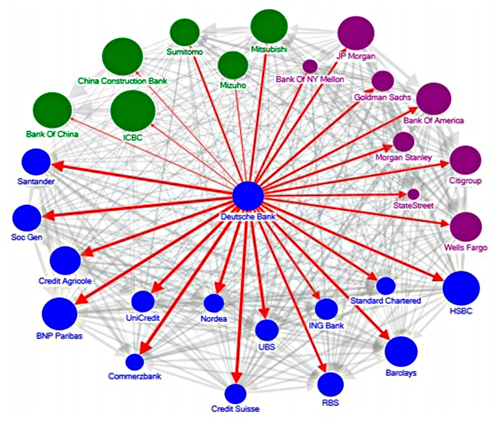

Systemic Risk Among Deutsche Bank and Global Systemically Important Banks (Source: IMF — “The blue, purple and green nodes denote European, US and Asian banks, respectively. The thickness of the arrows capture total linkages (both inward and outward), and the arrow captures the direction of net spillover. The size of the nodes reflects asset size.”)

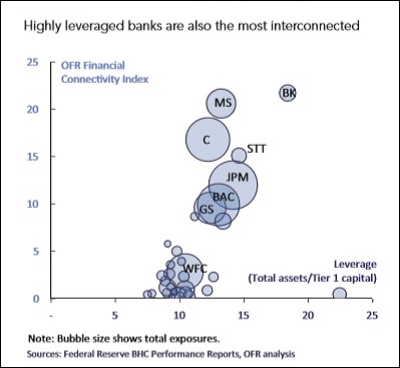

Wall Street Mega Banks Are Highly Interconnected: Stock Symbols Are as Follows: C=Citigroup; MS=Morgan Stanley; JPM=JPMorgan Chase; GS=Goldman Sachs; BAC=Bank of America; WFC=Wells Fargo.

By Pam Martens and Russ Martens: September 27, 2016

After repeated, but ignored, warnings over the past two years from researchers at the U.S. Treasury’s Office of Financial Research (OFR), the new banking crisis has arrived with a vengeance and at a most inopportune time – when confidence is already draining from the financial system because of two U.S. presidential candidates with the highest disapproval ratings in modern history.

Yesterday, Germany’s largest financial institution, Deutsche Bank, lost 7.06 percent by the close of trading on the New York Stock Exchange. That plunge in one of the most globally-interconnected banks dragged down the shares of every major Wall Street bank yesterday: Bank of America lost 2.77 percent; Morgan Stanley declined by 2.76 percent; Citigroup lost 2.67 percent; Goldman Sachs shed 2.21 percent; and JPMorgan Chase closed down 2.19 percent. Deutsche Bank, whose shares traded at more than $120 pre-crisis in 2007, closed at $11.85 yesterday in New York and was down another 3 percent in overnight trading in Europe.

At yesterday’s close, Deutsche Bank had $16.344 billion in market value with a balance sheet of $1.9 trillion in assets as of the end of 2015. If that doesn’t sound like a replay of the Citigroup debacle that spiraled out of control in 2008 and took down other bank shares, we don’t know what does. But the big picture is actually worse than even this suggests.

The first graph above comes from a report released in June of this year by the International Monetary Fund (IMF). The report singled out Deutsche Bank as “the most important net contributor to systemic risks.” The researchers wrote:

“Notwithstanding moderate cross-border exposures on aggregate, the banking sector is a potential source of outward spillovers. Network analysis suggests a higher degree of outward spillovers from the German banking sector than inward spillovers. In particular, Germany, France, the U.K. and the U.S. have the highest degree of outward spillovers as measured by the average percentage of capital loss of other banking systems due to banking sector shock in the source country…

“Among the G-SIBs [Global Systemically Important Banks], Deutsche Bank appears to be the most important net contributor to systemic risks, followed by HSBC and Credit Suisse…The relative importance of Deutsche Bank underscores the importance of risk management, intense supervision of G-SIBs and the close monitoring of their cross-border exposures, as well as rapidly completing capacity to implement the new resolution regime.”

Has there been “close monitoring” of the Global Systemically Important Banks by U.S. Federal regulators like the Federal Reserve and Office of the Comptroller of the Currency? Based on the reports released by the U.S. Treasury’s Office of Financial Research, the Federal regulators are just as asleep at the switch this time around as they were in the lead up to the Wall Street banking crash of 2008.

The regulators took no action when Citigroup effectively repealed an important derivatives reform measure by slipping an amendment into a Congressional spending bill in December 2014 that allowed banks holding FDIC-insured deposits to keep trillions of derivatives on the books of the bank, instead of pushing them out to other, uninsured, units of the bank holding company. That put the U.S. taxpayer right back on the hook for another massive bailout if the bank should fail.

Federal regulators have also sat on their hands as Citigroup has loaded up on credit default swaps, the very instruments that blew up the big insurer AIG in 2008, forcing a taxpayer bailout of $185 billion. As we wrote on August 4:

“According to the data, Citigroup now has $2.08 trillion in Credit Derivatives (the vast majority of which are Credit Default Swaps). Only JPMorgan is bigger with $3.1 trillion in credit derivatives. Equally frightening, the vast majority of these are private contracts between financial institutions (Over-the-Counter) where regulators lack the granular details of the deals. President Obama falsely promised the American people that derivatives would be moved onto exchanges with proper capital and transparency following the Dodd-Frank financial reform legislation in 2010. That has not happened. The vast majority of all derivatives are still traded in the dark.

“Not only are Citigroup’s Federal regulators allowing it to engage in this high risk trading but they are actually allowing Citigroup to purchase the high risk positions of a deeply troubled bank – Deutsche Bank. Risk Magazine reports… that Citigroup bought $250 billion of Credit Default Swaps from Deutsche Bank in 2013. Bloomberg News also reported on the $250 billion Citigroup purchase from Deutsche Bank.”

Subsequent to our August 4 article, Bloomberg News reported that Citigroup had “purchased a portfolio of credit-default swaps from retreating rival Credit Suisse Group AG” which had a notional value (face amount) of $380 billion.

That Federal regulators would allow this toxic stew to once again bubble up in the U.S. banking system after the biggest banking collapse since the Great Depression just eight years ago is nothing short of negligence and dereliction of duty.

The Federal Reserve is not only derelict, but according to the Office of Financial Research, it is not even properly conducting its stress tests on the big banks. On March 8, OFR released a study on Credit Default Swaps. The researchers found that the Fed’s stress tests are measuring only the bank holding company’s “direct counterparty concentrations” for credit default swaps rather than the indirect fallout. The authors found that “indirect effects can be as much as nine times larger than the direct impact” on the bank holding company, and ignoring that reality “could understate the stress on banks.”

Watching the fallout in the shares prices of interconnected banks yesterday, and the same pattern in January of this year, effectively proves that the OFR researchers are right and the Federal Reserve is dead wrong. (See related articles below.)

Related Articles:

Wall Street Banks Are Trading as a Herd Because They are Highly Interconnected

Interconnected Banks Pose Greatest Threat to U.S. Financial System

Bailed Out Citigroup Is Going Full Throttle into Derivatives that Blew Up AIG

Are Wall Street Banks in Trouble? You’d Never Know from the Headlines.