that statement as it bounced around the newswires and conflate “household spending” with a strong consumer. Nothing could be further from the truth. Household spending data is actually capturing how Wall Street masterminds continue to fleece the 99 percent.

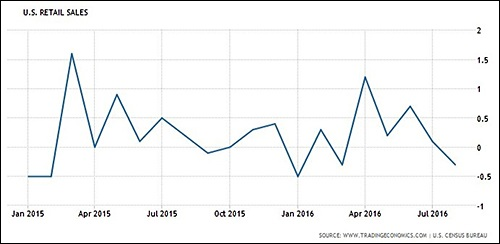

Just six days before the FOMC policy statement was issued, this is how USA Today reported on the strength of the consumer based on the Commerce Department’s release of retail sales data:

“U.S. retail sales slumped in August as auto and gasoline purchases fell and a core reading was unexpectedly weak, raising questions about consumer spending growth in the current quarter.

“Sales fell 0.3%, more than the 0.1% decline economists expected. A core measure — that excludes the volatile categories of autos, gasoline, building materials and food services — slipped 0.1%. Economists had forecast a 0.4% rise.”

Why is household spending going in one direction and consumer spending in another?

The Bureau of Labor Statistics (BLS), part of the U.S. Department of Labor, states that it is the “principal Federal agency responsible for measuring labor market activity, working conditions, and price changes in the economy.” BLS includes such expenditures as housing costs, transportation, education, personal insurance and pensions in its “household spending” data. BLS found the following in its data release for 2015:

“All major components of household spending increased in 2015… Of these, expenditures on personal insurance and pensions showed the greatest percentage increase, 10.9 percent. This was followed by education expenditures, rising 6.4 percent, transportation expenditures, rising 4.7 percent, and entertainment expenditures, rising 4.2 percent.”

The BLS found that the increase in education expenditures resulted largely from a “63.7 percent increase in finance, late, and interest charges for student loans….” The horror stories coming out of the Consumer Financial Protection Bureau from the young student debt slaves of the Wall Street banks put a human face on this statistic. The one percent have simply found more ingenious ways to fleece the 99 percent and call it “household spending.”

The housing cost statistic offered by BLS also fails to capture the financial distress being imposed on millions of Americans by Wall Street hedge funds and private equity funds that are scooping up homes in distressed neighborhoods and hiking rents far above fair market rates. In a report last Fall, American Prospect Magazine found the following:

“…in areas where Wall Street investors own a significant number of these single-family homes—including Atlanta, Las Vegas, Phoenix, Miami, Tampa, Orlando, Charlotte, Dallas, Chicago, Detroit, Denver, and Los Angeles and nearby Riverside—their practices have harmed tenants and undermined long-term neighborhood stability.

“In April of this year, for example, one-quarter of all home sales were to cash-carrying investors. Since 2010, institutional investors backed by Wall Street have purchased a total of 528,369 single-family homes nationwide, led by Florida (78,155), California (52,802), Georgia (46,914), Arizona (35,979), and North Carolina (34,769), according to RealtyTrac…Together, these Wall Street entities have raised close to $70 billion to buy these homes.”

A report issued by the Pew Charitable Trusts on March 30, 2016 put this housing impact on lower income households into sharp perspective:

“Since the start of the housing crisis in 2007, home ownership rates have declined among households in the middle- and upper-income tiers. These decreases have affected the rental market, as former owners became renters, leading to rental vacancy rates at historical lows below 7 percent. The diminished supply of rental properties increased the cost of rental housing dramatically; in 2014, renters at each rung of the income ladder spent a higher share of their income on housing than they had in any year since 2004. Although both renters and homeowners spent more for housing in 2014, notable differences in the proportion of household resources going to shelter were evident across income groups, with lower-income renter households spending close to half of their pretax income on rent.”

The increase in household spending is nothing to cheer about for the average American as the benefits are flowing to the same one percent that tanked the economy in 2008, creating the worst wealth destruction for the average American since the Great Depression, and have now simply found ever more creative ways to continue to soak the 99 percent.