By Pam Martens and Russ Martens: March 16, 2016

Since Wall Street’s felony counts last May (see “Related Articles” below) and the unleashing of ever more creative ways to fleece the populace, it’s getting tougher and tougher to find people willing to shill for the Wall Street claptrap that it’s been punished enough and it’s time to put the bashing to rest. It’s getting tougher — but not impossible.

Since Wall Street’s felony counts last May (see “Related Articles” below) and the unleashing of ever more creative ways to fleece the populace, it’s getting tougher and tougher to find people willing to shill for the Wall Street claptrap that it’s been punished enough and it’s time to put the bashing to rest. It’s getting tougher — but not impossible.

Matt Winkler, the Bloomberg News Editor-in-Chief Emeritus, wrote an opinion piece and appeared on Bloomberg TV last week to regurgitate the threadbare “Stop Bashing Wall Street. Times Have Changed” refrain. Winkler starts off with this premise:

“One of the reasons the American economy is performing better than any of the largest in Asia and Europe is that its regulators have repaired the damage of the financial crisis and the worst recession since the Great Depression. Led by the Federal Reserve, they replaced incentives for reckless speculation with catalysts for old-fashioned credit creation backed by levels of capital that are unprecedented in modern times.”

If the U.S. economy is doing better than Europe, it has less to do with the banks than with the fact that when Obama took office the U.S. national debt was $10 trillion and now it’s $19 trillion. Washington has resuscitated today’s economy on the backs of the next generation. That $19 trillion doesn’t include the other $4.5 trillion hiding out at the Federal Reserve from buying up the drek from Wall Street banks’ balance sheets. The Federal Reserve had a balance sheet of only $800 billion before its three rounds of drek buying began (a/k/a quantitative easing).

Winkler also fails to note that the U.S. economy has been growing at a rate barely able to fog a mirror, despite the trillions spent in pump priming. As Steve Ricchiuto, Chief U.S. Economist at Mizuho Securities USA, told CNBC in February 2015:

“…there’s also this wrong concept that I keep hearing over and over again in the financial press about this acceleration in economic growth. That isn’t happening. Last month we had a horrible retail sales number. We had a horrible durable goods number. We’re likely to have a very disappointing retail sales number coming forward. This month we’ve had a strong payroll number – we say everything’s great. It’s not great. It’s running where it’s been. It’s been the same thing for the last five years. There’s no improvement in the economy.”

According to the Atlanta Fed’s current GDPNow forecast, we’re still looking at a tepid 1.9 growth in the first quarter.

Even if the U.S. economy were doing better, it has been well established that the majority of citizens can’t participate in that growth under the current one percent stranglehold. As Senator Bernie Sanders repeatedly tells the thousands turning out for his rallies:

“There is something profoundly wrong when the top one-tenth of one percent owns almost as much wealth as the bottom 90 percent. There is something profoundly wrong when 58 percent of all new income since the Wall Street crash has gone to the top one percent.”

Winkler really treads into fantasy land with the statement: “Led by the Federal Reserve, they replaced incentives for reckless speculation with catalysts for old-fashioned credit creation…” If the conflicted Fed had actually ended the reckless speculation, how could JPMorgan’s London Whale have occurred in 2012? The financial crash occurred in 2008. The Dodd-Frank financial reform was signed into law in 2010. But the London Whale, where JPMorgan Chase gambled with hundreds of billions of dollars of its insured bank’s deposits and lost $6.2 billion in exotic derivative gambles in London, happened in 2012. The unprecedented, admitted to, felony counts against Citigroup and JPMorgan Chase for rigging foreign currency markets came just last year – five long years after the crash.

Winkler also makes this jaw-dropping statement: “The biggest banks today bear little resemblance to the risk-embracing juggernauts of a decade ago.” In fact, the hapless Fed was just called out by researchers at the U.S. Treasury’s Office of Financial Research for not knowing what it was doing in its stress tests of the biggest Wall Street banks to measure counterparty risk in the system. According to the researchers, “counterparty credit risks to the banking system collectively have risen and may suggest a greater systemic risk than is commonly understood.”

