By Pam Martens and Russ Martens: December 29, 2021 ~

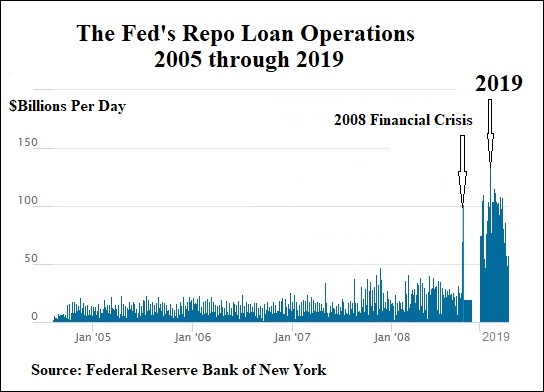

The conventional wisdom is that the Fed’s recent emergency lending facilities to Wall Street were caused by the COVID-19 crisis. The above chart, which uses the New York Fed’s own Excel spreadsheet repo loan data, shows the conventional wisdom is dangerously wrong.

In the last quarter of 2019 – before there was any news of COVID-19 in the U.S., and months before the World Health Organization declared COVID-19 a pandemic – the Fed pumped $4.5 trillion in cumulative repo loans to unnamed trading houses on Wall Street – its so-called “primary dealers.”

The collateral that the Fed accepted for the cumulative $4.5 trillion in loans consisted of $3.497 trillion in U.S. Treasury securities; $988.3 billion in agency Mortgage-Backed Securities (MBS); and $15.839 billion in agency debt.

The Fed’s emergency repo loan operations began on September 17, 2019. From September 17, 2019 through the last acknowledged operation on July 2, 2020, the Fed’s repo loans cumulatively totaled $11.23 trillion, made up of the following pledged collateral: $7.137 trillion in U.S. Treasury securities; $4 trillion in agency Mortgage-Backed Securities (MBS) and $91.525 billion in agency debt.

Just how fragile were Wall Street’s trading houses at that time that they needed to continuously roll over loans from the Fed – some on an overnight basis, others for weeks at a time? A quick gauge of the depth of the crisis in the last four months of 2019 is to compare the total of repo loans made in the 2008 financial crisis to those made in 2019. We’ve provided the chart at the top of this article for a quick snapshot.

The 2008 financial crisis was the worst in the United States since the Great Depression. Century-old Wall Street financial institutions were collapsing like a house of cards. And yet, the Fed only funneled a total of $3.144 trillion in repo loans to its primary dealers from January 2 through December 30, 2008. Instead, the Fed decided to set up an alphabet soup list of emergency bailout facilities through which it secretly issued $29 trillion in cumulative loans from December 2007 to July 2010.

The Fed rolled out many of those same 2008 emergency bailout facilities beginning in March of 2020 after the World Health Organization declared a pandemic on March 11.

Looking at the chart above and now having the precise tally of the $11.23 trillion in cumulative repo loans the Fed made from September 17, 2019 through July 2, 2020, it now appears that the bulk of the emergency repo loans were a stand-in operation until the Fed could roll out its full ensemble of emergency lending programs, which it carefully characterized as “in response to COVID-19.”

So the question is, if the pandemic was officially declared on March 11, 2020 and the first case of COVID-19 in the U.S. was confirmed by the CDC on January 20, 2020 – what caused the financial emergency on Wall Street in the fall of 2019 that required trillions of dollars in repo loan bailouts from the Fed?

The Fed has failed to provide any credible answers to that question. At first, the Fed suggested that corporate tax payments were drained from the system causing a liquidity crunch. But look carefully at the chart above. Corporations were making those same tax payments from 2009 through 2018 without causing a financial crisis or the need for trillions of dollars in emergency repo loans from the Fed.

Under Section 1103 of the Dodd-Frank financial reform legislation of 2010, the Fed has to disclose to the public its repo lending operations “on the last day of the eighth calendar quarter following the calendar quarter in which the covered transaction was conducted.” That means that the names of the banks and the amounts they borrowed from the Fed’s repo loan operations for the fourth quarter of 2019 are legally required to be reported this Friday.

The Fed has already reported the data for September 17, 2019 through September 30, 2019 as part of its report for the third quarter of 2019. That information was censored by every mainstream business news outlet. Wall Street On Parade broke the story on October 13. It will be fascinating to see if Friday’s report from the Fed – on New Year’s Eve no less – gets the same treatment from mainstream business media.

The data previously released by the Fed for the last 14 days of September 2019 shows that Goldman Sachs and Nomura Securities International (part of a Japanese financial firm) borrowed huge sums under the Fed’s 14-day term repo loans. Goldman Sachs had $29.6 billion in 14-day term repo loans outstanding by September 27, then took an additional $5 billion one-day repo loan on September 30. Nomura, by September 27, had $30 billion outstanding in 14-day term loans.

Another large term-loan borrower was a unit of JPMorgan Chase – the largest bank in the United States. On September 27, JPMorgan Securities had a total of $20 billion in 14-day term repo loans outstanding. On September 30, JPMorgan Securities took an additional $8 billion one day repo loan.

On the first day of the emergency repo loan operations on September 17, the New York Fed provided a total of $53.15 billion in one-day repo loans. JPMorgan Securities was the largest borrower at $7.6 billion or 14 percent of the total. At the time, JPMorgan Chase held $1.6 trillion in deposits. Why did it need $7.6 billion from the Fed on the very first day the emergency repo loan operations began?

In addition to the $7.6 billion borrowed by JPMorgan Securities on the first day of repo operations on September 17, UBS Securities, a unit of the Swiss multinational investment bank UBS, borrowed $5.5 billion or 10 percent of the total offered that day.

Also taking large repo loans on the first day of operations on September 17 was BNP Paribas Securities, part of the French investment bank, which took $5 billion of the $53.15 billion or 9 percent. Goldman Sachs also took $5 billion or another 9 percent; Citigroup borrowed $3.5 billion; Nomura Securities borrowed $3.5 billion; the New York branch of Societe Generale, a French multinational investment bank, borrowed $3 billion; the New York unit of the Bank of Nova Scotia borrowed $2.5 billion; Barclays Capital, part of the U.K. bank, took $2.4 billion (There were numerous other borrowers.)

Repos (repurchase agreements) are a short-term form of borrowing where corporations, banks, securities firms and money market mutual funds secure loans from each other by providing safe forms of collateral such as Treasury securities. The repo loan market is supposed to function without the assistance of the Federal Reserve. Instead, on July 28 of this year, the Fed announced that it is now creating a “Standing Repo Facility” that will offer $500 billion each weekday to the Fed’s 24 primary dealers with additional counterparties to be added. (See The Fed Gets Its Ducks in a Row for the Next Wall Street Bailout; Quietly Adds Goldman Sachs Bank, Citibank to Its New $500 Billion Standing Repo Facility.)

We do not know at what time the Fed will release the data on Friday but when it does, it will be available here.