By Pam Martens and Russ Martens: September 25, 2022 ~

The corrupt political backdrop for today’s unprecedented market quagmire feels like a hyperbolic trailer for a low-budget sci-fi thriller: The former president of the only remaining superpower in the world has been charged with “staggering” frauds against banks – the ones he just deregulated as president. (This same former president was also caught red-handed with Top Secret documents after he left public office — but the super power’s 18 intelligence agencies have no idea what he did, or was planning to do, with these documents.)

The corrupt political backdrop for today’s unprecedented market quagmire feels like a hyperbolic trailer for a low-budget sci-fi thriller: The former president of the only remaining superpower in the world has been charged with “staggering” frauds against banks – the ones he just deregulated as president. (This same former president was also caught red-handed with Top Secret documents after he left public office — but the super power’s 18 intelligence agencies have no idea what he did, or was planning to do, with these documents.)

On the other side of the globe, the sitting president of a bygone superpower is engaging in nuclear saber-rattling and conscripting 60-year-old men to fight an illegal war while young, able-bodied men flee the country en masse.

The world’s financial markets have gone off the rails in an equally disorienting fashion. The central bankers that had created bubbles in almost every asset class by keeping interest rates at zero for years, are now in competition for how fast they can raise interest rates in order to keep their currencies from collapsing and causing further crippling inflation. The dramatic spike in interest rates around the globe is causing prices to collapse in everything from stocks, bonds, commodities, and risk assets. There is nowhere for investors to hide.

Even the typical safe havens are quick sand. Gold has fallen from more than $2,000 in March to a closing price of $1,651.70 last Friday, a decline of 17.4 percent from March.

How about hiding out in short-term U.S. Treasury securities? Isn’t that always a safe haven? Not this time. Consider the share price of the Vanguard Short-Term Treasury Exchange Traded Fund (ETF). It sported a $61 share price last December. It closed at $57.79 on Friday. That’s because the Fed has promised to continue the pain (hiking short-term interest rates, which causes losses in existing debt instruments with lower fixed rates) until it gets inflation under control.

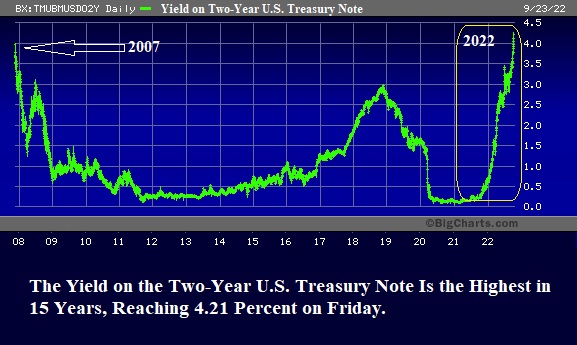

The yield on the two-year U.S. Treasury note is the highest in 15 years, closing Friday with a yield of 4.21 percent.

On Wednesday, the Fed raised its Fed Funds rate to 3 – 3.25 percent, hiking by ¾ point (75 basis points) for the third consecutive time this year (in June, July and September). Those hikes followed a ¼ point rate increase in March and a ½ point increase in May. The Fed’s actions effectively tripled short term interest rates in a span of six months – the most aggressive interest rate moves by the Fed in more than four decades.

In addition, according to the projections released by the Fed last Wednesday, it is planning to raise its Fed Funds interest rate (short-term overnight borrowing rate) to as much as 4.6 percent by next year. That would mean that it expects to hike rates by an additional 1.35 percent into next year.

At the end of August, Bespoke Investment Group released a study that found that the combined losses in stocks and bonds for investors was the worst in 50 years, because Wall Street financial advisors typically recommend a portfolio that is 60 percent stocks and 40 percent bonds. Both asset classes are not supposed to suffer sharp losses at the same time; one asset class is supposed to be a hedge against the other.

The 60-40 retiree portfolio is not the only portfolio feeling the pain. Hedge funds, trading houses, asset managers and Wall Street mega banks were not positioned for this type of aggressive monetary action by the Fed. Markets are starting to see large liquidations to stave off more pain.

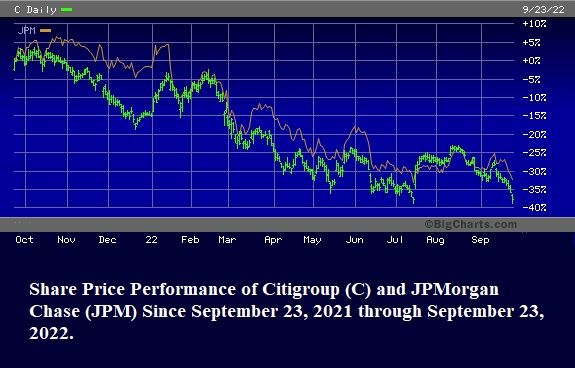

The share prices of two Wall Street mega banks, that rank number one and number two in terms of the largest derivative exposure, are tanking. Year-over-year, JPMorgan Chase has lost 32 percent of its market value while Citigroup has lost 38 percent. (See chart below.)

