By Pam Martens and Russ Martens: June 18, 2018 ~

Lloyd Blankfein, CEO of Goldman Sachs

Goldman Sachs CEO Lloyd Blankfein famously said in 2009 at the height of the financial crisis that he was “doing God’s work.” What Goldman Sachs was actually doing in secret at that time was receiving billions of dollars in undisclosed loans from the Federal Reserve – often at the insanely low interest rate of .01 percent. Goldman was also living off billions of dollars in publicly acknowledged taxpayer bailouts, while paying out obscene bonuses to its executives, including those who had shorted (made bets against) the U.S. housing market as it collapsed into the greatest disaster since the Great Depression. (See related articles below.)

Last week we received an unsolicited direct mail offer from Goldman Sachs. It was offering us the ability to borrow a personal loan ranging from $3500 to $40,000 with rates ranging from 6.99 to 24.99 percent. The solicitation noted that “only the most creditworthy applicants qualify for the lowest rates; and longer term loans have higher rates.”

The Goldman deal was coming from “Marcus,” which a footnote informed us “is a product of Goldman Sachs Bank USA,” a bank being backstopped with Federal deposit insurance, which is, in turn, backstopped ultimately by the U.S. taxpayer.

To summarize, a bank that received a cumulative total of $814 billion in bailout funds during a financial crash it helped to create, with much of that amount consisting of secret loans from the Fed at an interest rate close to zero, wants to charge interest rates as high as 25 percent to Americans, many of whom are still struggling to recover from the greatest economic downturn since the 1930s.

We decided to find out what ever happened to state usury laws that capped the amount of interest that banks and other types of lenders could charge to consumers. What we found wasn’t pretty. America has traveled from an age of enlightenment on usury to the Dark Ages.

In the early 18th Century, the American colonies set an interest rate cap on loans at 8 percent. In the late 18th Century, most states adopted a 6 percent cap on interest rates on loans. The early 1900s saw a rise in the power of Wall Street banks in Washington: 11 states eliminated their usury laws completely while others raised the cap to 10 to 12 percent interest. Between the 1940s and late ‘70s, the caps exploded across the United States, with many states allowing interest rates as high as 36 percent. Things have gotten dramatically worse since that time.

The Wall Street banking cartel – where a handful of banking behemoths now control the majority of savings deposits, and mortgages, and credit cards in the United States – also effectively control through lobbyists the usury legislation at the Federal and State levels. It should come as no surprise to anyone that concurrent with the unconscionable rise in the amount of interest that lenders can charge on loans has also come an unprecedented rise in wealth and income inequality in the United States.

Last year Fortune ran this headline: The Wealth Gap in the U.S. Is Worse Than In Russia or Iran and then backed it up with academic data. Also last year the World Economic Forum found that the United States ranks 23 out of 30 among developed countries in an index that factors in data on income, health, poverty and sustainability.

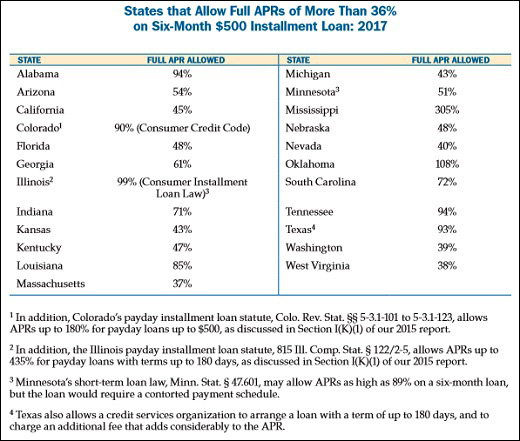

Last August, the National Consumer Law Center updated its 2015 report that analyzed usury statutes in all 50 states and the District of Columbia. Some of the findings will (like the current Trump policy to rip immigrant children from their parents) suggest to you that those in positions of power across the United States have lost their soul.

The report notes that since its 2015 study was published, “Mississippi legislators enacted the misleadingly named ‘Mississippi Credit Availability Act’ that allows an APR [Annual Percentage Rate] of 305% for a $500 loan repayable over six months. The state joins Tennessee, which amended its lending laws in 2014 to allow non-bank lenders to make cash advances at 279%, to make up the ‘Terrible Two’—the two states that have done the most to open their doors even wider for predatory lending practices in recent years.”

The “Terrible Two” should actually be called the “Unconscionable Monsters,” and a new category instituted that is called the “Banking Whore States.” Using the National Consumer Law Center’s graph below for what various states allow to be charged on a $500 six-month loan with all fees and interest included, we’d put the following states in this category: Oklahoma, 108 percent; Illinois, 99 percent; Alabama and Tennessee 94 percent; Texas 93 percent; and numerous others that range from 60 to 90 percent.

The political revolution that presidential candidate Senator Bernie Sanders called for in 2016 needs to happen very soon or America may be unable to ever find its way back.

Source: National Consumer Law Center

Related Articles:

Goldman Sachs’ Rich Man’s Bank Backstopped by You and Me

Here’s How Goldman Sachs Became the Overlord of the Trump Administration

Goldman Sachs Top Lawyer Is Part of a Secret Banking Cabal as CEO Blankfein Denies One Exists