By Pam Martens and Russ Martens: August 12, 2024 ~

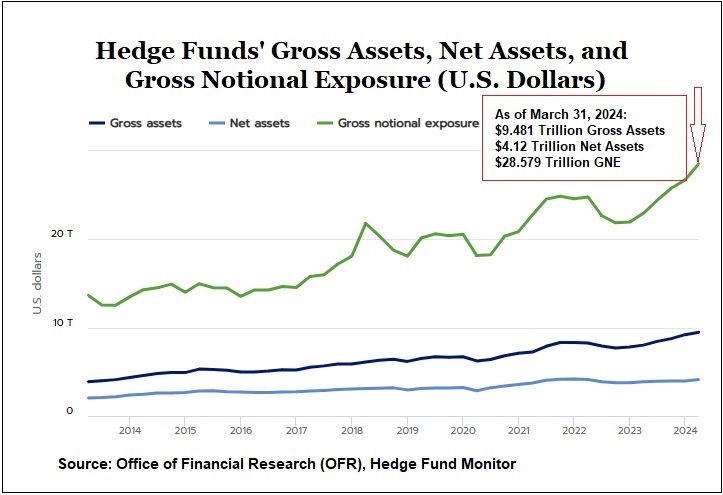

According to a report at the U.S. Treasury’s Office of Financial Research (OFR), the Gross Notional Exposure at hedge funds has skyrocketed by 24.5 percent in the span of one year: from $22.946 trillion on March 31, 2023 to $28.579 trillion on March 31, 2024. (Run your cursor along the top green line at this link to observe the stunning growth in hedge fund exposures despite the banking crisis in the spring of 2023 when the second, third and fourth largest banks blew up.)

Gross Notional Exposure (GNE) is defined by OFR as “the sum of the absolute value of long and short exposures, including those on and off the balance sheet.”

The OFR was created under the Dodd-Frank financial reform legislation of 2010 to keep bank and market regulators informed of growing risks, in the hope of preventing another financial crisis like that of 2007-2010 from occurring.

Unfortunately, Wall Street’s lobbying, bullying and regulatory capture has exponentially outstripped the clout of the OFR. As a result, all that the public can do is read about the potentially catastrophic risks inherent on Wall Street today at the OFR’s website and wonder when the next blowup and Fed bailout will occur. (See our report: Former New York Fed Pres Bill Dudley Calls This the First Banking Crisis Since 2008; Charts Show It’s the Third.)

The OFR carries this mild statement as to what can go wrong at over-leveraged hedge funds: “…Leveraged hedge funds are dependent on creditors’ willingness and ability to continue to lend. Further, declines in collateral and asset values can lead to margin calls that require hedge funds to tap their liquid assets….”

Allow us to fill in the gaps in that statement. The largest megabanks on Wall Street – which since the repeal of the Glass-Steagall Act in 1999 are also allowed to own taxpayer-backstopped, federally-insured, deposit-taking banks – are the major source of providing that leverage to hedge funds. This hedge fund lending and servicing operation at the megabanks is given the benign title of “Prime Broker.”

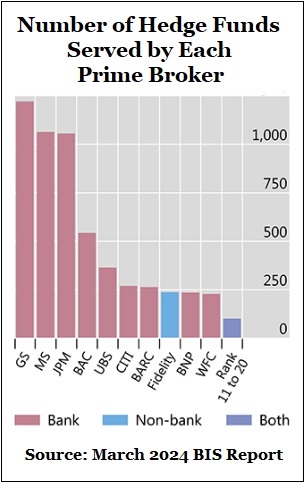

According to a March 4 report from the Bank for International Settlements, the Prime Broker operations of Goldman Sachs (GS), Morgan Stanley (MS), and JPMorgan Chase (JPM) (all U.S. financial institutions which own federally-insured banks) were each servicing more than 1,000 hedge funds as of 2022. (See chart to the right from that report.)

According to a March 4 report from the Bank for International Settlements, the Prime Broker operations of Goldman Sachs (GS), Morgan Stanley (MS), and JPMorgan Chase (JPM) (all U.S. financial institutions which own federally-insured banks) were each servicing more than 1,000 hedge funds as of 2022. (See chart to the right from that report.)

