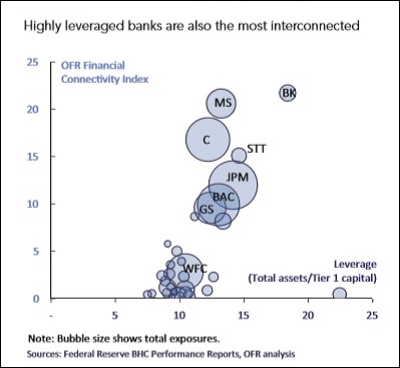

2015 Office of Financial Research Report: Wall Street Mega Banks Are Highly Interconnected: Stock Symbols Are as Follows: C=Citigroup; MS=Morgan Stanley; JPM=JPMorgan Chase; GS=Goldman Sachs; BAC=Bank of America; WFC=Wells Fargo.

By Pam Martens and Russ Martens: January 25, 2022 ~

The Office of Financial Research (OFR) is the federal agency created under the Dodd-Frank financial reform legislation of 2010. Its role is to provide early warnings to U.S. bank regulators and the public of systemic risks that threaten U.S. financial stability, so that another 2008-style Wall Street crisis can never again devastate the U.S. economy.

The OFR was doing an outstanding job of sounding alarm bells until the Trump administration gutted the agency. The Biden administration has clearly not done enough to restore the integrity of the office.

Consider the research report that was released by the OFR on July 12 of last year, which we just discovered yesterday. The report is titled: “Counterparty Choice, Bank Interconnectedness, and Systemic Risk.” The researchers, Andrew Ellul and Dasol Kim, examined 18 different over-the-counter (OTC) derivative markets and noted the following:

“Bank interconnectedness through the OTC derivative markets was identified as an important factor that contributed to the severity of the Great Financial Crisis…and remains an area of fragility of systemically important banks on which we have very limited understanding. The trading of OTC derivatives is notoriously concentrated in the largest banks, which are also the ones for which we have data. One important feature is the substantial counterparty risk that banks face, in our context the most important counterparty risk is that faced by banks trading with non-bank entities.”

Exactly who are these “non-bank entities”? According to the researchers, banks are increasingly using non-financial corporations on the other side of their derivative trades.

Let the above two paragraphs sink in for a moment. After giant, federally-insured banks in the U.S. interconnected themselves via trillions of dollars in derivative bets with wobbly foreign investment banks and a dodgy unit of the giant insurer, AIG, and blew themselves up along with the U.S. economy in 2008, these inter-linkages are still going on 14 years later and regulators have “limited understanding” of just how dangerous this daisy chain of risk really is.

The researchers summarize their findings as follows:

“We show that banks are more likely to either establish or maintain a relationship, and increase their exposures within an existing relationship, with non-bank counterparties that are already heavily connected and exposed to other banks. Banks in such densely-connected networks are more likely to connect with riskier counterparties for their most material exposures. The effects are strongest in the case of (non-bank) financial counterparties. These findings suggest moral hazard behavior in counterparty choices. Finally, we demonstrate that these exposures are strongly linked to systemic risk. Overall, the results suggest a network formation process that amplifies risk propagation through non-bank linkages in opaque financial markets.”

“Risky counterparties,” “heavily connected” banks, “opaque financial markets” –these are the identical factors that blew up century old financial institutions in 2008 and required hundreds of billions of dollars in government bailouts and trillions of dollars in secret loans from the Fed.

The big problem with this OFR research study is that the actual names of the banks and the risky counterparties on the other side of their derivative trades are not mentioned once in the entire report. The only bank names to make an appearance are on Figure 7, a document from the Financial Crisis Inquiry Commission showing the timebomb that Goldman Sachs had become in 2008 with its dubious derivative counterparties.

Fortunately, it doesn’t take research geniuses to quickly figure out who among the megabanks on Wall Street are dangerously interconnected – either to each other or the same risky counterparties. It took us less than a minute to compile the chart below, showing how Wall Street megabanks JPMorgan Chase and Citigroup have been trading like clones of one another, and losing serious ground, over the past five trading sessions.

Then there is the chart we published on January 17, listing the names of the six largest Wall Street borrowers under the Fed’s emergency repo loan facility that was abruptly set up on September 17, 2019 to deal with a financial crisis that the Fed has yet to credibly explain. (Our bet is on a derivatives blowup.) It should be noted that not one mainstream media outlet has released the names of these banks, despite the fact that the Fed itself released the names of the banks and borrowing amounts on December 30, 2021.

The OFR hasn’t always muzzled itself from naming names. In a comprehensive report in February 2015, OFR researchers sounded a very clear alarm bell that just five mega banks in the U.S. posed enormous risks to U.S. financial stability. JPMorgan Chase scored the highest for systemic risk; Citigroup ranked second. Systemic risk scores were based on size, interconnectedness, substitutability, complexity, and cross-jurisdictional activities. The other three banks with high scores were Bank of America, Goldman Sachs and Morgan Stanley.

According to the OFR researchers, Meraj Allahrakha, Paul Glasserman, and H. Peyton Young:

“The larger the bank, the greater the potential spillover if it defaults; the higher its leverage, the more prone it is to default under stress; and the greater its connectivity index, the greater is the share of the default that cascades onto the banking system. The product of these three factors provides an overall measure of the contagion risk that the bank poses for the financial system. Five of the U.S. banks had particularly high contagion index values — Citigroup, JPMorgan, Morgan Stanley, Bank of America, and Goldman Sachs.”

The OFR researchers also pointed directly to Citigroup and JPMorgan Chase for their large base of foreign assets and intrafinancial system liabilities, writing:

“A bank that has large foreign assets and large intrafinancial system liabilities is a potential source of spillover risk. If a large loss in value in foreign assets caused such an institution to fail, the losses could be transmitted to the rest of the U.S. financial system. Five banks had large foreign assets (exceeding $300 billion) and Citigroup and JPMorgan had large figures for both foreign assets and intrafinancial system liabilities…Again, the largest banks are the most interconnected and they are involved in the most cross-jurisdictional activity.”

The Federal Reserve has farmed out its supervision of JPMorgan Chase, Citigroup, Goldman Sachs and Morgan Stanley to the Federal Reserve Bank of New York. Unfortunately, the New York Fed is, literally, owned by these mega banks as its shareholders. The banks elect two-thirds of the Board of Directors of the New York Fed.

All four of these banks played a major role in the 2008 financial crash and all four of these banks (together with Bank of America) control the vast majority of derivatives.

It should be abundantly clear by now that the Federal Reserve is the worst possible regulator of these megabanks and Congress must act with urgency to strip the Fed completely of supervision and oversight of these serial bad actors, as well as its ability to prop them back up with bailouts every time their derivatives blow up.