By Pam Martens and Russ Martens: July 5, 2022 ~

The Department of Commerce’s Bureau of Economic Analysis (BEA) will release its advance estimate for U.S. Gross Domestic Product (GDP) for the second quarter of 2022 at 8:30 a.m. on July 28. All eyes on Wall Street will be glued to that number as a gauge of where stock prices are headed.

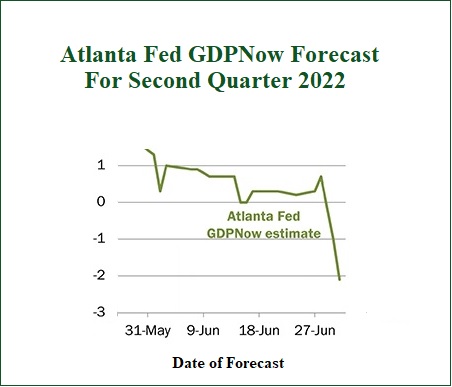

As of this morning, the highly respected number crunchers at the Atlanta Fed’s GDPNow model are forecasting a contraction of -2.1 percent in U.S. economic growth in the second quarter. (That’s the real GDP growth/seasonally adjusted annual rate.) The Atlanta Fed’s GDPNow modelers will update their forecast five more times, based on additional economic data releases, before the advance estimate for second quarter GDP is officially released by the BEA on July 28.

GDP contracted at a -1.6 percent annualized rate in the first quarter. Two quarters of negative GDP growth has been the criteria on Wall Street for characterizing the economy as in recession. The definition of recession at the National Bureau of Economic Research (NBER) is “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” NBER’s Business Cycle Dating Committee is the official word on classifying when a U.S. recession has begun and ended.

If there is a meaningful contraction in the U.S. economy, Wall Street trading house, Morgan Stanley, sees the potential for the stock market, as measured by the S&P 500, to sink to as low as 3,000. As of Friday’s close, the S&P 500 stood at 3825.33, which was already a loss of 19.7 percent year-to-date.

The S&P 500 closed out last year at 4,766.183. If it were to reach 3,000 this year, that would be a year-to-date loss of 37 percent – and that could actually be the good news compared to what is likely to happen to Nasdaq if there is a significant GDP contraction.

The Nasdaq composite index closed out last year at a reading of 15,644.97. The Nasdaq closed Friday at 11,127.85 – a year-to-date decline of 29 percent. A GDP contraction would be likely to hit the Nasdaq much harder than the S&P 500 because the Nasdaq is stuffed with tech companies trading at lofty price-to-earnings multiples; numerous companies with negative earnings histories; many companies paying no dividends; and companies which should have never been brought to public markets in the first place. (See our report: SEC Chair Jay Clayton Left Markets in the Biggest Mess Since 1929.)

According to a study (see Table 9) released last year by Professor Jay Ritter in the Department of Finance at the University of Florida, there were more traditional IPOs with negative earnings issued in the four years of the Trump administration than at any time in the last 40 years. (The study only goes back to 1980.)

The study focuses on traditional IPOs and eliminates the following: “IPOs with an offer price below $5.00 per share, unit offers, ADRs, closed-end funds, partnerships, acquisition companies [SPACs], REITs, bank and S&L IPOs, and firms not listed on CRSP [Center for Research in Security Prices] within six months of the offer date are excluded.”

According to Ritter’s research, 77 percent of the traditional IPOs issued in 2017 had negative earnings; 81 percent in 2018; 77 percent in 2019; and 80 percent in 2020.

We could find no other era in the last 40 years that even came close to this hubristic record. For example, in the four years leading up to the historic dot.com crash in 2000, the percentage of IPOs with negative earnings looked like this: 36 percent in 1997; 46 percent in 1998; 76 percent in 1999; and 81 percent in 2000. That four-year average comes to 59.75 percent versus the four-year average from 2017 through 2020 of 78.75 percent of traditional IPOs coming to market with negative earnings.

Morgan Stanley is not the only trading house on Wall Street that is making bold predictions of what might lie ahead for markets. In a communique on July 1, analysts at JPMorgan Chase predicted that “global oil prices could reach a ‘stratospheric’ $380 a barrel if US and European penalties prompt Russia to inflict retaliatory crude-output cuts….”

At the other end of predictions on the price of oil, Citigroup analysts say that crude oil could plunge to $65 a barrel by year end if a deep recession hits.

As of 8:16 a.m. (ET) this morning, U.S. domestic crude oil, West Texas Intermediate, was trading at $108.74 a barrel (front month futures market).

JPMorgan Chase and Citigroup are two of the four largest derivatives traders on Wall Street. Since they are taking wildly divergent views of what might happen in the oil market, one must factor in the possibility that they are simply talking their book.