By Pam Martens: October 9, 2014

Eric Hunsader of Nanex

There were some interesting moves in the Chicago futures markets yesterday that might have been an effort to instill fear in traders that were short the market ahead of the release of the Fed’s minutes slated for unveiling at 2 p.m. Getting the party started early could induce panic short covering if the Fed minutes suggested a dovish approach to raising interest rates – which indeed they did.

The stock market had been down as much as 55 points around the 11 a.m. hour but began a gradual advance ahead of the release, with a surge to close up 274.8 points higher on the Dow Jones Industrial Average. Looking a bit psychotic, that move of more than 329 points peak to trough followed by just one day a loss of 273 points in the Dow.

Eric Hunsader, chart watcher and computer whiz who heads the market data firm Nanex, posted at Twitter yesterday that there were six separate 1000 contract eMini trades between 12:38 and 1:10 p.m. Then, just 22 seconds before the release of the Fed minutes, another 1000 eMinis are bought when “liquidity is non-existent,” says Hunsader.

The eMini is an electronically traded futures contract based on the Standard and Poor’s 500 index. Its contract values are one-fifth the size of the larger S&P 500 futures contract.

There are some equally fascinating charts posted this morning by Hunsader at Twitter showing unusual moves both in equities and currency markets ahead of the release of the Fed minutes.

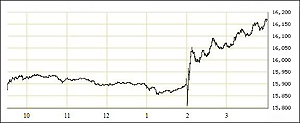

The market action yesterday reminded us of the curiosities in the stock market on December 18 of last year when the market bizarrely cheered the announcement that the Fed was going to start taking away the punch bowl by tapering its monthly bond buying program to the tune of $10 billion a month. Business headlines reported the big rally which brought the Dow to a close of up 292 points. What was left out of the reporting was that the market’s immediate reaction to the news was not a rally but a downward plunge — a much more logical reaction.

Here’s how we reported the action the following day:

Dow Jones Industrial Average, Intraday Moves on December 18, 2013 from BigCharts.com

“The stock market did not initially rally at 2 p.m. on the Fed’s announcement – it did a bungee jump downward, as you can see on the daily chart here from BigCharts.com. That plunge is the patently normal reaction any sane market watcher would have expected after all previous hints from the Fed that it would begin tapering have sent the market into panic losses.

“But by 2:03 p.m., a very strange thing was happening. The market reversed course on a dime and the Dow Jones Industrial Average was up 51 points. By 2:05 p.m., it was up 125 points. By 2:10, up 158 points. By the close of trading at 4:00 p.m., it was up 292.71 points.

“The idea that the stock market took a Xanax after lunch and was in a confident, gleeful mood by mid afternoon is the stuff of tooth fairy yarns. Don’t think for one second that this was a genuine rally, that Wall Street is cheering its punch bowl being taken away, that removing $10 billion a month from speculators is chicken feed, that the onset of Fed tapering isn’t perceived on Wall Street as the horrific beginning of tightening of monetary policy.

“This was no rally. This was panic short-covering.

“Panic short-covering that fuels a rally of this size happens when big money has made bets on the market going down (shorted the market) and the market goes the other way, forcing speculators to quickly buy stocks to cover (close out) their open short trades to avoid steeper losses. That’s why there was such a huge spike in the market from the initial plunge at 2 p.m. versus the market being up 158 points just 10 minutes later.

“The obvious, and most important question, is who pushed the market up in the first place to panic the shorts? Who got the party started? That would have taken some serious money moving into Standard and Poor’s futures contracts or key component stocks in the Dow.”

Now, there is one other concern. Could market participants outside of the Fed gain early unauthorized access to Fed minutes or details of what they will contain? David Kotok of Cumberland Advisors noted the following in a September 18, 2014 column at Business Insider:

“My colleague Bob Eisenbeis was formerly the director of research at the Federal Reserve Bank of Atlanta. He participated in many Fed activities, including FOMC meetings. He has a long and distinguished history with the Fed. He never violated the principle that inside information should not be intentionally leaked to journalists. I asked Bob if he saw any leaks during his tenure at the Fed. His answer was ‘yes.’ Bob recalls that there were two leaks and that Chairman Greenspan sought an investigation of each leak, once by the FBI and another by the Inspector General. The outcome of these investigations was not revealed to the FOMC when Bob was present.”