As of June 30, according to the Office of the Comptroller of the Currency (OCC), the bank holding companies of JPMorgan Chase had $56 trillion in notional derivatives (face amount) while Citigroup had $46 trillion. (Not to put too fine a point on it, but Citigroup blew itself up with derivatives in 2008 and only survived because the Fed secretly gave it $2.5 trillion in cumulative loans, at below market interest rates, from December 2007 through at least June 2010.) Those secret loan amounts were reported following a congressionally-mandated audit of the Fed by the Government Accountability Office.

JPMorgan Chase does not have a distinguished history when it comes to derivatives either – to put it mildly. In March 2013 the Senate Permanent Subcommittee on Investigations released a 300-page investigative report documenting that the bank had used depositors’ money from its federally-insured commercial bank to gamble in derivatives in London and lose at least $6.2 billion. This became known as the infamous “London Whale” scandal.

The ranking member of that Subcommittee, the late Senator John McCain, said this in his opening remarks at the related hearing:

“This investigation into the so-called ‘Whale Trades’ at JPMorgan has revealed startling failures at an institution that touts itself as an expert in risk management and prides itself on its ‘fortress balance sheet.’ The investigation has also shed light on the complex and volatile world of synthetic credit derivatives. In a matter of months, JPMorgan was able to vastly increase its exposure to risk while dodging oversight by federal regulators. The trades ultimately cost the bank billions of dollars and its shareholders value.

“These losses came to light not because of admirable risk management strategies at JPMorgan or because of effective oversight by diligent regulators. Instead, these losses came to light because they were so damaging that they shook the market, and so damning that they caught the attention of the press. Following the revelation that these huge trades were coming from JPMorgan’s London Office, the bank’s losses continued to grow. By the end of the year, the total losses stood at a staggering $6.2 billion dollars.

“This case represents another shameful demonstration of a bank engaged in wildly risky behavior. The ‘London Whale’ incident matters to the federal government because the traders at JPMorgan were making risky bets using excess deposits, portions of which were federally insured. These excess deposits should have been used to provide loans for main-street businesses. Instead, JPMorgan used the money to bet on catastrophic risk.”

One would think that in a representative democracy, such egregious behavior by taxpayer-subsidized mega banks would be swiftly and meaningfully reformed by an engaged Congress. Instead, the OCC reported on September 13 that just five commercial banks in the U.S. control $200.18 trillion in derivatives, or 86 percent of all derivatives held by all of the nation’s banks. In order of exposure to derivatives, those five bank holding companies are: JPMorgan Chase, Citigroup, Goldman Sachs, Bank of America and Morgan Stanley.

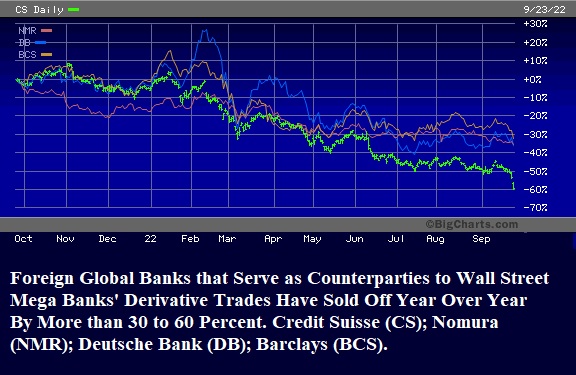

The global foreign banks that are counterparties to many of Wall Street mega banks’ derivative trades are also suffering major losses to their share prices. (See chart below.) This is starting to look very much like the domino effect that collapsed financial markets in 2008.

Intraday on Friday, Credit Suisse traded at an all time low of $4.04 in New York. It closed not much better at $4.14. To put that in perspective, a large Swiss, Global Systemically Important Bank (GSIB) is just $4.14 cents away from trading at zero market value.

Two other GSIBs are not doing much better: Deutsche Bank closed at $8.34 in New York on Friday while Barclays closed at $7.08. Nomura, a primary dealer at the New York Fed, also traded intraday on Friday at an all-time low of $3.325 before ticking slightly upward to $3.37 by the closing bell.

This is an absolutely frightening situation to anyone who knows anything about how the fragility of the banking system and its gluttonous appetite for derivatives played out in 2008. It was the largest financial collapse since the Great Depression.

But it would appear that Congress and the Fed are once again asleep at the switch. The Senate Banking Committee and the House Financial Services Committee hauled seven of the CEOs of the largest commercial banks in the U.S. before their respective committees last week. (Included were the CEOs of Citigroup and JPMorgan Chase.) There was not one mention by any Senator or House Rep about the dangers of derivatives or weak foreign counterparties to those derivatives. It is apparently a taboo subject.

Even oil is no longer a winning bet. With Russia’s savage war in Ukraine disrupting energy supplies, one would think that the price of oil would be rising. But U.S. domestic crude oil, known as West Texas Intermediate or WTI, has collapsed from a price of $130 in March to a closing price on Friday on the New York Merc (NYMEX) of $79.43 – a decline of 39 percent since March.

Oil is effectively telling markets that the chance that the Fed can engineer a soft landing (instead of a deep recession that will scuttle demand for energy) is little more than wishful thinking.