By Pam Martens and Russ Martens: September 11, 2018 ~

Donald Regan, Former U.S. Treasury Secretary from Merrill Lynch

The reverberations from the New York Times OpEd last week, where an anonymous “senior official” in the Trump administration effectively described a coup taking place to stop the President’s mad impulses, are still shaking the nation.

But President Donald Trump, from the day he took office, has been little more than a titular figure head for the fossil fuels industry – with Koch Industries in particular calling the shots. The Trump administration took the unthinkable step of removing the United States from the Paris Climate Accord and there is breaking news that the Environmental Protection Agency will ease rules on methane gas emissions for oil and gas companies like Koch Industries.

The only real difference between this coup and past coups is that Koch Industries and its front group, Freedom Partners, are so much more in your face than Wall Street’s highly finessed but equally predatory cabal.

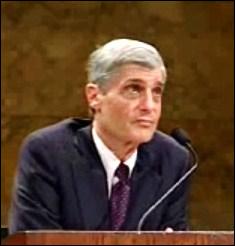

Americans have had hard evidence of the Wall Street cabal’s control of the President and much of the legislative branch throughout history. There is the famous video in Michael Moore’s movie, “Capitalism: A Love Story,” where Treasury Secretary Donald Regan whispers in President Ronald Reagan’s ear while he is delivering a speech and barks at him to “speed it up” — like Reagan is merely an actor on the payroll of an invisible but powerful authority. The President doesn’t seem surprised or annoyed but acts as if he is accustomed to taking orders from this man.

Donald Regan had been the Chairman and CEO of Merrill Lynch, the largest Wall Street brokerage firm in terms of stockbroker headcount throughout much of the last century. Regan first became Reagan’s Treasury Secretary and then his Chief of Staff and was viewed by many as the Acting President of the United States.

Robert Rubin, Former Treasury Secretary and Citigroup Board Chair

The Bill Clinton administration had Robert Rubin, a 26-year veteran of Goldman Sachs and former Co-Chairman, operating on behalf of Wall Street’s money trust – what it was called in the early 1900s. Rubin succeeded in pushing through the repeal of the depression era Glass-Steagall Act, which had kept the U.S. financial system safe for 66 years until its repeal in 1999, by barring banks holding Federally insured deposits from merging with speculating investment banks and brokerage firms. The financial system collapsed just nine years later in the same epic fashion as 1929 – when there also was no Glass-Steagall Act in place.

Rubin went directly from U.S. Treasury Secretary to become Chair of the Executive Committee at Citigroup in 1999 – a key beneficiary of the repeal of the Glass-Steagall Act. Rubin remained in that position until he stepped down in January 2009 as the bank was imploding. He collected over $120 million in compensation along the way. (In the leadup to the financial crisis, Rubin was briefly named Chairman of the Board of Directors of Citigroup in 2007.)

President Obama’s administration had multiple Wall Street operatives pulling the levers with very little pushback from Obama. Ron Suskind’s 2011 book, “Confidence Men,” includes the revelation that during the financial crisis President Obama told his Treasury Secretary Tim Geithner to “wind down” the failing Citigroup and Geithner ignored the directive. Suskind writes as follows:

“In early April, Obama’s economic team congregated in the Oval office for the morning briefing. All the key players were there, except Geithner. After a few moments, the president talked about a resolution plan for Citigroup as a key item in his arsenal, and wondered how close it was to completion. Christina Romer and Larry Summers glanced at each other. They had been talking for nearly a month about how the Treasury Department seemed to be ignoring the president’s clear, unequivocal orders involving Citigroup. Geithner and his team were moving forward with their own favored policy, the stress tests, but they had done virtually nothing about a plan to wind down Citigroup.”

