Source: Federal Deposit Insurance Corporation

By Pam Martens and Russ Martens: December 27, 2016

In 1934 the U.S. had 14,146 commercial banks holding insured deposits. By 1985, that number had barely budged, standing at 14,417. Then came the Bill Clinton administration in the 1990s and its reckless and unprecedented banking deregulation which allowed the giant Wall Street banks to swallow up, or drive out of business, thousands of banks across America. According to the Federal Deposit Insurance Corporation (FDIC), as of December 22 of this year, there are only 5,927 FDIC insured banks left in the U.S., a stunning decline of 59 percent from 1985.

But those numbers are just the tip of the iceberg. Banking concentration in the U.S. has reached an unprecedented crisis level when it comes to deposits. Out of the dramatically shrunken base of 5,927 FDIC insured banks which were holding a total of $11.2 trillion in total deposits (insured and uninsured deposits) as of September 30, 2016, just four banks hold 44.6 percent of all deposits. Those four banks are JPMorgan Chase Bank N.A. with $1.486 trillion in total deposits; Bank of America N.A. with $1.3 trillion in total deposits; Wells Fargo Bank N.A. with $1.3 trillion in total deposits; and Citibank N.A. with total deposits of $947.8 billion. (Deposit figures are as of September 30, 2016. The source is the FDIC.)

Each of those four banks also have an outsized presence on Wall Street; each of them received taxpayer bailouts during the 2008 crash; each received secret, below-market interest rate loans from the Federal Reserve during the crisis; and three of them (JPMorgan Chase, Bank of America and Citibank) are currently holding tens of trillions of dollars in derivatives within the insured banking subsidiary – meaning there would be a forced taxpayer bailout if the derivatives blew up the bank.

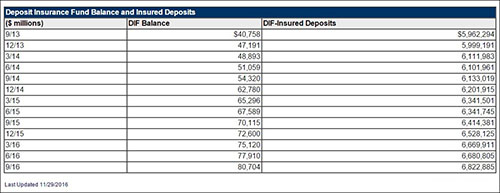

Here’s why these behemoth banks pose such a threat to the safety and soundness of the U.S. banking system. The FDIC’s Deposit Insurance Fund (DIF) as of September 30, 2016 stood at $80.7 billion (that’s billion with a “b”) to insure a total of $6.8 trillion of DIF-insured deposits. That’s a slim reserve ratio of 1.18 percent in a banking system that required $16 trillion of secret Federal Reserve loans to resuscitate itself from 2007 to 2010. Citigroup, parent of Citibank, alone received $2.5 trillion in cumulative revolving loans of the $16 trillion loaned by the Fed. It has more derivatives today than it did at the peak of the crisis in 2008.

How did Bill Clinton’s administration set this train wreck in motion? In 1999, Clinton signed the repeal of the Glass-Steagall Act which had kept the nation’s banking system safe for 66 years. This allowed Wall Street’s speculative trading activities in its investment banks and brokerage firms to merge with commercial banks holding insured deposits that are backstopped by the U.S. taxpayer. But Clinton did two other horrendous banking deeds: in 1994 Clinton signed into law the Riegle-Neal Interstate Banking and Branching Efficiency Act. This permitted bank holding companies to acquire banks anywhere in the nation and invalidated the laws of 36 states which had allowed interstate banking only on a reciprocal or regional basis. And, finally, Clinton signed into law the Commodity Futures Modernization Act of 2000, allowing trillions of dollars of OTC derivatives on Wall Street to escape regulation.

It is nothing short of fiduciary negligence that Congress has allowed this dangerous banking system to remain unreformed eight long years after the greatest financial collapse since the Great Depression.