Making this situation even more outrageous, each of these megabanks has a notorious reputation for mismanaging risk in their relationships with hedge funds in the past.

Let’s start with Morgan Stanley. During the 2008 financial crisis, Morgan Stanley owned a hedge fund called FrontPoint Partners, which was shorting subprime collateralized debt obligations (CDOs) filled with subprime residential mortgages. To be more precise, FrontPoint was hoping to profit on American homeowners being unable to pay their tricked-up mortgages and being thrown out on the street.

FrontPoint was also gleefully betting that the biggest banks on Wall Street would collapse. Michael Lewis writes in his bestselling book, The Big Short, that FrontPoint was shorting “Bank of America, along with UBS, Citigroup, Lehman Brothers, and a few others.” Lewis notes that “They weren’t allowed to short Morgan Stanley because they were owned by Morgan Stanley, but if they could have, they would have.”

And while Morgan Stanley’s own hedge fund, FrontPoint, was shorting subprime and the Wall Street banks, the Federal Reserve was infusing $16 trillion cumulatively in secret revolving loans to shore up the Wall Street banks, including $2.04 trillion in revolving loans to Morgan Stanley. (See Table 8 of the GAO report here.)

A footnote in the GAO report tells us this: “Morgan Stanley funds include TALF borrowing by funds managed by FrontPoint LLC, which was owned by Morgan Stanley at the time TALF operated.” TALF was one of the numerous emergency lending programs created by the Fed during the 2007-2010 financial crisis.

According to Fed data, FrontPoint received over $4 billion of Morgan Stanley’s $9.3 billion in TALF loans. While Morgan Stanley was the second largest recipient of total Fed emergency lending programs, it was the number one borrower under TALF with 43 percent of those funds going to FrontPoint.

How risky was Morgan Stanley at the time the Fed was flooding it with emergency lending? According to the Financial Crisis Inquiry Commission report on the 2007-2010 crisis, both Lehman Brothers (which went bankrupt) and Morgan Stanley had reached leverage ratios of 40:1 by the end of 2007 – “meaning for every $40 in assets, there was only $1 in capital to cover losses. Less than a 3% drop in asset values could wipe out a firm.”

Next, let’s consider how Goldman Sachs was interacting with a hedge fund going into the Wall Street collapses of 2008.

John Paulson is the founder of the hedge fund Paulson & Co. On April 16, 2010, the Securities and Exchange Commission announced formal charges against Goldman Sachs pertaining to the infamous 2007 ABACUS deal: “The SEC alleges that one of the world’s largest hedge funds, Paulson & Co., paid Goldman Sachs to structure a transaction in which Paulson & Co. could take short positions against mortgage securities chosen by Paulson & Co. based on a belief that the securities would experience credit events.” Translation, Paulson helped Goldman select dodgy investments that were likely to default or receive credit downgrades and then made easy bets that they would.

The SEC complaint goes on: “…after participating in the portfolio selection, Paulson & Co. effectively shorted the RMBS [Residential Mortgage Backed Securities] portfolio it helped select by entering into credit default swaps (CDS) with Goldman Sachs to buy protection on specific layers of the ABACUS capital structure. Given that financial short interest, Paulson & Co. had an economic incentive to select RMBS that it expected to experience credit events in the near future. Goldman Sachs did not disclose Paulson & Co.’s short position or its role in the collateral selection process in the term sheet, flip book, offering memorandum, or other marketing materials provided to investors.”

According to the SEC’s complaint, Paulson & Co. paid Goldman Sachs approximately $15 million for structuring and marketing ABACUS. By October 2007, 83 percent of the bonds in the portfolio had been downgraded and 17 percent were on negative watch. By Jan. 29, 2008, 99 percent of the portfolio had been downgraded.

The SEC estimated that investors lost more than $1 billion in the ABACUS deal while Paulson profited by approximately the same amount.

