By Pam Martens and Russ Martens: July 15, 2016

President Obama Calls Surprise Meeting With Financial Stability Oversight Council Members, March 7, 2016

The problem with stereotyping Republicans is that when they are screaming from the rooftops about a legitimate fraud, Democrats don’t believe them — even when the evidence is overpowering that they are right.

For years now, Republicans have been screaming that the Dodd-Frank Wall Street Reform and Consumer Protection Act that was signed into law in 2010 by President Obama is a fraud on the public.

Few have examined Dodd-Frank’s failed promises as carefully as Wall Street On Parade. The legislation promised to rein in derivatives – it didn’t. It promised to end the future need for taxpayer bailouts of too-big-to-fail banks. It didn’t. It promised to institute the Volcker Rule to prevent banks from gambling with insured deposits. It didn’t. It promised to reform the practices of the ratings agencies that played a pivotal role in the 2008 collapse. It didn’t.

Dodd-Frank did two great things: it created the Consumer Financial Protection Bureau (CFPB) which has played a major role in exposing and disciplining companies that abuse consumers in areas like credit cards, auto loans, student loans, and mortgages. Dodd-Frank also created the Office of Financial Research in the U.S. Treasury Department – which has been sending out regular warnings that Wall Street is still a dangerous, toxic brew of interconnectedness while putting a bright light on how the Fed is mismanaging its stress tests of the mega Wall Street banks.

But these two agencies which are valiantly working in the public interest are no match for how Wall Street has been allowed by the Obama administration to game the designed-to-be-gamed provisions of Dodd-Frank.

Take this morning’s news from Bloomberg News. The so-called Volcker Rule provisions of Dodd-Frank that barred the Wall Street banks holding insured deposits from owning private-equity funds (where they could inflate asset values with little push-back) and hedge funds (where they could dump or hide their own losses) have been repeatedly pushed forward and now are not set to go into effect until July of next year – an outrageous seven years after Dodd-Frank was signed into law.

Wall Street is clearly counting on their heavy funding of Hillary Clinton’s campaign to put a friendly ear in the Oval Office, and at the Fed, Treasury and SEC, so it can individually apply for permanent exceptions to these and various other Dodd-Frank rules.

Under Dodd-Frank, the Wall Street banks were required to move their derivatives to exchanges or central clearinghouses. As recently as March 7 of this year, President Obama held a press conference following his meeting with the Financial Stability Oversight Council and stated the following about derivatives: “you have clearinghouses that account for the vast majority of trades taking place.”

When the President made this statement he was surrounded by every major Wall Street bank regulator who knew that statement was patently false. Not only is it false but the reality of what has actually happened suggests a willingness to egregiously mislead the American people.

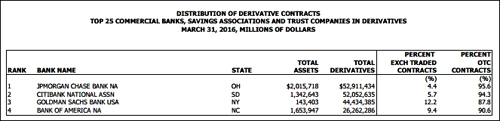

Below is a table from the most recent derivatives data published by the Office of the Comptroller of the Currency (OCC), a regulator of national banks. (The chief of the OCC, Thomas Curry, sat across the table from President Obama on March 7 when the President made his false statement to the American people.) The table shows that as of March 31, 2016, the four banks that account for the vast majority of all derivatives in the U.S. had moved a mere sliver of their derivatives to exchanges. Out of JPMorgan Chase’s $52.9 trillion in derivatives, it had moved a mere 4.4 percent to exchanges while a stunning 95.6 percent remained in opaque Over-the-Counter contracts — private contracts between the bank and counterparties whose terms are often off limits to regulators.

The amount of derivatives that still had not moved to exchanges at the four banks ranged from a high of 95.6 at JPMorgan Chase to 94.3 percent at Citibank, to 87.8 percent at Goldman Sachs Bank USA and 90.6 percent at Bank of America. (The total dollar amount of derivatives is understated in this table since it shows the dollar amount at the insured bank only, not the total held at the bank holding company level. As we reported yesterday, Citigroup, at the bank holding company level, has now eclipsed JPMorgan Chase in total derivatives, holding 35 percent more than it did at the time it blew itself up in 2008.)