The Non Profit Organization, Code Pink, Appeared on Multiple Occasions Holding Protest Signs Behind Tim Geithner as he Appeared Before Congress to Explain the Massive Bailouts of the Banks

Not only was Citigroup not unwound but it received $2.5 trillion in secret loans, at almost zero interest rates, from the Federal Reserve and without the awareness or approval of Congress. The loans were made through the Federal Reserve Bank of New York, the institution headed by Geithner prior to becoming Treasury Secretary. On top of the Fed’s secret loans, Citigroup also received the following in bailout money: $45 billion in capital from the U.S. Treasury; the Federal government guaranteed over $300 billion of Citigroup’s assets; the Federal Deposit Insurance Corporation (FDIC) guaranteed $5.75 billion of its senior unsecured debt and $26 billion of its commercial paper and interbank deposits.

The coup by Wall Street in the Obama administration was one of the greatest in history. After looting their banks from within through obscene compensation based on the manufacture of fraudulent instruments, not one Wall Street bank CEO was prosecuted by Obama’s Justice Department. The failure to prosecute came despite the Financial Crisis Inquiry Commission (FCIC) providing names to the DOJ where it felt there was the potential for criminal charges.

In September of 2016, Senator Elizabeth Warren sent a 20-page letter to the Inspector General of the Department of Justice, Michael E. Horowitz, asking for an investigation into why the DOJ had failed to indict any of the Wall Street executives that had been referred to it by the FCIC. In a separate letter, Warren asked then FBI Director James Comey for his related files. In her letter to the Inspector General of the DOJ, Warren wrote:

“A review of these documents conducted by my staff has identified 11 separate FCIC referrals of individuals or corporations to DOJ in cases where the FCIC found ‘serious indications of violations[s]’ of federal securities or other laws. Nine individuals were implicated in these referrals (two were implicated twice). The DOJ has not filed any criminal prosecutions against any of the nine individuals. Not one of the nine has gone to prison or been convicted of a criminal offense. Not a single one has even been indicted or brought to trial. Only one individual was fined, in the amount of $100,000, and that was to settle a civil case brought by the SEC.”

Nothing more was ever heard about Senator Warren’s inquiry so Wall Street On Parade filed a Freedom of Information Act (FOIA) request with the Justice Department on October 23, 2017. The Justice Department responded with a complete denial of any information on the FCIC referrals. (Read the full Justice Department response to Wall Street On Parade’s FOIA request here.)

As PBS’s Frontline revealed in 2013 in an investigation dubbed The Untouchables, Obama’s Justice Department was not using any of the standard arsenal that its criminal division has to investigate financial frauds. Martin Smith, the producer, states on air: “We spoke to a couple of sources from within the Criminal Division, and they reported that when it came to Wall Street, there were no investigations going on. There were no subpoenas, no document reviews, no wiretaps.”

Obama’s Attorney General, Eric Holder, and the head of the DOJ’s Criminal Division, Lanny Breuer, came from and returned to the big Wall Street law firm, Covington & Burling, the law firm that, according to a Federal judge, fronted for the illegal misdeeds of Big Tobacco for four decades. (Read our report here.)

You are likely wondering why, if the fossil fuels industry is cracking the whip at the Trump White House, there is also so much deregulation of Wall Street happening. That’s because Koch Industries also has a sprawling trading division called Koch Supply & Trading with offices in Houston, New York City, Wichita, Mexico City, London, Geneva, Singapore, and Shanghai. According to its website, it trades crude oil, refined products and derivatives, metals, interest rates and currency futures, among other things. That aligns its interests directly with the deregulation crowd on Wall Street.

Government of the people, by the people, for the people is not going to be returning anytime soon unless corporate money is outlawed from political campaign financing. The Republican Trump administration is today allowing the fossil fuels industry to destroy the environment while creating more oil billionaires just as the Wall Street Democrats greased the skids for the greatest financial collapse since the Great Depression by permitting the repeal of the Glass-Steagall Act, then watched as taxpayer bailout money was sluiced into multi-million dollar bonuses to implicated Wall Street executives.