Winkler makes yet another assertion that is totally unhinged from reality:

“Banks also have reined in most of the proprietary trading in derivatives that brought them into conflict with their depositors.”

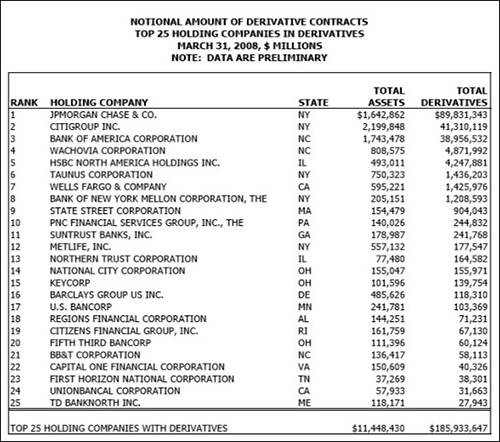

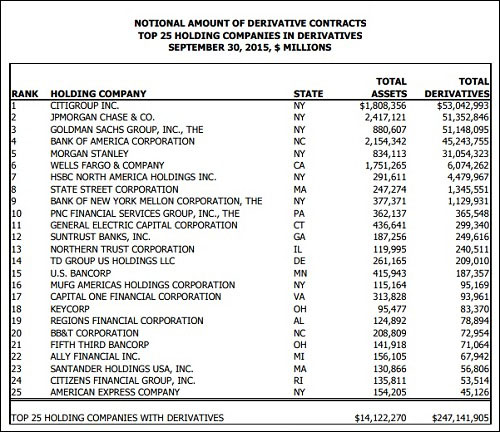

That’s simply a whopper of a misstatement. According to the official reports from the regulator of national banks, the Office of the Comptroller of the Currency, at the end of the first quarter of 2008, the 25 top bank holding companies in derivatives held $186 trillion in derivatives. As of September 30, 2015, that figure is $247 trillion – a 33 percent increase. (See charts below.)

As we reported on January 16, risk from derivative concentrations at a handful of Wall Street banks has also increased since the crash in 2008. Just five Wall Street banks — Citigroup, JPMorgan Chase, Goldman Sachs, Bank of America and Morgan Stanley – are sitting on $231 trillion in notional derivatives as of September 30 of last year. That amounts to 93 percent of all derivatives held by all 6,100 banks in the U.S.

Matt Winkler previously came under scrutiny by the New York Post, the New York Times and others in 2013 for Bloomberg reporters’ allegations of his spiking stories critical of China after the Bloomberg reporters had worked on them for the better part of a year. The New York Post reported that reporter Michael Forsthye “was escorted from Bloomberg’s Hong Kong office” on November 14, 2013 “after he was fingered as the person who leaked embarrassing claims about how the news and data giant spiked a story that could have angered leaders in China.” Winkler denied the allegations but the Times dryly noted:

“Most important for the larger Bloomberg company’s bottom line, financial news terminal subscriptions, which cost more than $20,000 per year and are the main revenue generator for Bloomberg, slowed for a spell in China, after officials issued orders to some Chinese companies to avoid buying subscriptions.”

The drubbing of Winkler included a video satire (see below) of the Bloomberg affair, released by Next Media Animation. The video noted that Mike Bloomberg would be leaving the Mayor’s office shortly and had announced plans to visit China to build greater business ties. During Mayor Bloomberg’s 12 year stint in public office, his wealth ballooned more than ten-fold, growing from $3 billion to $31 billion according to Forbes. The bulk of his wealth stems from those Bloomberg Terminals which now cost $24,000 a year and are spread across the trading floors of Wall Street and global banks.

Related Articles:

Citigroup Was Using Taxpayer Bailout Funds While Committing Its Foreign Currency Felony

JPMorgan’s Jamie Dimon Deals With His Bank’s Felony Charge – Badly