On July 15, 2010, the SEC announced that Goldman Sachs would pay $550 million to settle its ABACUS charges. Fabrice Tourre, a young Goldman investment banker involved in the deal, was the only person to face a civil trial. No one was criminally prosecuted. John Paulson walked free – ostensibly because he didn’t actually sell the product or misrepresent it to investors – he just stacked the deck against investors and, apparently, that’s not a big deal in the eyes of the SEC.

As one more example of the dystopian world in which we now live, there were media reports in March that Donald Trump was considering John Paulson as his Treasury Secretary if he won the presidential election in November.

And then there is JPMorgan Chase – the poster boy for everything that is wrong with the U.S. financial system today. JPMorgan Chase has the distinction of admitting to five criminal felony counts brought by the U.S. Department of Justice since 2014 while still being allowed by its regulators to grow wildly in scope and size.

Under the Dodd-Frank financial “reform” legislation, banks were required to relinquish their ownership of hedge funds. But instead, JPMorgan Chase retained its stake in the hedge fund, Highbridge Capital Management, whose sale to the bank was brokered by the sex trafficker of children, Jeffrey Epstein, who remained a pampered client at the bank for more than 15 years, despite his serving jail time and being placed on a sex-offender registry.

The now settled federal lawsuit brought by the Attorney General of the U.S. Virgin Islands alleged that JPMorgan Chase had “actively participated” in Epstein’s sex trafficking. A Memorandum of Law arguing for partial summary judgment in the case, makes the following points:

“Even if participation requires active engagement…there is no genuine dispute that JPMorgan actively participated in Epstein’s sex-trafficking venture from 2006 until 2019. The Court found allegations that the Bank allowed Epstein to use its accounts to send dozens of payments to then-known co-conspirators [redacted] provided excessive and unusual amounts of cash to Epstein; and structured cash withdrawals so that those withdrawals would not appear suspicious ‘went well beyond merely providing their usual [banking] services to Jeffrey Epstein and his affiliated entities’ and were sufficient to allege active engagement.”

The U.S. Virgin Islands’ attorneys cite to internal emails at JPMorgan Chase showing that employees at the bank were aware of Epstein’s “[c]ash withdrawals … made in amounts for $40,000 to $80,000 several times a month” while also being aware that Epstein paid his underage sexual assault victims in cash.

JPMorgan Chase’s involvement in the Epstein sex trafficking ring was also alleged in a class action lawsuit against JPMorgan Chase brought by lawyers David Boies and Bradley Edwards on behalf of Epstein’s victims. (JPMorgan Chase paid $290 million to settle that case last year.) At a March 13, 2023 court hearing in the case, Boies argued in open court that JPMorgan Chase had used a private jet owned by its hedge fund, Highbridge Capital Management, to transport girls for Epstein’s sex trafficking operation. A January 13, 2023 amended complaint filed by Boies’ law firm provided the following details on that allegation:

“As another example of JP Morgan and [Jes] Staley’s benefit from assisting Epstein, a highly profitable deal for JP Morgan was the Highbridge acquisition.

“In 2004, when Epstein’s sex trafficking and abuse operation was running at full speed, Epstein served up another big financial payday for JP Morgan.

“Epstein was close friends with Glenn Dubin, the billionaire who ran Highbridge Capital Management.

“Through Epstein’s connection, it has been reported that Staley arranged for JP Morgan to buy a majority stake in Dubin’s fund, which resulted in a sizeable profit for JP Morgan. This arrangement was profitable for both Staley and JPMorgan, further incentivizing JP Morgan to ignore the suspicious activity in Epstein’s accounts and to assist in his sex-trafficking venture.

“For example, despite that Epstein was not FINRA-certified, Epstein was paid more than $15 million for his role in the Highbridge/JP Morgan deal.

“Moreover, Highbridge, a wholly-owned subsidiary of JP Morgan, trafficked young women and girls on its own private jet from Florida to Epstein in New York as late as 2012.”

There appears to be little to no guardrails or moral compass on Wall Street in its pursuit of profits. That will doom both it and the U.S. economy if federal regulators continue to stand down.