By Pam Martens and Russ Martens: April 7, 2020 ~

If it sounds ghoulish, it’s because it is ghoulish.

Some of the biggest banks on Wall Street have been intimidating their traders to come back to work despite an executive order from the Governor of New York State, Andrew Cuomo, ordering people to remain at home during the coronavirus outbreak unless they work for essential businesses like grocery stores, pharmacies and hospitals.

New York State, home to Wall Street, is now the epicenter of the coronavirus outbreak in the United States with 5,489 deaths as of today or 44 percent of all deaths from coronavirus in the entire United States.

Now, it turns out, while Wall Street traders have taken on greater health risks of catching the coronavirus by traveling to work on mass transit and working in a potentially contaminated building, some of the biggest banks will collect a death benefit should the employees die from the virus.

Wall Street banks own a form of life insurance called BOLI, short for Bank-Owned Life Insurance. The death benefit pays to the corporate owner of the policy, in this case the banks, not the employee or their family. Because it’s a life insurance policy, it has a lot of nice perks for the banks’ bottom line. The cash benefit of the policy builds up tax free while the policy is in force and the paid death benefit is free of federal income taxes. The bank is supposed to get the employee’s permission before taking out the policy but there is little evidence that employees know what they’re signing when a huge stack of papers is pushed in front of them on their hire date.

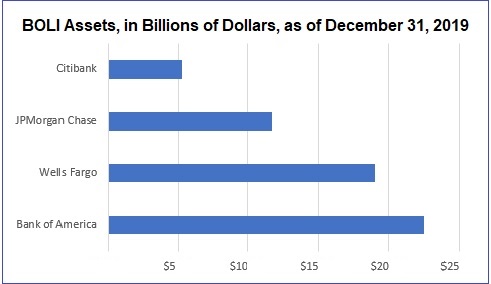

The amount of BOLI assets held by the banks is listed on Schedule RC-F on their Call Reports that are filed with federal regulators. As of December 31, 2019, four of the largest U.S. banks, JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank held a combined $58.44 billion in BOLI assets. The breakdown was as follows: Bank of America $22.55 billion; Wells Fargo $19 billion; JPMorgan Chase $11.66 billion; and Citibank $5.23 billion.

BOLI Assets at Largest Federally-Insured Banks as of December 31, 2019 (Source: FFIEC Call Reports)

But death benefits represent a large multiple to the amount of investments held in the policies. Experts suggest that $58.44 billion in BOLI assets could represent approximately $584 billion in future death benefits, or more than half a trillion dollars.

In 2003 and 2004, the Government Accountability Office (GAO) investigated these policies for Congress. The GAO found that some corporations kept the life insurance in force even after the employee had left the company – nullifying any ability to consider him or her a “key” to the business. The GAO wrote: “Unless prohibited by state law, businesses can retain ownership of these policies regardless of whether the employment relationship has ended.” The GAO also found that multiple companies held life insurance policies on the same individual.

Because Wall Street traders move frequently between Wall Street banks, you could have a situation where multiple banks collect death benefits on the same worker – who was intimidated into coming to work during a highly-transmissible pandemic, thus endangering both himself and his family.

In 2006, Congress passed the Pension Protection Act that included a section on these policies. Instead of outlawing BOLI and its corporate sibling, Corporate Owned Life Insurance (COLI), Congress grandfathered all of the millions of previously issued policies while making a few changes to tax and reporting rules.

One bedrock of insurance law that goes all the way back to the 19th Century is that a party must have an insurable interest in the life of another person in order to take out an insurance policy. The U.S. Supreme Court held in Warnock v. Davis in 1881 that “in all cases there must be a reasonable ground, founded upon the relations of the parties to each other, either pecuniary or of blood or affinity, to expect some benefit or advantage from the continuance of the life of the assured. Otherwise the contract is a mere wager, by which the party taking the policy is directly interested in the early death of the assured. Such policies have a tendency to create a desire for the event. They are, therefore, independently of any statute on the subject, condemned, as being against public policy.”

While it is highly questionable that rank and file employees are “key” to the success of a business, there is certainly no question that their contribution to the business ends when they terminate their employment. And yet, somehow, banks are allowed to collect death benefits on terminated workers right under the nose of State insurance regulators. According to our sources, banks run sweeps of the Social Security roster to keep tabs on former employees, find out who has died, and then file death benefit claims.

Wall Street On Parade previously filed a Freedom of Information Act request in 2014 with the Office of the Comptroller of the Currency (OCC), the federal regulator of national banks, to obtain granular data on BOLI at JPMorgan Chase. We were told by letter that the OCC had 450 pages of responsive material but it was not going to be released to us or the public. (See OCC Response to Appeal from Wall Street On Parade Re JPMorgan Banker Death Bets.)

In our May 12, 2014 appeal of the ruling by OCC, we made the following points:

“Since December of 2013, JPMorgan Chase has experienced five unusual deaths among current workers in their 30s and one unusual death of a 28-year old former worker whose brother currently works for JPMorgan and was cited by name in the U.S. Senate’s Permanent Subcommittee on Investigations’ report of JPMorgan’s London Whale trading debacle…

“Three of the six JPMorgan-related deaths cited in the article referenced above were allegedly from leaps from buildings in London, Hong Kong and Manhattan, respectively. None of JPMorgan’s peer banks — such as Citigroup, Morgan Stanley or Goldman Sachs – have publicly reported any suicides in the past six months as far as I’m aware. A 12-month review of public death notices among Citigroup employees revealed no cluster of deaths of young men in their 30s. (JPMorgan is reported to have 260,000 employees versus Citigroup’s reported 251,000.)…

“Why young men in their 30s are dying at JPMorgan but not at its peer banks is a matter of critical public health and safety concern. It is against public policy to keep the records secret. As the Chief Medical Examiner of Connecticut (where one of the deaths occurred) states on its web site: ‘Medicolegal investigations also protect the public health: by diagnosing previously unsuspected contagious disease; by identifying hazardous environmental conditions in the workplace, in the home, and elsewhere; by identifying trends such as changes in numbers of homicides, traffic fatalities, and drug and alcohol related deaths; and by identifying new types and forms of drugs appearing in the state, or existing drugs/substances becoming new subjects of abuse.’ ”

Our appeal was denied and more strange deaths at JPMorgan Chase ensued. (See related articles below.)

Last Friday, the Wall Street Journal reported that JPMorgan Chase had experienced a coronavirus outbreak on its trading floor with more than two dozen traders sick and dozens more in quarantine. Despite that, Bloomberg News reported today that traders are still being pressured to come back to work with one out of every five traders back on the trading floor.

Federal regulators clearly have no serious interest in reining in abuses on Wall Street. Perhaps Governor Cuomo will deem it timely to investigate this matter in a comprehensive way as a matter of protecting the health of all New Yorkers.

Related Articles:

Second Alleged Murder-Suicide by JPMorgan Worker in Seven Months

JPMorgan Managing Director Dies Suddenly; Has Links to Other JPM Deaths