By Pam Martens and Russ Martens: April 20, 2023

On Wednesday, the Federal Reserve released its Beige Book, a compilation of current economic conditions in each of its 12 Federal Reserve districts. The information that was collected in each of the regional reports was gathered on or before April 10 – so it is relatively current.

It is not a good sign that three of the Fed districts that pump out a significant chunk of U.S. GDP reported that bank credit had tightened noticeably, ostensibly as fallout from the banking collapses in March and depositor runs.

The New York Fed reported that credit conditions in the Second Fed District, which includes New York state, the 12 northern counties of New Jersey, Connecticut’s Fairfield County, Puerto Rico and the U.S. Virgin Islands, “deteriorated sharply.” It summarized the situation as follows:

“Conditions in the broad finance sector deteriorated sharply coinciding with recent stress in the banking sector. Small to medium-sized banks in the District reported widespread declines in loan demand across all loan segments. Credit standards tightened noticeably for all loan types, and loan spreads continued to narrow. Deposit [interest] rates moved higher. Finally, delinquency rates edged up on residential and commercial mortgages.”

One of the banks that failed in March and was put into receivership by the Federal Deposit Insurance Corporation (FDIC) was Signature Bank, which was headquartered in Manhattan. Signature Bank was the third largest bank failure in U.S. history.

The San Francisco Fed, whose District has been the epicenter of collapsing banks and/or their share prices, reported the following regarding credit conditions:

“Lending activity fell significantly in recent weeks amid higher interest rates and elevated uncertainty in the banking sector. Lending standards tightened notably, and several depository institutions opted to reduce loan volumes, especially for new clients, despite reporting ample liquidity. Reports indicated that existing and planned projects across sectors were delayed or cancelled due to higher funding costs, heightened uncertainty, and more limited access to credit. Following recent volatility in deposit levels at regional and community banks, outflows have reportedly stabilized since late March.”

The second largest bank failure in U.S. history, Silicon Valley Bank, occurred in March in this District. See our report: Silicon Valley Bank Was a Wall Street IPO Pipeline in Drag as a Federally-Insured Bank; FHLB of San Francisco Was Quietly Bailing It Out. (The largest bank failure in U.S. history was Washington Mutual, which occurred during the financial crisis of 2008.)

A federally-insured bank that had immersed itself in crypto-related deposits, Silvergate Bank, headquartered in California, also failed in March but was allowed to wind itself down. There continue to be growing concerns about the survivability of San Francisco-based First Republic Bank, whose stock price has lost 90 percent of its value year-to-date. See our report from yesterday: Liquor Sales Will Be Brisk on Wall Street Ahead of First Republic Bank’s Earnings Report on Monday.

Although it was not clear why, the Dallas Fed also reported a particularly dour outlook in its district, writing as follows:

“Loan demand continued to decline in March as bankers reported worsening business activity. Loan volumes fell, driven largely by a sharp contraction in consumer loans. Loan performance worsened slightly overall. Credit standards and terms tightened sharply, and marked increases in loan pricing were noted. Banking outlooks continued to deteriorate, with contacts expecting a contraction in loan demand and business activity and an increase in nonperforming loans over the next six months. Increased uncertainty and lack of confidence resulting from the recent banking issues were cited as concerns.”

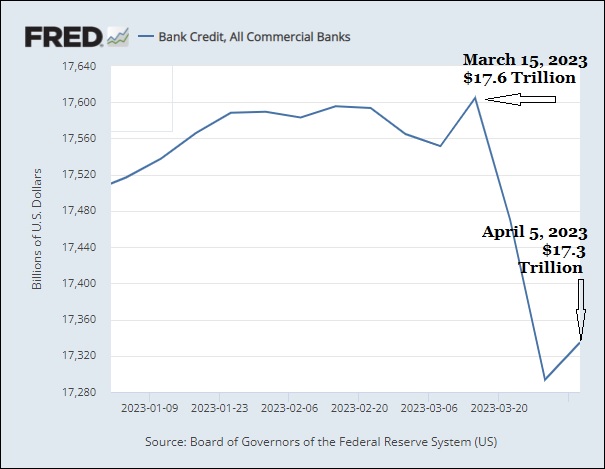

The revelations in the Beige Book are compatible with the Fed’s separate data on total bank credit at all commercial banks, which plunged by $300 billion between March 15 and April 5, the latest data available. That is a dramatic decline in the span of three weeks. (See chart above.)