By Pam Martens: December 30, 2014

There Is a Wizard of Oz Quality to the Federal Reserve These Days

We are watching a collapse in industrial commodity prices, including crude oil. Yields on junk bonds (high yield debt) have risen dramatically. Investors have sought out the safe haven of U.S. Treasury notes, driving the yield lower as junk bond yields rise from an exit flight out of higher risk securities.

The above paragraph could just as well be describing December of 2008. Unfortunately, it’s also an apt description of where we find ourselves on December 30, 2014.

Aside from the irrationally exuberant U.S. stock market, there are two other serious mismatches that don’t compute between December of 2008, in the midst of the greatest financial collapse on Wall Street since the Great Depression, and December 2014. First, the publicly traded stocks of the largest Wall Street banks were in precipitous decline in late 2008, as they should have been, since rising levels of distressed debt and crashing industrial commodity prices mean the economy is weakening and banks will take a hit to earnings. Bizarrely, today, the share prices of Citigroup, Bank of America, and JPMorgan Chase are actually higher than where they started the year.

The second serious mismatch is the rhetoric coming out of the Federal Reserve. The statement released by the Federal Open Market Committee (FOMC) on December 16, 2008, accurately acknowledged the “declines in the prices of energy and other commodities” as a harbinger of “weaker prospects for economic activity.” Today, despite a stunning collapse in the prices of industrial commodities, the December 17, 2014 FOMC statement mentions only “declines in energy prices” and says nothing about the stark weakness in a broad range of other industrial commodities.

FOMC Release Date: December 16, 2008 (Excerpt)

“The Federal Open Market Committee decided today to establish a target range for the federal funds rate of 0 to 1/4 percent.

“Since the Committee’s last meeting, labor market conditions have deteriorated, and the available data indicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook for economic activity has weakened further.

“Meanwhile, inflationary pressures have diminished appreciably. In light of the declines in the prices of energy and other commodities and the weaker prospects for economic activity, the Committee expects inflation to moderate further in coming quarters.

“The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time.”

FOMC Release Date: December 17, 2014 (Excerpt)

“Information received since the Federal Open Market Committee met in October suggests that economic activity is expanding at a moderate pace. Labor market conditions improved further, with solid job gains and a lower unemployment rate. On balance, a range of labor market indicators suggests that underutilization of labor resources continues to diminish. Household spending is rising moderately and business fixed investment is advancing, while the recovery in the housing sector remains slow. Inflation has continued to run below the Committee’s longer-run objective, partly reflecting declines in energy prices. Market-based measures of inflation compensation have declined somewhat further; survey-based measures of longer-term inflation expectations have remained stable.

“Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators moving toward levels the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for economic activity and the labor market as nearly balanced. The Committee expects inflation to rise gradually toward 2 percent as the labor market improves further and the transitory effects of lower energy prices and other factors dissipate. The Committee continues to monitor inflation developments closely.

“To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate.”

Now notice what has remained the same for the past six consecutive years: the Federal Funds rate has remained targeted at “0 to 1/4 percent” by the Federal Reserve. This is what economists refer to as ZIRP – Zero Interest Rate Policy. Despite the Fed holding rates this low for all this time, the economy has not built up a head of steam strong enough to materially boost wage growth or prevent a recurring collapse in industrial commodity prices. And yet, the Fed has been able to keep the public and investors focused all year on just when it is going to raise interest rates in 2015 to keep the economy from overheating. (There is a decidedly Wizard of Oz feel to the Fed these days.)

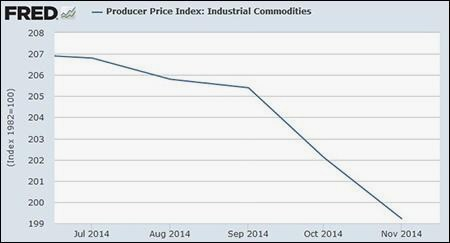

The takeaway from the following chart is as simple as this: overheating economies are completely, incontrovertibly not associated with collapsing industrial commodity prices. Collapsing industrial commodity prices are consistent, however, with the following paragraph that appeared at Bloomberg News yesterday morning:

“Emerging-market distressed debt losses are the worst this month since the global financial crisis. Bank of America Merrill Lynch’s Distressed Emerging Markets Corporate Plus Index fell 13.4 percent through Dec. 26, set for its worst performance since October 2008, as a tumble in the price of oil sparked a currency crisis in Russia. That brought this year’s decline to 19.7 percent, the most in six years. High-yield distressed securities in the U.S. lost 8 percent, the indexes show.”

Producer Price Index — Industrial Commodities, July through November 2014 (Graph courtesy of the Federal Reserve Bank of St. Louis; data from Bureau of Labor Statistics)