By Pam Martens and Russ Martens: September 30, 2020 ~

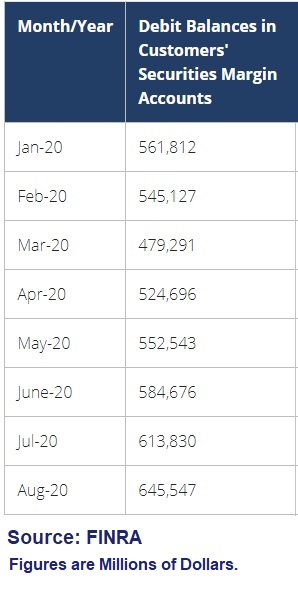

Conjuring up another era of “irrational exuberance,” data from Wall Street’s self-regulator, FINRA, shows that margin debt has grown by 15 percent since the end of January to a total of $645.5 billion as of August 31 of this year. That’s very close to the prior record of $668.9 billion set at the end of May 2018, according to the FINRA database.

Margin debt is created when investors borrow money against their stocks (or other marginable securities) held in a margin account at a brokerage firm. Typically, the margin loan is to enable the customer to buy more stock on a leveraged basis. Under the Federal Reserve’s Regulation T, investors may borrow a maximum of 50 percent of the purchase price of stocks from their brokerage firm. The remaining 50 percent of the price of the securities must be funded with cash. That’s known as Initial Margin or IM.

Then there is the ongoing Maintenance Margin requirement set by FINRA and the stock exchanges. Maintenance margin requires that the investor’s equity in the account not be less than 25 percent of the current market value of the securities in the account. If the equity value falls below 25 percent, the customer will be issued a “margin call” and required to deposit more cash or securities to reach the 25 percent equity level. If the customer fails to do this in a timely manner, the brokerage firm has the contractual right to liquidate enough securities, of their choosing, to regain the required level of equity in the account.

During periods of volatility, a brokerage firm can increase both Initial Margin and Maintenance Margin requirements. Interactive Brokers did just that last week according to CNBC, which reported the following:

“Interactive Brokers— which serves 876,000 broker accounts — typically has a 50% initial margin requirement and a 25% maintenance requirement. The new levels bring the initial requirement to 67.5% and a maintenance requirement of 33.75%.”

According to a letter sent to customers by Interactive Brokers, the change in policy grew out of a concern over the potential for increased volatility leading up to and following the presidential election.

Interactive Brokers is not alone in sensing a need to exercise caution. According to FIA, the trade organization for the futures, options and centrally-cleared derivatives markets, CME Group increased its margin requirements on the popular E-mini S&P futures contract dramatically in March as markets plunged in the U.S. The FIA wrote this about what it calls the “flagship of the equity complex” and “the most heavily traded equity index futures in the U.S.”

“The IM [Initial Margin] requirement began the year at $6,300 per contract and by March 2 it had risen to $6,600. Then the pandemic hit, and over the next three weeks CME’s clearinghouse increased the IM requirement six times as its margin model reacted to the extreme price movements during that time. By March 23, IM had been raised to $12,000 per contract, nearly double the amount at the beginning of the year.”

High margin debt is typically associated with a boom followed by a bust. Margin debt peaked ahead of the dot.com bust in 2000 and again in 2007, ahead of the Great Financial Crisis.

It’s an ominous sign that margin debt is still rising in the U.S. at a time when a headline is crossing the tape that “U.S. Economy Plunges 31.4 Percent in Second Quarter” (the revised number from a month ago); when food pantry lines are miles long; when 11 million Americans are still out of work; and during a time when there is sinking confidence in Washington’s ability to bring adults to the table to deal with the twin economic and health crises.