By Pam Martens and Russ Martens: April 27, 2016

Goldman Sach’s Advertising Slogan Is “Progress Is Everyone’s Business.”

Back in 2010, with the public still numb from the epic financial crash and still in the dark about the trillions of dollars of secret loans the Federal Reserve had pumped into the Wall Street mega banks to resuscitate their sinking carcasses, Matt Taibbi penned his classic profile of Goldman Sachs at Rolling Stone, with this, now legendary, summation: “The world’s most powerful investment bank is a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.”

Historically, what smells like money to Goldman Sachs has been eight-figure money and higher. As recently as 2013, the New York Times reported that Goldman had a $10 million minimum to manage private wealth and was kicking out its own employees’ brokerage accounts if they were less than $1 million. Now, all of a sudden, Goldman Sachs Bank USA is offering FDIC insured savings accounts with no minimums and certificates of deposits for as little as $500 with above-average yields, meaning it’s going after this money aggressively from the little guy. What could possibly go wrong?

The last utterances we ever hoped to see bundled into a bank promotion were the words “Goldman Sachs” and “FDIC insurance” and “peace-of-mind savings.” But that’s what now greets one at the new online presence of Goldman Sachs Bank USA, thanks to the repeal of the Glass-Steagall Act in 1999, which allowed high-risk investment banks like Goldman Sachs to also own FDIC-insured, deposit-taking banks.

Goldman Sachs has been paying lots of fines for wrongdoing in the past few years, topping off at a cool $5 billion earlier this month for what the U.S. Justice Department characterized as “serious misconduct in falsely assuring investors that securities it sold were backed by sound mortgages, when it knew that they were full of mortgages that were likely to fail.” There was also the $550 million settlement in 2010 with the SEC for Goldman allowing the hedge fund run by billionaire John Paulson to secretly assist it in creating a portfolio designed to fail so Paulson could short it, while Goldman sold it to its own clients without divulging this pesky detail.

Students of Wall Street history may also recall that Goldman’s hubris leading up to the crash of 1929 played a role in why the Glass-Steagall Act of 1933 banned casino-like investment banks from getting near insured deposits. Prior to the ’29 crash, Goldman ran the Goldman Sachs Trading Company, a closed end fund (called a trust in those days). Goldman Sachs also offered that deal to the little guy at $104 a share. The fund appeared to investigators as a dumping ground for Goldman while also paying it a hefty management fee. The little guy who bought the shares at $104 a share at the top of the bull market was left with about a buck and change after the ’29 crash.

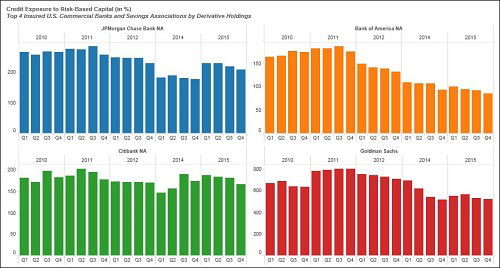

So why this generous move now by Goldman Sachs Bank USA to offer above average returns to the little guy? It likely has a lot to do with the chart below from the Office of the Comptroller of the Currency’s (OCC) December 31, 2015 report on the four largest banks based on derivatives exposure. According to the report, the credit exposure from derivatives versus the bank’s risk-based capital is as follows: JPMorgan Chase 209 percent; Bank of America 85 percent; Citibank 166 percent and Goldman Sachs (wait for it) – a whopping 516 percent.

Not to put too fine a point on it, but you might recall that one of the key promises of the Dodd-Frank financial reform legislation was that after the largest bank bailout in financial history in 2008, these derivatives were going to be pushed out of the insured bank into bank affiliates that would not endanger the taxpayer-backstopped deposits and force another monster taxpayer bailout in the next crisis. This became known as the “push-out rule” which could never seem to materialize into a hard and fast law. Then, in December 2014, Citigroup simply used its muscle to legislate the rule out of existence.

The Obama administration also promised that Dodd-Frank would put an end to these trillions of dollars of opaque derivatives being traded in the dark between firms as private contracts (over-the-counter). Dodd-Frank promised to bring them into the sunshine at central clearinghouses. But the December 2015 report from the OCC makes clear that’s just another failed promise, stating:

“In the first quarter of 2015, banks began reporting their volumes of cleared and non-cleared derivatives transactions, as well as risk weights for counterparties in each of these categories. In the fourth quarter of 2015, 36.9 percent of the derivatives market was centrally cleared.”

According to the OCC, as of December 31, 2015 there were $237 trillion in notional derivatives (face amount) at the 25 largest bank holding companies with the bulk of that amount on the books of the insured banks. That compares with $169 trillion on the books of the 25 largest bank holding companies at December 31, 2007, just prior to the implosions on Wall Street. This means there has been an explosive 40 percent increase in eight years when the Obama administration was supposed to be reining in risk on Wall Street.

When you hear Hillary Clinton repeatedly tell the public that she wants to continue along the same pathways as President Obama and that the restoration of the Glass-Steagall Act is not needed, let the image of Goldman Sachs Bank USA and its FDIC insurance logo and its $41 trillion in derivatives come to mind.

Four Largest Banks by Derivatives — Percentage Ratio of Credit Exposure to Risk-Based Capital: OCC Report Dated December 31, 2015