By Pam Martens and Russ Martens: April 22, 2019 ~

Ben Bernanke, Chairman of the Federal Reserve Board During the Financial Crisis

Based on data that Wall Street On Parade has newly compiled, there is a strong suggestion that the Federal Reserve conspired with at least three of the largest Wall Street firms to hide their teetering condition from the public during the financial crisis, despite the fact that these were all New York Stock Exchange listed companies with a duty to reveal material, adverse financial information to the public in a timely fashion.

If Maxine Waters wants to leave her mark in history as Chairman of the House Financial Services Committee, she will subpoena records from the Federal Reserve on its biggest and dirtiest bailout program, known as the Primary Dealer Credit Facility (PDCF). She and her colleagues must then demand answers from Fed witnesses during the hearing Waters has scheduled for May 16 at 10:00 a.m. The upcoming hearing is titled “Oversight of Prudential Regulators: Ensuring the Safety, Soundness and Accountability of Megabanks and Other Depository Institutions.”

The Federal Reserve is the prudential regulator of the largest Wall Street bank holding companies – three of which are only alive today because the Fed engaged in an unprecedented $5.7 trillion cash for trash operation with the three during the financial crisis. Until the public knows the truth about why the Fed bailed out the insolvent Citigroup – despite its mandate not to lend to an insolvent institution – and why it bailed out Morgan Stanley and Merrill Lynch, which were broker-dealers, not major commercial banks, there can be no confidence in the U.S. financial system.

There can be no trust or confidence because we strongly suspect that the reason for these unprecedented bailouts comes down to two words – derivatives and counterparties. These banks were all so intertwined as counterparties to each other’s insane levels of derivatives that the Fed had no clue what to do other than to save them all. That thesis would also explain why the Fed funneled trillions of dollars in cumulative loans to foreign banks – which also just happened to be derivative counterparties to the collapsing Wall Street firms. These interlocking concentrations of risk between derivative counterparties are just as dangerous today as they were in 2008 because the Fed has not forced the banks to follow the law and put these derivatives on exchanges or central clearing facilities. The majority of the derivatives remain as dark, private over-the-counter contracts between counterparties.

The Primary Dealer Credit Facility (PDCF) was put in place by the Fed on Sunday, March 16, 2008, the same date that JPMorgan Chase took over Bear Stearns to prevent its bankruptcy filing. PDCF lasted until February 1, 2010, according to the Federal Reserve.

In creating the PDCF, the Fed invoked its emergency lending powers under Section 13(3) of the Federal Reserve Act. The PDCF provided, cumulatively, $8.95 trillion in revolving overnight cash loans against what became by September of 2008, a pile of trash collateral whose details have yet to find their way into the public arena.

The Fed stated that the purpose of PDCF was to “improve the ability of primary dealers to provide financing to participants in securities markets, and to promote the orderly functioning of financial markets more generally.” The first thing that’s terribly wrong with that statement is that the Federal Reserve has no mandate to bail out “securities markets.” That’s why they’re called “free markets.” The other serious problem is that the primary dealers are not commercial bank units with Federally insured deposits which the Fed does have a mandate to provide liquidity to through its discount window. Primary dealers are broker-dealers who at the time were holding securities of highly questionable value.

To put the Fed’s action into historic perspective, up until March 16, 2008, there had only been 123 loans made by the Fed under the provisions of Section 13(3). All 123 loans were made during the Great Depression, from 1932 to 1936, and totaled $1.5 million. Section 13(3) was not invoked again until this Fed, under Chairman Benjamin Bernanke, turned it into a secret multi-trillion dollar money spigot beginning with PDCF. Between the PDCF and its multiple sibling bailout programs, the Fed engaged in 21,000 transactions cumulatively totaling more than $16 trillion from December 2007 through July 21, 2010. And that doesn’t include all of the bailout monies by a long shot. (See the Levy Economics Institute’s $29,000,000,000,000: A Detailed Look at the Fed’s Bailout by Funding Facility and Recipient.)

