By Pam Martens and Russ Martens: January 20, 2020 ~

Photo of the Trading Floor at the New York Fed (Obtained by Wall Street On Parade from an Educational Video)

The New York Fed is so protective of its surreptitious trading relationship with Wall Street that it previously denied Wall Street On Parade a photo of its trading floor. (We obtained the one pictured here from a Fed educational video.) It is, by the way, the only one of the 12 regional Federal Reserve banks to have a trading floor.

The New York Fed has been allowed by Congress to insert itself so deeply in markets that it’s highly possible that history will find it at least partly responsible for the next market implosion.

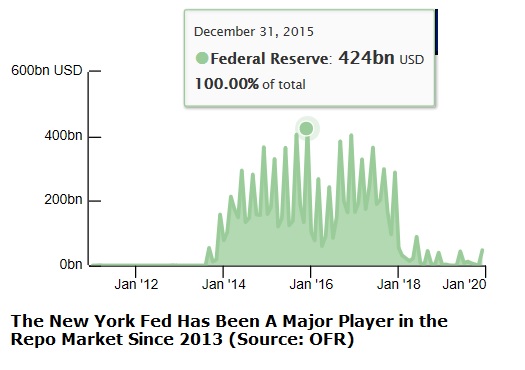

The well-promulgated notion that the Federal Reserve began heavily meddling in the repo loan market on September 17 of last year is a piece of fiction. According to the U.S. government’s own database, residing at the Office of Financial Research (OFR), from 2014 through December 31, 2017, the New York Fed was engaged in repo transactions with U.S. Money Market Funds with $200 to $400 billion changing hands on pivotal days. For example, on December 31, 2015, the Fed engaged in $424 billion in repo transactions; on December 31, 2016, $403 billion changed hands; and as recently as June 30, 2017, $354 billion changed hands between Money Market Funds and the New York Fed.

These repo transactions were called Reverse Repurchase Agreements (Reverse Repos), where the New York Fed sold U.S. Treasury securities it held to Money Market Funds with a stated agreement to repurchase the security at a specified price on a specified date in the future. The difference between the sale price and the repurchase price, adjusted for the number of days outstanding, implies a rate of interest paid by the New York Fed on the transaction.

Because a Money Market Fund could make a very large transaction with the New York Fed without concern about a default by a dozen other Wall Street bank counterparties among whom it might have otherwise attempted to spread its risk, the New York Fed became the Reverse Repo loan counterparty of choice, rapidly dominating the market.

In a November 18, 2016 article by Bradley Keoun at TheStreet.com, Josh Galper, a repo-expert at Finadium, was quoted as follows regarding the Fed: “They’ve become a very large player in a very short period of time, and that creates a market distortion that I view as undesired. It crowds out private-sector players and it distorts pricing.”

The New York Fed not only crowded out other counterparties but they also crowded out other forms of repo collateral according to OFR data. The repo collateral at Money Market Funds went from 33 percent U.S. Treasuries on January 31, 2011 to 63 percent on August 31, 2019 according to OFR data, making obligations of Wall Street and foreign banks less and less desirable.

The New York Fed effectively created a new market of one-stop shopping for all your Treasury needs for time-constrained and harried Money Market Fund managers. TheStreet.com article provided this quote from Debbie Cunningham, Chief Investment Officer for Global Money Markets at the large mutual fund company, Federated Investors: “The Fed’s program is very easy. It takes a lot of work otherwise to call 40 other counterparties.”

Today, the Fed has moved in the opposite direction. Since September 17 of last year, it is buying, not selling, hundreds of billions of dollars each week in Treasury securities and government agency mortgage debt from Wall Street trading houses it calls its “primary dealers,” some of which are the very same dealers it crowded out of the Money Market Fund repo loan market. These are the first repo loans where the Fed is buying up securities and crediting the trading houses with cash since the financial crisis – raising the question in the public mind as to whether a new crisis is brewing.

Now, another market is being grossly distorted. Since the New York Fed turned on its money spigot and began cumulatively adding trillions of dollars each month to the trading desks of Wall Street firms – with no questions asked as to what these firms were doing with the money – the Dow Jones Industrial Average has spiked 3,000 points, closing last week at 29,348.

Americans need to have a serious conversation about how we got to this point in time when dangerous, high-risk Wall Street trading firms own our federally-insured deposit-taking banks and taxpayers are never more than one stupid-move by the New York Fed away from another epic bailout of the U.S. financial system.

Just how overdue is that conversation?

No one ever expected that the New York Fed would become both the sugar daddy and key regulator to Wall Street’s most dangerous banks. But it did.

No one ever expected that the New York Fed would secretly funnel $29 trillion of electronically conjured money to bail out the Wall Street banks and their foreign derivatives counterparties during and after the 2008 financial crash. But it did.

No one ever expected that the New York Fed would be rewarded for allowing Citigroup to become a smoldering ruin of a derivative fireworks factory by getting increased supervisory powers after the epic 2008 crash, but it did.

No one ever expected that JPMorgan Chase, a bank that admitted to three criminal felony counts and lost $6.2 billion of depositors’ money trading exotic derivatives would be rewarded, by the New York Fed, by getting fees to manage $1.7 trillion of the New York Fed’s assets, but it did.

And despite this abysmal history at the New York Fed, Congress has yet to call the New York Fed executives to testify about its latest multi-trillion-dollar meddling in U.S. markets.