Five Wall Street Mega Banks Are Highly Interconnected: Stock Symbols Are as Follows: C=Citigroup; MS=Morgan Stanley; JPM=JPMorgan Chase; GS=Goldman Sachs; BAC=Bank of America

By Pam Martens and Russ Martens: July 6, 2017

According to the Federal Deposit Insurance Corporation (FDIC), as of March 31, 2017 there were a total of 5,856 banks in the U.S. operating under its Federal deposit insurance umbrella. But according to government financial researchers, five of those banks pose an ongoing material threat to the U.S. financial system. Not surprisingly, those five banks hold insured deposits for savers while simultaneously engaging in highly leveraged, high risk trading on Wall Street.

On June 27, Janet Yellen, the Chair of the U.S. Federal Reserve (the nation’s central bank) spoke at an event at the British Academy in London. She stated the following about the U.S. financial system:

“Would I say there will never, ever be another financial crisis? You know probably that would be going too far, but I do think we are much safer, and I hope that it will not be in our lifetimes and I don’t believe it will be.”

We hate to be the bearer of bad tidings, but there is no substantive data to support Janet Yellen’s view. In fact, the very body that provides the intelligence to the Financial Stability Oversight Council (F-SOC), the U.S. Treasury’s Office of Financial Research (OFR), has been pumping out volumes of research that strongly suggest just the opposite. According to OFR’s research, those five Wall Street mega banks hold the fate of the U.S. financial system in their highly interconnected and highly dangerous hands. Tragically, that’s pretty much the same condition the U.S. was in heading into the crash of 2008.

According to OFR research:

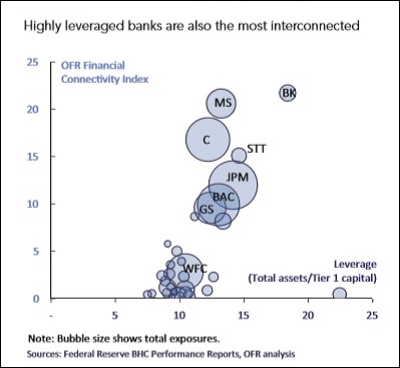

“The larger the bank, the greater the potential spillover if it defaults; the higher its leverage, the more prone it is to default under stress; and the greater its connectivity index, the greater is the share of the default that cascades onto the banking system. The product of these three factors provides an overall measure of the contagion risk that the bank poses for the financial system. Five of the U.S. banks had particularly high contagion index values — Citigroup, JPMorgan, Morgan Stanley, Bank of America, and Goldman Sachs.”

According to data from the Office of the Comptroller of the Currency (OCC), those same bank holding companies as of March 31, 2017 were sitting on astronomical levels of derivatives: in notional (face amount) of derivatives, Citigroup held $54.8 trillion; JPMorgan Chase held $48.6 trillion; Goldman Sachs Group had $45.6 trillion; Bank of America held $35.8 trillion while Morgan Stanley sat on $30.8 trillion. Graphs in the OCC report show that the top 25 bank holding companies held a total of $242.3 trillion in notional derivatives at the end of the first quarter of 2017, of which these five bank holding companies accounted for 89 percent of that amount.

OFR research has also found systemic risks exist from these five banks’ holdings of large foreign assets and/or intrafinancial system liabilities, writing:

“A bank that has large foreign assets and large intrafinancial system liabilities is a potential source of spillover risk. If a large loss in value in foreign assets caused such an institution to fail, the losses could be transmitted to the rest of the U.S. financial system. Five banks had large foreign assets (exceeding $300 billion) and Citigroup and JPMorgan had large figures for both foreign assets and intrafinancial system liabilities…Again, the largest banks are the most interconnected and they are involved in the most cross-jurisdictional activity.”

What is stunning about the interconnectedness of today’s big Wall Street banks is that it so closely parallels the research findings on the crash of 2008. In a 2011 paper prepared for the Money and Banking Conference in Buenos Aires, financial researcher Jane D’Arista wrote:

“Interconnectedness is one of the critical clusters of related causes of the crisis. It resulted from the extraordinary growth in indebtedness within the financial sector that facilitated higher leverage ratios and rising levels of speculative trading for institutions’ own accounts. As the amount of short-term borrowing and lending among financial institutions expanded, markets for repurchase agreements and commercial paper became primary funding sources, forging a chain that linked the fortunes of many institutions and various financial sectors to the performance of a few of the largest and exacerbated systemic vulnerability. Increased profits and compensation masked the growing vulnerabilities in the system but the crisis outcome was inevitable given:

— the buildup of unsustainable debt for individual institutions and the system as a whole;

— systemic undercapitalization as inflated on- and off-balance sheet positions increased risk from falling prices and the potential loss of funding, and;

— the heightened potential for loss of confidence as opaque markets for funding and OTC derivatives increased uncertainty about prices, volumes of transactions and the positions of counterparties.”

The reason that there has been so little meaningful reform since the 2008 epic collapse on Wall Street and the greatest taxpayer bailout in U.S. history, is that the U.S. political system is as broken as Wall Street’s structure.

According to the Center for Responsive Politics, since 1998, Citigroup has spent more than $98 million lobbying Congress while JPMorgan Chase has spent approximately $85 million. Those figures are dwarfed, however, by the hundreds of millions of dollars that Wall Street’s trade groups spend lobbying Congress. It is also dwarfed by the corruption that flows from the disintegration of campaign finance laws which now allow the millionaires and billionaires on Wall Street to make obscene political donations to both of the major political parties as well as individual candidates. The will of the majority of Americans to shrink these Wall Street behemoths down to a non-dangerous size and restore credibility to the U.S. banking system has been completely drowned out by casino capitalism’s money spigot in Washington.