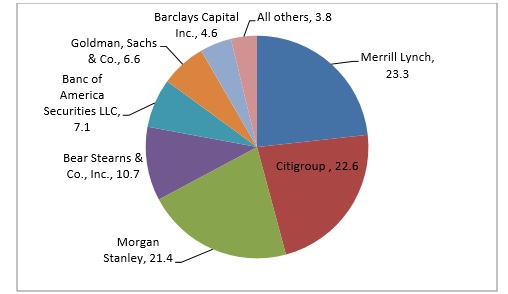

Just the PDCF alone was a staggering use of the Fed’s emergency lending powers. The program issued 1,376 loans that cumulatively totaled $8.95 trillion, of which Citigroup, Morgan Stanley and Merrill Lynch received $5.7 trillion or 64 percent of the total at a combined mean interest rate of 1.065 percent.

The PDCF should have become a serious target for Congressional investigation on September 14, 2008 when the Fed announced that it would allow the PDCF to accept equities (stocks) and junk bonds as collateral for loans.

Both stocks and junk bonds were in a state of free fall after the bankruptcy filing of Lehman Brothers on September 15, 2008. No responsible banker in the world would have accepted these as collateral for multi-billion-dollar loans that were continuously renewed. But the Fed did.

The Fed did something even more outrageous. While its governing rule for broker-dealers called Regulation T mandates that broker-dealers not lend more than 50 percent against stocks, the Fed was loaning as much as 90 percent against a hodgepodge of stocks and other questionable collateral under the PDCF. Consider the following noteworthy example.

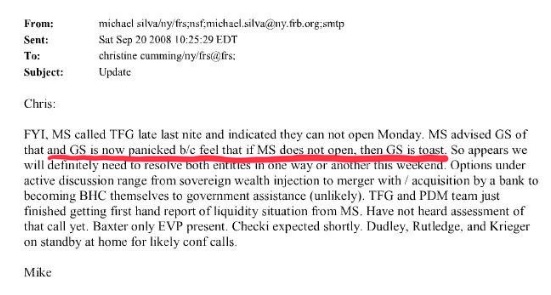

Last year the nonprofit watchdog, Better Markets, published the internal email below from Michael Silva, then Chief of Staff and Senior V.P. for the Executive Group at the Federal Reserve Bank of New York, which was the operator of the PDCF and most of the other Fed bailout programs. The email is dated Saturday, September 20, 2008 and explains that late on the Friday evening before, Morgan Stanley had called Timothy Geithner (TFG), the President of the New York Fed, and informed him that “they can not open Monday.”

Despite this warning about Morgan Stanley, this is what happened the very next business day, Monday, September 22, 2008. From the PDCF facility, the New York Fed gave Morgan Stanley a loan of $28.5 billion, not at an interest rate commensurate with a failing institution but at an interest rate for a top-notch credit risk. The Fed charged Morgan Stanley 2.25 percent and this is what it took as collateral for this loan: $11.6 billion in undefined equity instruments; $7.8 billion in “corporate market instruments” which the Fed defined at the time as “unsecured securities issued by private corporations” (about as clear as mud); $1.44 billion in junk bonds rated CAA/CCC or lower; $6.96 billion in “ratings unavailable” instruments; and the balance in supposedly higher rated instruments. The Fed made a loan to a self-confessed failing broker-dealer of $28.5 billion, representing 93 percent of the collateral it posted of $30.576 billion, and 91 percent of the collateral was of questionable merit. (You can download the Fed’s PDCF data here.) This kind of cash for trash would play out for the next six months at the PDCF.

Adding to the suspect nature of the PDCF operation, the Fed added another layer of darkness. On September 21, 2008 the Fed announced that it was going to extend credit to the London broker-dealer subsidiaries of Merrill Lynch, Morgan Stanley and Goldman Sachs. In November of that year, it extended the London affiliate arrangement to Citigroup. This program had an additional element of risk: the Fed agreed to accept collateral denominated in foreign currency, meaning that it now not only had risk from collateral of dubious value but it was also at risk from currency fluctuations.

The Fed had effectively become the risk-taker for Wall Street’s casino.