The mega Wall Street banks were also required under Dodd-Frank to move their derivatives out of the FDIC-insured banks they owned and onto the books of uninsured affiliates to prevent another forced bailout by taxpayers. That didn’t happen either and Citigroup was able to slip language into the December 2014 spending bill to completely repeal that provision of Dodd-Frank.

Reforming derivative practices on Wall Street was a critical component of the Dodd-Frank legislation. Toxic derivative trades had resulted in the largest failure in U.S. history of an insurance company during the 2008 crash. Large Wall Street banks had made the U.S. insurer, AIG, its guarantor (counterparty) on derivatives called credit default swaps — effectively gambles by Wall Street banks that sectors and companies were going to default on their debt. Because AIG did not have the funds to make good on those bets, the U.S. government took over AIG with a $185 billion taxpayer backstop. It was later revealed that major Wall Street and foreign banks and hedge funds received more than half of that bailout money ($93.2 billion) for the derivatives bets they had made with AIG and securities loan transactions. The firms were paid 100 cents on the dollar even though AIG was using taxpayer money.

As correctly depicted in the recent movie, “The Big Short,” the two largest rating agencies, Moody’s and Standard and Poor’s, competed for market share by doling out triple-A ratings on toxic bundles of subprime debt. The ratings were paid for by the very Wall Street banks that were issuing the debt. The ratings are still paid for by the Wall Street banks – an insane conflict of interest that Dodd-Frank failed to rein in. There is also still a gold-plated revolving door between employees moving from the ratings agencies to the Wall Street banks.

The official report from the Financial Crisis Inquiry Commission on the 2008 financial collapse had this to say about the ratings agencies’ role in the crash:

“We conclude the failures of credit rating agencies were essential cogs in the wheel of financial destruction. The three credit rating agencies were key enablers of the financial meltdown. The mortgage-related securities at the heart of the crisis could not have been marketed and sold without their seal of approval. Investors relied on them, often blindly. In some cases, they were obligated to use them, or regulatory capital standards were hinged on them. This crisis could not have happened without the rating agencies. Their ratings helped the market soar and their down-grades through 2007 and 2008 wreaked havoc across markets and firms.

“In our report, you will read about the breakdowns at Moody’s, examined by the Commission as a case study. From 2000 to 2007, Moody’s rated nearly 45,000 mortgage-related securities as triple-A. This compares with six private-sector companies in the United States that carried this coveted rating in early 2010. In 2006 alone, Moody’s put its triple-A stamp of approval on 30 mortgage-related securities every working day. The results were disastrous: 83% of the mortgage securities rated triple-A that year ultimately were downgraded. You will also read about the forces at work behind the breakdowns at Moody’s, including the flawed computer models, the pressure from financial firms that paid for the ratings, the relentless drive for market share, the lack of resources to do the job despite record profits, and the absence of meaningful public oversight. And you will see that without the active participation of the rating agencies, the market for mortgage-related securities could not have been what it became.”

There is no question that some corporate-funded Republicans can have a seismic negative impact on reforming Wall Street. Just look at what Rob Portman, a Republican from Ohio, has done to the Senate’s Permanent Subcommittee on Investigations. Under the former Chairmanship of Senator Carl Levin, Democrat from Michigan, the Subcommittee turned out unparalleled reports on financial crimes by Wall Street and foreign banks with such meticulous detail and subpoenaed documents that regulators and the Justice Department were forced to take action. Now the Subcommittee, under the Chairmanship of Portman, has become a corporate lapdog while portraying government as the problem. Portman’s two largest campaign donors between 2011 and 2016 are PACs, executives, or employees of Citigroup and Goldman Sachs, according to the Center for Responsive Politics.

But just because Republicans are often clueless about how to effectively regulate Wall Street, it doesn’t mean that they’re wrong about Dodd-Frank being an abject failure.

Related Article:

Dodd-Frank Versus Glass-Steagall: How Do They Compare?

Vast Majority of Derivatives Are Still Not On Exchanges, OCC Report , March 31, 2016