By Pam Martens and Russ Martens: May 3, 2016

On April 21, Wall Street On Parade reported that the U.S. government (also known as the U.S. taxpayer) was on the hook for potentially tens of billions of dollars in derivative losses at Freddie Mac and Fannie Mae – the two companies the government put under conservatorship during the Wall Street financial collapse of 2008. (See related article below.)

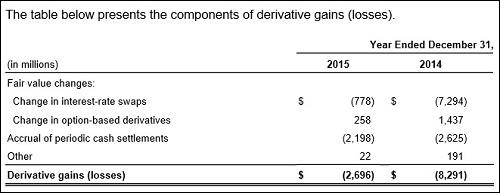

This morning, Freddie Mac is adding further angst to this potential derivatives blowup scenario by reporting that it lost $4.56 billion in its derivatives portfolio in just the first three months of this year – a stunning 90 percent increase over what it lost in derivatives in the first quarter of 2015. That brings its derivative losses for all of 2014, 2015 and the first quarter of 2016 to $15.54 billion. (See chart below.) This is certain to bring gasps from some members of Congress.

While positive net income has offset the derivative losses in recent years, making Freddie Mac profitable overall, the company said in its press release this morning that it had an overall $354 million net loss for the first quarter of this year, meaning the derivative losses fully wiped out the earnings it makes from its portfolio of mortgages and other sources of positive income such as the fees it collects for guaranteeing mortgages.

Despite acknowledging that its net worth is a mere $1 billion, Freddie Mac said in its press release that it would not be drawing further from the U.S. Treasury at this time. Under the conservatorship arrangement, the U.S. Treasury has already infused over $187.5 billion into Freddie Mac and Fannie Mae. But according to a government audit released by the Government Accountability Office (GAO) on February 25 of this year, the U.S. Treasury has committed taxpayers to an additional $258.1 billion that Freddie Mac and Fannie Mae can draw down.

The original conservatorship plan called for the government to receive senior preferred stock in both companies that would pay a 10 percent dividend. (Since both were insolvent at the time, the rate was set high as it would be for a junk-rated company.) After years of the 10 percent dividend being paid by additional draw downs of money from the Treasury (sort of like taking out a home mortgage and asking the same bank to advance you the money to pay the mortgage interest instead of being declared in default), in August 2012 the Treasury amended its agreement. Under the new terms, beginning on January 1, 2013, Freddie Mac and Fannie Mae began paying the Treasury all of its net earnings above and beyond a capital cushion. (This has become known as the “net worth sweep”.)

In addition to the Senior Preferred shares, the U.S. Treasury also received a warrant to purchase, for a nominal price, 80 percent of the common stock outstanding at the time the warrant is exercised. The Treasury Department has not yet exercised that warrant and speculators are having a heyday engaging in speculative trading in the over-the-counter stocks of both Freddie Mac and Fannie Mae, guessing on what might happen in the future. (Lawyers are also challenging the 2012 amendment in court as being unfair to other stockholders.) The U.S. Treasury has the right to exercise the warrant, in whole or in part, at any time through September 7, 2028.

In Freddie Mac’s 10K filing with the Securities and Exchange Commission for the full year of 2015, the company conceded that “Our ability to access funds from Treasury under the Purchase Agreement is critical to keeping us solvent.”

The massive year over year increase in Freddie Mac’s derivative losses suggest that there is more here than meets the eye. It also raises the question as to whether the Federal Housing Finance Agency (FHFA), Freddie and Fannie’s official Federal conservator and supervisor, is on top of what’s embedded in these derivative contracts.

According to Freddie Mac’s 10K filed with the SEC, these are just some of the risks it faces going forward:

“Yield Curve Risk

“Yield curve risk is the risk that changes in the level and shape of the yield curve, such as a level change, or a flattening or steepening, will adversely affect our economic value. Our yield curve risk under a specified yield curve scenario is reflected in our PMVS-YC disclosure.

“A change in the level of interest rates (represented by a parallel shift of the yield curve, all else constant) exposes our assets and liabilities to risk, potentially affecting future expected cash flows and their present values.

“Similarly, changes in the shape or slope of the yield curve (often reflecting changes in the market’s expectation of future interest rates) exposes our assets and liabilities to risk, potentially affecting expected future cash flows and their present values.

“Volatility Risk

“Volatility risk is the risk that changes in the market’s expectation of the magnitude of future variations in interest rates will adversely affect our economic value.

“We are exposed to volatility risk in both our mortgage-related assets and liabilities, especially in instruments with embedded options.

“Spread Risk

“Spread risk is the risk that yields in different asset classes may not move together and may adversely affect our economic value.

“This risk arises principally because interest rates on our mortgage-related investments may not move in tandem with interest rates on our financial liabilities and derivatives, potentially affecting the effectiveness of our hedges.

“We are continually exposed to significant spread risk, also referred to as mortgage-to-debt OAS risk, arising from funding mortgage-related investments with debt securities.

“We also incur spread risk when we use LIBOR- or Treasury-based instruments in our risk management activities.

“We are exposed to spread risk arising from the difference in time between when we commit to purchase a multifamily mortgage loan and when we securitize the loan. During this time, spreads can widen, causing losses due to changes in fair value. We also have spread risk on the K Certificates we hold in our mortgage-related investments portfolio.”

If all of this is Greek to you, it may well be Greek to Freddie Mac’s Board of Directors and its overseers at FHFA. Let’s face it, it wouldn’t be the first time Wall Street banks have played their derivative counterparties for a fool. Think about the government’s bailout of AIG and who ended up with more than half the dough from that bailout. Or how about that Merrill derivatives salesman that greased the skids for Orange County, California going bankrupt?

In a March 2015 report from the New York Fed, it conceded who the government was worrying about when it took over Freddie and Fannie – a full week before Lehman Brothers went under. The New York Fed wrote:

“Fannie Mae and Freddie Mac held large positions in interest rate derivatives for hedging. A disorderly failure of these firms would have caused serious disruptions for their derivative counterparties.”

Who are their derivative counterparties? The too-big-to-fail banks on Wall Street of course.

Freddie Mac’s Derivative Gains and Losses. Source — 2015 10K Filed With the SEC

Related Article:

U.S. Government Is Now a Major Counterparty to Wall Street Derivatives

Related Documents:

First Amendment to Freddie Mac’s Senior Preferred Stock Purchase Agreement with Treasury (May 2009)

Freddie Mac’s Senior Preferred Stock Purchase Agreement with Treasury (September 2008)