Citigroup was clearly an insolvent institution during the time the Fed had inserted a money feeding tube into the collapsing colossal. During the week of November 17, 2008, Citigroup’s stock lost 60 percent of its value – in one week. As of the close of trading on Friday of that week, the company had a market capitalization of $20.5 billion, which was $4.5 billion less than the $25 billion that the U.S. Treasury had pumped into the company under the TARP bailout. Notwithstanding that, the money spigot continued to flow to Citigroup. It received another $20 billion in an equity infusion from TARP. Altogether, Citigroup received $2.5 trillion in cumulative loans from the Fed under various programs; $45 billion in capital infusions from the U.S. Treasury under TARP; the Federal government guaranteed over $300 billion of Citigroup’s assets; the Federal Deposit Insurance Corporation (FDIC) guaranteed $5.75 billion of its senior unsecured debt and $26 billion of its commercial paper and interbank deposits. And yet, it was clearly insolvent, as Sheila Bair, the former Chair of the FDIC wrote in her memoir, Bull by the Horns:

“By November, the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

Under a provision in the Dodd-Frank financial reform legislation, the Fed was forced to release some details of its emergency lending programs on December 1, 2010. It became clear at that time that instead of functioning as a Lender of Last Resort to the Federally-insured depositor banks during the financial crisis so that credit could keep flowing to the real economy, the Federal Reserve functioned as the stock-and-junk-buyer-of-last resort to the Wall Street casino – violating anything remotely resembling its legislated emergency lending powers.

That part the public has heard about. What the public has not heard any meaningful details about is the fact that the PDCF’s $8.95 trillion in loans was collateralized by $2 trillion in stock of unknown corporations and quality; $491 billion was collateralized with junk bonds deep into junk status (rated CAA/CCC or lower); and another $1.5 trillion was collateralized with securities earmarked by the Fed as “Ratings Unavailable.”

Who was providing the lion’s share of this stock, junk bonds and “ratings unavailable” to acquire super cheap loans from the Fed? The same three banks that received the lion’s share of the loans: Citigroup, which received $2.02 trillion cumulatively in loans from the PDCF; Morgan Stanley which received $1.9 trillion; and Merrill Lynch, whose PDCF borrowing clocked in at $1.775 trillion, according to the Government Accountability Report (GAO) audit of the Fed’s bailout programs.

But here’s where the GAO study fails the test of an audit. The word “equities” is mentioned only three times in its audit – with no mention of why the Fed was allowed to accept equities (stocks) as collateral during a time of a collapsing stock market. There is also no clarity provided on why the Fed was accepting junk bonds at a time of collapsing junk bond prices. The GAO audit does offer this very modest concern about the PDCF’s collateral:

“For PDCF collateral data, the lack of sufficiently detailed data documentation for some key pricing variables made it difficult to draw reliable conclusions about whether assets pledged to the PDCF as collateral were priced consistently.”

The GAO audit, which was released on July 21, 2011 – one year after the tepid Dodd-Frank financial reform legislation was already the law of the land, came about as a result of an amendment to the Dodd-Frank financial reform legislation inserted by Senator Bernie Sanders. There is no breakdown of what these stocks being used as collateral were all about. Were they large cap stocks listed on the New York Stock Exchange? Were they over-the-counter small cap stocks of companies about to go bust? Was it the stock of the Wall Street banks themselves? And what happened to the stock? How long did it sit on the Fed’s balance sheet? Is it still there now?

It’s time for the House Financial Services Committee to force the Fed to come clean with the American people – nothing less than the safety and integrity of the U.S. financial system hangs in the balance.

PDCF’s Largest Borrowers. Source: Levy Economics Institute Using Fed Data

Related Articles:

Bernanke, Geithner, Paulson: The Fed Should Be Able to Make Secret Trillion Dollar Loans Again

The Chorus Grows for the Fed to Buy Up Stocks in the Next Wall Street Crisis

Fed Chair Bernanke Held 84 Secret Meetings in the Lead Up to the Wall Street Collapse

Yes, James Freeman, We Do Know How Bad the Federal Reserve Is