Deposits at 25 Largest U.S. Commercial Banks

By Pam Martens and Russ Martens: May 8, 2023 ~

Since the banking crisis began making headlines at expensive media real estate, the narrative has been that deposits are fleeing the small commercial banks and flooding into the biggest banks that are perceived as too-big-to-fail and thus offer a safer venue for deposits.

Because these mega banks are the same ones that the Fed has been bailing out since the financial crisis of 2008, that narrative requires believing that our fellow Americans are dumber than a stump.

We decided to check out that narrative for ourselves. Not only is that scenario wrong, but it is so decidedly wrong, and it’s so easy to get the accurate figures, that from where we sit it looks like there might have been an agenda by someone to harm smaller banks. (Since it’s short sellers who have benefited to the tune of more than $7 billion from this misinformation, the Securities and Exchange Commission should find out who the public relations firms are who placed this erroneous information, and who paid them.)

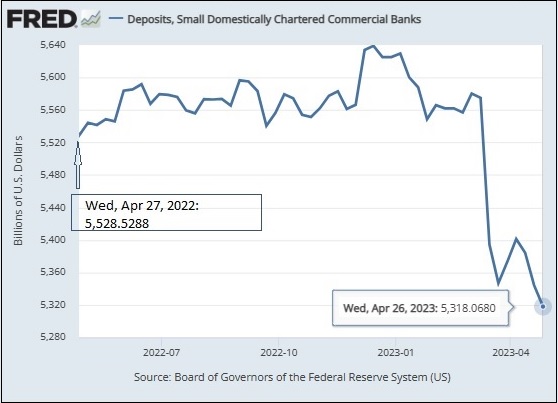

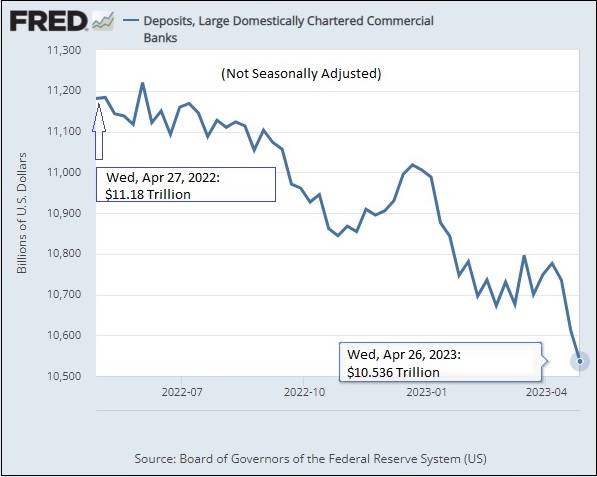

Each Friday, at approximately 4:15 p.m., the Federal Reserve (“the Fed”) releases its H.8 report showing the assets and liabilities of commercial banks in the United States. Monthly deposit data is included going back one year, as well as deposit data for each of the last four weeks. Data is also broken down by the 25 largest banks and the approximate 4,000 small banks. Equally helpful, the folks at the St. Louis Fed make it possible to chart much of that H.8 data via its FRED charting tools. (See charts above and below.) The 25 largest banks in the U.S. lost a total of $644 billion in deposits between April 27, 2022 and April 26, 2023.

The three largest banks in the U.S., as measured by deposits, are JPMorgan Chase, Bank of America and Wells Fargo. Between April 27, 2022 and April 26, 2023, JPMorgan Chase lost $184 billion in deposits; Bank of America lost $162 billion; and Wells Fargo lost $118.7 billion, for a combined loss in deposits of $464.7 billion — representing 72 percent of the decline in deposits at the 25 largest banks. (That’s a crystal clear indication of just how dangerously concentrated banking has become in the U.S.)

The deposit losses at JPMorgan Chase, Bank of America and Wells Fargo are more than twice what the 4,000 small banks lost in total during the same period. Their combined loss in deposits was just $210 billion. (See chart below.)

Bank of America and Wells Fargo not only lost those large deposit sums on a year-over-year basis, but both banks saw deposits fall during the past five quarters, including the quarter ending March 31, 2023 when headlines were declaring that they were seeing big inflows of deposits as a result of the banking crisis. JPMorgan Chase lost deposits in each of the quarters in 2022 and then saw a small increase in deposits in the first quarter of this year – likely from all of those misleading headlines. (This information is easily obtained from the financial statements the firms file publicly with the SEC.)

To give you an idea of just how pervasive this false narrative has been about the big banks sloshing around in all those deposits fleeing the small banks, as recently as April 28 the Bloomberg columnist, John Authers, wrote a column that was syndicated to the Washington Post – likely to be read by a large number of members of Congress. In the article, Authers included this nugget:

“This summary from the Canadian firm Palos Management explains neatly why the bigger banks are still OK:

“The first quarter’s performance of the big four was consistent with a broad consensus that the big banks have capitalized on massive depositor inflows, clearly related to the well-documented liquidity stresses facing their smaller, regionally based brethren. This should come as no surprise. The panic-fueled depositor exodus from the smaller banks to the larger ‘too big to fail’ banks is simply a rational decision. Protection of capital rules.”

Why would a journalist rely on unverified deposit data from a Canadian firm when the deposit data is readily available from the banks’ own filings with the SEC as well as in the Fed’s H.8 weekly releases?