Citigroup Headline at Risk Magazine Web Site, January 27, 2016

By Pam Martens and Russ Martens: August 4, 2016

Having closely observed how Citigroup collapsed under the weight of its own corruption and risk-taking hubris in 2008 and spread its contagion across Wall Street, a headline we never dreamed we would see in our lifetime is shown above from Risk Magazine’s web site. The article under the heart-stopping headline is dated January 27, 2016 and informs readers that Citigroup is now viewed by clients as one of the top-three market makers in single name Credit Default Swaps in both North America and Europe.

Credit Default Swaps are the instruments that blew up the giant insurance company, AIG, in 2008, requiring the U.S. government to bail out the company to the tune of $185 billion. The bailout money went in the front door of AIG and was then funneled out the backdoor to the big Wall Street banks that had used AIG as their counterparty to guarantee their bets on Credit Default Swaps. The AIG bailout was effectively a backdoor bailout of the biggest banks on Wall Street.

Credit Default Swaps also played a role in Citigroup’s implosion in 2008, which necessitated the following government bailout: $45 billion in equity infusions; over $300 billion in asset guarantees; and more than $2 trillion in cumulative, below-market-rate loans from the Federal Reserve. Citigroup, then and now, holds insured savings deposits while at the same time engaging in high risk trading at both its investment bank and commercial bank.

Sheila Bair was the head of the Federal Deposit Insurance Corporation (FDIC) during the 2008 crash. The FDIC is the Federal agency that insures the deposits of U.S. commercial banks and savings associations. Bair published an authoritative book on the crisis, Bull by the Horns. This is an excerpt of what Bair had to say about Citigroup’s management of risk and its Credit Default Swaps:

“By November, the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking…It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

The OCC and the New York Fed are doing the exact same thing today – cowering under the lobbying and political clout of Citigroup – which perversely just hired Mervyn King, the former head of the Bank of England, the U.K.’s central bank, now that former Treasury Secretary Robert Rubin has collected his $120 million from Citigroup and moved on.

What exactly is a single name Credit Default Swap? In simple terms, it’s a derivative that allows a bet to be placed on whether a corporate issuer will default on its corporate bonds. There are two sides to every trade: one side is buying protection against the bankruptcy or default of the issuer of the bond; the other side is selling the protection and taking on the risk that they will have to make good on the Credit Default Swap if the issuer triggers a credit event under the terms of the contract.

The first problem is that there are few, if any, counterparties that have guaranteed these contracts with enough capital to make good on these obligations if a major bank, which has been heavily bet against, goes under. (Think Lehman Brothers.) A major bank going under would impair the capital of all other major banks because of the interconnectedness of Wall Street. Trillions of dollars in Credit Default Swaps simply ensures another massive government bailout in the next financial crisis.

Also, the concept of insurance through the ages is that one must have an insurable interest in order to buy insurance. For example, one can’t take out a life insurance policy on their neighbor because of the incentive to knock him off and collect the proceeds. Likewise, one can’t buy homeowner’s insurance on a neighbor’s house because of the incentive to burn it down and collect the policy proceeds.

The same problem crops up with Credit Default Swaps. It’s one thing if a bank makes a $100 million loan to ABC Corporation and then buys a Credit Default Swap for the same amount to hedge their risk. But many speculators simply pile into single name Credit Default Swaps when a bank or corporation looks to be in trouble. This is pure gambling and should never be aided and abetted by an insured depository institution which, under law, is required to maintain the safety and soundness of bank deposits.

The slogan of the Office of the Comptroller of the Currency (OCC), the Federal agency that regulates national banks, is: “Ensuring a Safe and Sound Federal Banking System for All Americans.” What’s it’s actually doing instead is ensuring that another epic financial crisis is in the cards for America.

Take, for example, a quarterly report proudly published by the OCC that seems to brag about the value of all kinds of exotic trading, including derivatives, taking place at the behemoth Wall Street banks. Since 1999 and the repeal of the Glass-Steagall Act, these same banks also hold the majority of the insured savings deposits in the U.S. An insane and combustible mixture if ever there was one.

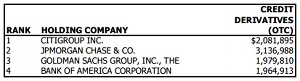

The most recent quarterly report from the OCC on trading and derivatives at the insured banks as of the end of the first quarter of this year, illustrates the extent to which Citigroup has plowed into the trading of Credit Default Swaps.

According to the data, Citigroup now has $2.08 trillion in Credit Derivatives (the vast majority of which are Credit Default Swaps). Only JPMorgan is bigger with $3.1 trillion in credit derivatives. Equally frightening, the vast majority of these are private contracts between financial institutions (Over-the-Counter) where regulators lack the granular details of the deals. President Obama falsely promised the American people that derivatives would be moved onto exchanges with proper capital and transparency following the Dodd-Frank financial reform legislation in 2010. That has not happened. The vast majority of all derivatives are still traded in the dark.

Not only are Citigroup’s Federal regulators allowing it to engage in this high risk trading but they are actually allowing Citigroup to purchase the high risk positions of a deeply troubled bank – Deutsche Bank. Risk Magazine reports in the article linked above that Citigroup bought $250 billion of Credit Default Swaps from Deutsche Bank in 2013. Bloomberg News also reported on the $250 billion Citigroup purchase from Deutsche Bank.

In total derivatives, as of the end of the first quarter of this year, the OCC reports that at the bank holding company level, Citigroup has now eclipsed even JPMorgan. Citigroup now holds $55.6 trillion in notional amount of all types of derivatives versus JPMorgan’s $52.3 trillion.

It’s long past the time for the adults to enter the room.

Notional Amount of Credit Derivatives at Four Largest Dealers as of March 31, 2016 (Source OCC: In Billions of U.S. Dollars)