By Pam Martens and Russ Martens: December 15, 2020 ~

Janet Yellen, Former Chair of the Federal Reserve, Taking the Oath at Her Senate Confirmation Hearing in 2013

President-elect Joe Biden’s nomination of Janet Yellen as Treasury Secretary is being viewed cautiously in some progressive circles. As the post-financial crisis Chair of the Federal Reserve under President Obama, Yellen had the opportunity to interpret the rules of the Dodd-Frank financial reform legislation in a manner that would rein in the risks of the mega banks on Wall Street. She failed in that regard while attempting to reassure a skeptical public that the Fed’s stress tests on the banks were adequate to prevent another crisis.

Yellen famously stated at a London conference in 2017 the following: “Would I say there will never, ever be another financial crisis? You know probably that would be going too far, but I do think we are much safer, and I hope that it will not be in our lifetimes and I don’t believe it will be.”

Two and a half years later, beginning on September 17, 2019, the Fed was back to bailing out Wall Street – months before there was a case of COVID-19 anywhere in the world.

That being said, Yellen is the most qualified and least scandal-ridden nominee for U.S. Treasury Secretary we’ve had in a long time. Yellen chaired the Fed from 2014 to 2018 and was its Vice Chair from 2010 to 2014. She came to the Federal Reserve Board after serving as President of the San Francisco Fed from 2004 to 2010. Yellen also Chaired the White House Council of Economic Advisors from 1997 to 1999 during the Bill Clinton administration. She graduated summa cum laude from Brown University with a degree in economics in 1967 and received her Ph.D. in economics from Yale University in 1971.

The U.S. Treasury’s realm is vast. Its bureaus include the IRS; the Office of the Comptroller of the Currency which regulates national banks; the Bureau of Engraving and Printing and the U.S. Mint that issues the currency and coin of the U.S.; the Financial Crimes Enforcement Network (FinCEN) which is tasked with combating money laundering; and numerous other units. The Treasury Secretary not only sits atop the Treasury but as a result of the Dodd-Frank financial reform legislation, the Treasury Secretary also chairs the Financial Stability Oversight Council (F-SOC) which is responsible for preventing another systemic financial crisis.

But despite its vast reach, U.S. Presidents have nominated and the U.S. Senate has confirmed some highly questionable candidates as U.S. Treasury Secretary.

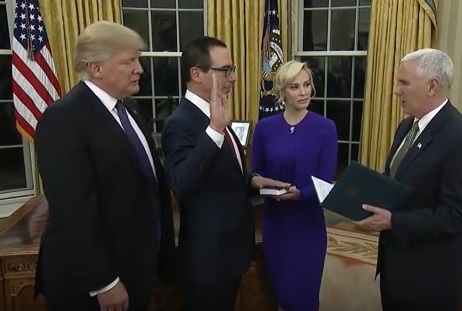

Vice President Mike Pence Swears In Steven Mnuchin as U.S. Treasury Secretary on February 13, 2017. President Donald Trump and Mnuchin’s Fiancée, Louise Linton, Look On. (Linton Is Now Married to Mnuchin.)

Take the case of the current sitting Treasury Secretary Steve Mnuchin. During his January 19, 2017 confirmation hearing, it emerged that Mnuchin had hid offshore accounts from his financial disclosures. Senator Ron Wyden stated: “Mr. Mnuchin, a month ago you signed documents and an affidavit that omitted the Cayman Island fund, almost $100 million of real estate, six shell companies and a hedge fund in Anguilla. This was not self-corrected. The only reason it came to light was my staff found it and told you it had to be corrected.”

As to Mnuchin’s fitness for the job, Senator Wyden presented Mnuchin’s work history as follows during the confirmation hearing:

“Mr. Mnuchin’s career began in trading the financial products that brought on the housing crash and the Great Recession. After nearly two decades at Goldman Sachs, he left in 2002 and joined a hedge fund. In 2004, he spun off a hedge fund of his own, Dune Capital. It was only a few lackluster years before Dune began to wind down its investments in 2008.

“In early 2009, Mr. Mnuchin led a group of investors that purchased a bank called IndyMac, renaming it OneWest. OneWest was truly unique. While Mr. Mnuchin was CEO, the bank proved it could put more vulnerable people on the street faster than just about anybody else around.

“While he was CEO, a OneWest vice president admitted in a court proceeding to ‘robo-signing’ upward of 750 foreclosure documents a week. She spent less than 30 seconds on each, and in fact, she had shortened her signature to speed the process along. Investigations found that the bank frequently mishandled documents and skipped over reviewing them. All it took to plunge families into the nightmare of potentially losing their homes was 30 seconds of sloppy paperwork and a few haphazard signatures.

“These kinds of tactics were in use between 2009 and 2014, a period during which the bank foreclosed on more than 35,000 homes. ‘Widow foreclosures’ on reverse mortgages – OneWest did more of those than anybody else. The bank defends its record on loan modifications, but it was found guilty of an illegal practice known as ‘dual tracking.’ One bank department tells homeowners to stop making payments so they can pursue modification, while another department presses on and hurtles them into foreclosure anyway.”

It also emerged during Mnuchin’s confirmation hearing that while he was in charge, OneWest had foreclosed illegally on active-duty U.S. military service members.

Despite all of this, Republicans in the Senate voted this man into office. Now for a look at how Democrats have behaved.

