Data Source: St. Louis Fed

By Pam Martens and Russ Martens: November 21, 2019 ~

Yesterday the Federal Reserve released the minutes of its Federal Open Market Committee meeting of October 29-30. The minutes show that the FOMC members were fingering their worry beads over plans for their longer-term handling of the hundreds of billions of dollars weekly that the New York Fed is pumping into the overnight and term repo markets. The worries center on whether the Fed is creating moral hazard and/or that the banks will “take on an undesirably high amount of liquidity risk.”

We have news for the Fed: both of those horses have left the barn. The Fed enshrined moral hazard and liquidity risk among Wall Street banks when it funneled $29 trillion to the miscreant banks from 2007 to 2010 while intentionally hiding its footprints from the public until it lost its court battle and had to disclose the data.

According to the Bank of England’s Financial Stability Report that was released in July, the leveraged loan market is now $3.2 trillion. U.S. mega banks and other global banks hold 38 percent of those high-risk loans or $1.21 trillion. The report also points out that “In the U.S., gross corporate debt as a share of GDP is now above pre-crisis levels.”

The Fed’s FOMC minutes also revealed that it is worried about “the likelihood that participation in the Federal Reserve’s repo operations could become stigmatized….” Well, obviously, if you can’t get one of your peer banks to give you a collateralized overnight loan and have to turn to the Fed, you’ve got a stigma problem.

One thing the Fed did not mention was that its urgent need to funnel $3 trillion into the overnight lending market on Wall Street within a period of two months might spook the commercial paper market where corporations and banks borrow for longer periods, like one to three months.

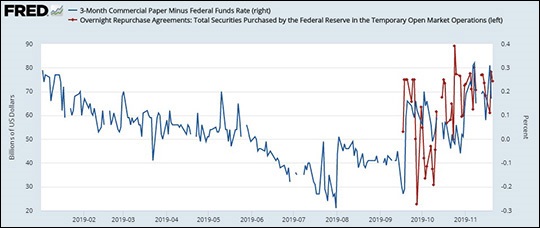

Our chart above, using data provided by the St. Louis Fed, shows that before the New York Fed intervened in the repo market on September 17, the interest rate on 3-month commercial paper was smaller than the targeted rate on the Federal Funds rate set by the Fed. But as the Fed spooked the market by turning on its repo money spigot for the first time since the financial crisis, 3-month commercial paper rates have spiked higher than the Fed Funds rate. In other words, corporations and banks are now paying more to borrow in the commercial paper market. (Please note that the red line in the chart above does not include the 14-day term loans the New York Fed is making. If those were added in, the daily amount of money provided by the New York Fed would have sometimes spiked to over $100 billion.)

The St. Louis Fed data also shows that the commercial paper market is shrinking at the same time the cost to borrow is rising – suggesting that money market funds may be unwilling to roll over maturing commercial paper – exactly what happened during the financial crisis.

The St. Louis Fed data shows that the commercial paper market stood at $1.163 trillion on July 3 of this year. By October 16, that number stood at $1.079 trillion, a decline of $84 billion. Since that time, the amount of commercial paper outstanding has been growing again, to $1.131 trillion by November 13, but that it still a decline from July 3 of $32 billion.

The following is an excerpt from the FOMC minutes on how the Fed is thinking about its future actions in the repo market:

“The staff presented two potential approaches for conducting repo operations if the Committee decided to maintain an ongoing role for such operations. Under the first approach, the Desk would conduct modestly sized, relatively frequent repo operations designed to provide a high degree of readiness should the need for larger operations arise; under the second approach, the FOMC would establish a standing fixed-rate facility that could serve as an automatic money market stabilizer. Assessing these two approaches involved several considerations, including the degree of assurance of control over the federal funds rate, the likelihood that participation in the Federal Reserve’s repo operations could become stigmatized, the possibility that the operations could encourage the Federal Reserve’s counterparties to take on excessive liquidity risks in their portfolios, and the potential disintermediation of financial transactions currently undertaken by private counterparties. Regular, modestly sized repo operations likely would pose relatively little risk of stigma or moral hazard, but they may provide less assurance of control over the federal funds rate because it might be difficult for the Federal Reserve to anticipate money market pressures and scale up its repo operations accordingly. A standing fixed-rate repo facility would likely provide substantial assurance of control over the federal funds rate, but use of the facility could become stigmatized, particularly if the rate was set at a relatively high level. Conversely, a standing facility with a rate set at a relatively low level could result in larger and more frequent repo operations than would be appropriate. And by effectively standing ready to provide a form of liquidity on an as-needed basis, such a facility could increase the risk that some institutions may take on an undesirably high amount of liquidity risk.”