By Pam Martens: August 4, 2014

It’s so crazy that one’s first instinct is that it must be a spoof web site. It reads:

“A Citibank International Personal Bank FX Leveraged Loan Account can help you maximize the most of what you have. It allows you to borrow up to 5 times your deposit balance to trade in foreign currencies, so you may increase your potential investment power.” (The italics on deposit balance are ours.)

It turns out that this is a real Citibank offering, a real Citibank web site, and there is a similar deal being offered in Hong Kong by Citibank – one of Wall Street’s largest banks – a bank that appears hell bent on setting a Guinness World Record for the most screw ups in one decade.

Putting aside the fact that Citigroup, parent of Citibank, is under investigation for potentially helping to rig foreign currency trading with other global banks, there is the fact that Citigroup simply cannot afford another hit to its reputation – like inducing bank depositors to gamble with five times leverage in the highly complex foreign exchange markets.

A quick refresher is in order. Citigroup is the successor to National City Bank, blamed by Senator Carter Glass of Virginia in 1929 as playing a major role in causing the stock market crash which led to the Great Depression. In 2011, the Financial Crisis Inquiry Commission reported that Citigroup played a pivotal role in the 2008 financial crash, writing further that: “The Federal Reserve Bank of New York and other regulators could have clamped down on Citigroup’s excesses in the run-up to the crisis. They did not.”

In 1929, the business model worked like this: National City Bank made bad loans and packaged them up as securities and sold them to unwary investors. Last month, Citigroup paid a $7 billion fine for making bad loans and packaging them up as securities and selling them to unwary investors.

During the 2008 to 2010 financial crash, no other bank required as much financial support from the U.S. taxpayer as did Citigroup. The bank received $45 billion in equity infusions; over $300 billion in asset guarantees, and more than $2 trillion in below-market rate loans from the New York Fed. In addition to selling bad debt to investors, Citigroup pushed what it couldn’t sell into vehicles off its balance sheet. Tens of billions of that bad debt ended up back on its balance sheet, causing its insolvency in 2008.

The Glass-Steagall Act, enacted in 1933 with sponsors Senator Carter Glass and Congressman Henry Steagall, separated insured deposit banking from the speculative excesses of brokerage firms and investment banks. That legislative wall existed from 1933 to 1999 and protected our nation all that time from the kinds of abuses of the late 1920s on Wall Street. Nine years after its repeal, the U.S. financial system collapsed again from the exact same causes as in 1929.

No other bank played as great a role in the repeal of the Glass-Steagall Act than Citigroup. In 1998, Sanford Weill of Travelers Group and John Reed of Citibank had the temerity to announce the merger of their two firms into a new company to be called Citigroup, while the Glass-Steagall Act was still in force. Travelers at the time owned both the Smith Barney brokerage firm as well as the Salomon Brothers investment bank, holdings barred under the Glass-Steagall Act. The Alan Greenspan Federal Reserve approved the merger despite the law barring it and Congress dutifully repealed the Glass-Steagall Act the following year.

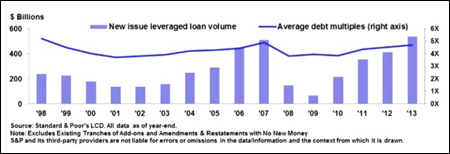

Today, leveraged loans are looking suspect. Reuters reported that leveraged loans hit an all-time high of $1.14 trillion in 2013 and may reach $1 trillion again this year.

Federal bank regulators typically describe leveraged loans along these lines:

• Where loan proceeds are used for buyouts, acquisitions, or capital distributions.

• A borrower is recognized in the debt markets as a highly leveraged firm, which is characterized by a high debt-to-net-worth ratio.

• Transactions when the borrower’s post-financing leverage, as measured by its leverage ratios (for example, debt-to-assets, debt-to-net-worth, debt-to-cash flow, or other similar standards common to particular industries or sectors), significantly exceeds industry norms or historical levels.

The concern has reached the level that Federal Reserve Chair, Janet Yellen, felt it necessary to brief the U.S. Senate on the issue in her testimony on July 15. Yellen stated:

“In some sectors, such as lower-rated corporate debt, valuations appear stretched and issuance has been brisk. Accordingly, we are closely monitoring developments in the leveraged loan market and are working to enhance the effectiveness of our supervisory guidance.”

Yellen’s alarm bell came less than a month after the Office of the Comptroller of the Currency, the regulator of national banks, sounded its own warning in its Semiannual Risk Perspective of June 25. The OCC wrote:

“U.S. syndicated leveraged loan issuance reached a record high in 2013 as the search for yield in the low interest rate environment drove an increase in risk appetite across institutional investors such as collateralized loan obligations (CLO) and retail loan funds. Issuers continued to take advantage of low interest rates, and competition among lenders for new business remained intense. Merger and acquisition loans had a strong year (32 percent of new issuance) and achieved the highest issuance volume since 2007, driven by higher corporate profit margins and business valuations. The average total-debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple for leveraged loans issued in 2013 rose to 4.7X, a level last exceeded in 2007. The combination of higher leverage, lower yields, tighter credit spreads, and weaker covenant protections provides ample evidence of increasing credit risk in the leveraged loan market…”

The report goes on to note that “the quality of underwriting in the syndicated leveraged loan market remains a supervisory concern.”

According to Antoine Gara, writing at TheStreet.com on April 8 of this year and citing data from a report issued by JPMorgan analyst Vivek Januja, “Among large banks, Citigroup has stepped up its leveraged loan issuance the fastest, with volumes rising 74% from 2011 to 2013, and LBO underwriting fees the fastest among large banks.”

Gara goes on to note that according to JPMorgan’s data, the number of loan downgrades is up sharply, exceeding upgrades in 2013 for the first time since 2009 with downgrades in the first quarter of 2014 running about double the pace of 2013.

Amidst this backdrop, the bank that became notorious for the size of its perpetual bailouts in 2008; the bank that lost 60 percent of its market value in just one week in 2008 due to a no-confidence vote from investors; the bank that is able to pay just one paltry penny a quarter as a dividend; the bank that Americans can thank for the repeal of the Glass-Steagall Act; the bank that is currently under multiple investigations on multiple continents; the behemoth that flunked its stress test with the Federal Reserve earlier this year because the Fed doesn’t have confidence it could withstand a major economic downturn – is selling leveraged loans to its bank depositors so they can gamble in the foreign exchange market with five times leverage.

If ever there was a mandate for the restoration of the Glass-Steagall Act, this is it.

Leveraged Loans Are Increasing and With Higher Leverage, Causing Concerns Among Regulators (OCC Graph Released in June 2014)