Timothy Geithner Is Sworn in as 75th U.S. Treasury Secretary in 2009 as His Wife, Carole, Looks On

President Obama’s first Treasury Secretary was Timothy Geithner, who had been the President of the egregiously conflicted New York Fed that is literally owned by some of the biggest banks on Wall Street. In his role as New York Fed President, Geithner spent a great deal of time wining and dining with executives of miscreant banks like Citigroup instead of reining in the wildly speculative conduct that blew them up. Geithner then oversaw the creation of a sprawling octopus of bailout programs for the cratering Wall Street banks during the financial crisis of 2008. Those programs were secretly sluicing trillions of dollars in cumulative loans to failing Wall Street firms, at below-market interest rates, without the awareness of any elected official in Congress. The Wall Street bailouts were occurring in darkness under Geithner as millions of Americans were left on their own to deal with job losses and foreclosures.

It took court actions by the media and a government audit to force the Fed to release the details of its unfathomable $29 trillion in cumulative loans over two and a half years to bail out and resuscitate the Wall Street casino.

Where did Geithner go after leaving the Treasury Department? He became President of – wait for it – the Wall Street firm, Warburg Pincus.

Three major books have cast a negative view of Geithner’s tenure as Treasury Secretary. In Ron Suskind’s Confidence Men, Geithner is said to have ignored a direct order from President Obama to wind down Citigroup. In Neil Barofsky’s Bailout: An Inside Account of How Washington Abandoned Main Street While Rescuing Wall Street, Geithner is portrayed as a callous bureaucrat who viewed the Home Affordable Modification Program (HAMP) as a way to “foam the runways” for the Wall Street banks, slowing down the speed of foreclosures so the banks could deal with them, with no sincere intention of helping struggling families stay in their homes.

The harshest assessment of Geithner came from the former FDIC Chair during the financial crisis, Sheila Bair. In her book, Bull by the Horns, Bair expressed the belief that Citigroup’s two main regulators, John Dugan (a former bank lobbyist) at the Office of the Comptroller of the Currency and Geithner, as President of the New York Fed, were hiding the dire financial condition of Citigroup. Bair writes as follows:

“If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

There are some serious questions as to whether the same thing is happening today at Citigroup.

Bair also exposes Geithner’s proposal for the Federal Deposit Insurance Corporation (FDIC) to provide all out support to Citigroup, guaranteeing all of its debt, including its half trillion in foreign deposits. Bair struck down the idea of guaranteeing foreign deposits but did agree to guarantee Citigroup’s issuance of new debt, providing it was used for lending to help stimulate the economy. What the FDIC examiners found instead was that “Citi was using the program to pay dividends to preferred shareholders, to support its securities dealer operations, and, through accounting tricks, to make it look as if funds raised through TLGP [Temporary Liquidity Guarantee Program] debt were actually raising capital for Citi’s insured bank.”

The second Treasury Secretary under Obama was Jack Lew. Robert Scheer wrote this about Lew at The Nation at the time:

“I suppose that he can’t be much worse than Timothy Geithner, but that should be scant cause for cheer over the news that the president has nominated Jack Lew as Treasury secretary. Both championed the financial deregulation craze of the Clinton administration, and both are acolytes of Robert Rubin, the former Clinton Treasury secretary who unfettered Wall Street greed and then took his own considerable cut of the action.”

Rubin had moved directly to Citigroup shortly after stepping down as Treasury Secretary and helping to move forward the repeal of the Glass-Steagall Act which allowed Citigroup to become a zombie bank/Wall Street trading casino. Rubin received compensation of over $120 million at Citigroup over the next decade to serve on its Board of Directors. Rubin was still sitting there in 2008 when the bank collapsed into the arms of the taxpayer.

Jack Lew Testifying at His Confirmation Hearing, February 13, 2013

Senator Bernie Sanders had this to say from the Senate floor about confirming Jack Lew as Treasury Secretary:

“As someone who supports President Obama, I remain extremely concerned that virtually all of his key economic advisers have come from Wall Street. And let me be clear. It’s not just because Mr. Lew served as a Chief Operating Officer at Citigroup during the financial crisis. It’s not just because Citigroup awarded Mr. Lew a $940,000 bonus as he was leaving to join the State Department in 2009. It’s not just because Citigroup received a total of $2.5 trillion in virtually zero interest loans from the Federal Reserve or that the Treasury Department provided Citigroup with a bailout of more than $45 billion, during Mr. Lew’s tenure at Citigroup. I am opposed to Mr. Lew’s nomination because of the views he now holds about Wall Street and the financial system.

“On September 22, 2010, when I asked Mr. Lew at a Budget Committee hearing if he believed that the deregulation of Wall Street significantly caused the financial crisis, here is what he said: ‘I don’t believe that deregulation was the proximate cause. I would defer to others who are more expert about the industry to parse it better than that.’ At his confirmation hearing earlier this month, Mr. Lew called the Glass-Steagall Act ‘anachronistic’ and said that the Dodd-Frank Act had ‘effectively’ dealt with the issue of banks that are too big to fail. I strongly disagree.

“Mr. President, in my view, we don’t need another Treasury secretary who thinks that the deregulation of Wall Street did not significantly contribute to the financial crisis. We need someone who will stand up to these large financial institutions and say enough is enough! Do I think that Mr. Lew is that person? No, I do not.”