Public Debt as a Percent of GDP

By Pam Martens and Russ Martens: July 27, 2018 ~

The much anticipated Gross Domestic Product (GDP) number for the second quarter of 2018 was released at 8:30 a.m. this morning. President Trump had played advance man for the number during a rally yesterday saying some were predicting it could be over 5 percent but he would be happy if it had a 4 in front of the number. The number came in at 4.1 percent with the first quarter GDP being revised up to 2.2 percent.

While the President would like to see this as a lasting trend owing to the brilliance of his economic policies, experts say the U.S. is far more likely to revert back to the trend of growth in the 2 percent range. The Federal Reserve is projecting a GDP rate of 2.8 percent for all of 2018; 2.4 percent in 2019; and back to the sluggish 2 percent GDP in 2020 – the type of tepid annual growth that has plagued the country since the epic Wall Street crash of 2008 delivered the worst period of wealth destruction since the Great Depression.

The Obama administration also saw some quarters where GDP ratcheted above trend – but the annual rate of GDP growth remained subdued. In the best economic year of the Obama presidency, 2015, GDP came in at 2.9 percent.

Trump achieved this one-quarter number on the back of a trillion dollar tax cut passed last year and a $300 billion stimulus boost passed in February of this year to spread over this year and next. The outsized GDP number was also likely buoyed by corporations rushing to stock up on materials needed to run their businesses before the new tariffs kick in.

What there is no dispute about is that the Trump administration’s fiscal policies are going to lead to their own headwind to growth – mushrooming national debt and higher interest payments on that debt.

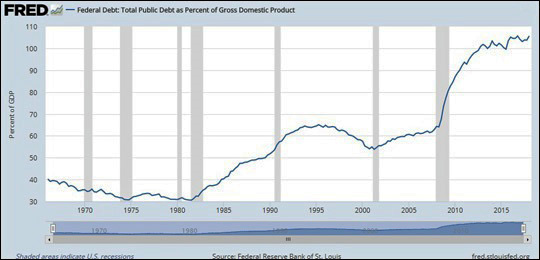

At the end of the third quarter of 2001, in the administration of George W. Bush (a Republican), the U.S. national debt stood at $5.8 trillion. On the same date in 2008, four months before Barack Obama (a Democrat) assumed the presidency, the national debt stood at $10 trillion. Four months before Obama left office, the national debt stood at $19.57 trillion, just shy of a doubling of the national debt in just eight years – a stunning rate of growth.

Currently, the gross Federal debt is $21.27 trillion. According to a report released last year by the Congressional Budget Office (CBO), the annual Federal budget deficit is projected to cross the $1 trillion mark by 2020, in part because of the tax cuts. That means the U.S. Treasury will be bringing ever increasing amounts of Treasury debt to market and that increased supply is likely to put upward pressure on interest rates.

The increase in supply of Treasury debt is coming at a time of lessening demand. The Federal Reserve is in the process of scaling back its purchases of U.S. Treasuries in order to “normalize” its balance sheet from its Quantitative Easing (QE) days during the Great Recession. The Fed’s first cutback in its purchases came in October of 2017 with the Fed shrinking the amount of maturing Treasury principal it was rolling over into new Treasuries by $6 billion a month. The shrinkage amount will grow gradually until October of this year when the Fed will roll over $30 billion less each month in Treasuries going forward than it had in prior years. (The Fed also acquired large holdings in mortgage-backed securities during the financial crisis and it is trimming its rollover of maturing principal in those as well.)

Another headwind is the fact that the Fed was easing during most of the Obama administration and it has been in rate-hike mode since December of 2015. The Government Accountability Office (GAO) indicates that 58 percent of U.S. Treasury securities held by the public will be maturing between now and 2022. That debt will most likely be rolled over into a higher interest rate environment, meaning that the government’s outlay for interest payments on its debt will be rising significantly: another headwind to growth.

All of this raises the question as to why the Trump administration would engage in tax cuts and deficit spending when the economy was expanding and enjoying a very low rate of unemployment. Because those moves hamper long-term growth by increasing the national debt burden, they are only prudent to spur the economy during times of recession, not expansion.

The outcome of all of this is that President Trump will be able to brag about his great economy for one quarter and our children’s generation will be left to deal with crippling debt and a lower standard of living.

Trump Tweet, July 27, 2018