By Pam Martens and Russ Martens: March 16, 2021 ~

David Solomon, Chairman and CEO, Goldman Sachs

Less than five months ago, Goldman Sachs and its Malaysian subsidiary were criminally charged by the U.S. Department of Justice “for a sweeping international corruption scheme, conspiring to avail itself of more than $1.6 billion in bribes to multiple high-level government officials across several countries so that the company could reap hundreds of millions of dollars in fees.” The case has become infamously known as the 1MDB scandal, named after the Malaysian sovereign wealth fund that was ripped off.

Goldman Sachs admitted to the charges and paid a criminal penalty and disgorgement of over $2.9 billion to settle the charges with the Department of Justice. That sum was on top of the $2.5 billion in cash it paid to settle with the government of Malaysia.

Stripping shareholders of $5.4 billion of their capital for criminal conduct in the midst of the worst pandemic in a century might have humbled a lesser institution and encouraged its Chairman and CEO, David Solomon, to stay out of the spotlight.

Unfortunately for Solomon, however, Goldman Sachs has just come into the cross-hairs of Senator Sherrod Brown, Chair of the Senate Banking Committee, and his feisty colleague on that Committee, Senator Elizabeth Warren.

The Senators sent Solomon a letter on Friday demanding answers to a series of questions surrounding Goldman’s decision to take advantage of a temporary, weakened capital requirement by federal regulators that was sold to the public as allowing banks to continue to make loans to businesses during the pandemic without being hamstrung by capital restraints.

The Senators wanted to know, among numerous other concerns, if Goldman had received a waiver from regulators to continue its dividend distributions to shareholders (in other words, depleting its capital) throughout the pandemic while also availing itself of the weakened capital rule. Goldman paid $1.25 per share as a cash dividend each quarter throughout 2020. Its next declared dividend payment in the same amount is scheduled for payment on March 30.

According to Goldman’s most recent SEC filing, it had 345,794,361 common shares outstanding as of February 5, 2021. Using five quarterly dividends of $1.25 per share, by March 30 of this year it will have paid out approximately $2.16 billion in cash to shareholders since its March 30 dividend payment in 2020.

Add that $2.16 billion to the $5.4 billion that Goldman paid to settle claims related to its 1MDB bribery scandal and we reach the sum of $7.56 billion that has gone poof from Goldman’s capital since last March. S&P Global reported on January 19 that Goldman’s CFO, Stephen Scherr, announced on an earnings call with analysts on that date that Goldman planned to buy back approximately $1.9 billion of its stock in the first quarter of 2021. Since there’s only 15 days left in this quarter, one might assume most of that money has been spent.

The capital rule in question is the Supplementary Leverage Ratio (SLR) which impacts only the largest banks and requires that they have capital equal to three percent of their total on-balance sheet assets and off-balance sheet exposures. The weakened rule allowed the banks to exclude holdings of U.S. Treasury securities and their deposits at Federal Reserve banks from their calculation of the SLR. The temporary rule was set to expire on March 31 but lobbyists for the biggest Wall Street banks have been lobbying to have the rule extended.

The Senators indicate in the letter that they are singling out Goldman Sachs for this reason:

“To our knowledge, Goldman Bank is the only depository institution that opted into these weakened capital requirements whose holding company continued to reduce its capital by paying dividends. We believe your organization has a unique perspective with regard to these rules.”

There must be some type of subtlety that we’re missing on the words “opted into,” because two other Wall Street mega banks which, like Goldman, have massive off-balance sheet exposure to derivatives, also took advantage of the weakened rule and continued to pay out their regular cash dividends throughout 2020. Those mega banks are Citigroup and JPMorgan Chase.

Citigroup reported the following in its most recent 10-K filing with the SEC:

“Temporary Supplementary Leverage ratio (SLR) relief for bank holding companies, commencing in the second quarter of 2020, allowing Citigroup to temporarily expand its balance sheet by excluding U.S. Treasury securities and deposits with the FRB from the SLR denominator. Citigroup’s reported Supplementary Leverage ratio of 7.00% benefited by 109 basis points during the fourth quarter of 2020 as a result of the temporary relief. Excluding the temporary relief, Citigroup’s Supplementary Leverage ratio would have been 5.91%….”

JPMorgan Chase wrote this in its most recent 10-K filing with the SEC:

“The Firm’s SLR was 6.9%. The SLR reflects the temporary exclusions of U.S. Treasury securities and deposits at Federal Reserve Banks, as required by the Federal Reserve’s interim final rule issued on April 1, 2020. The Firm’s SLR excluding the temporary relief was 5.8%.”

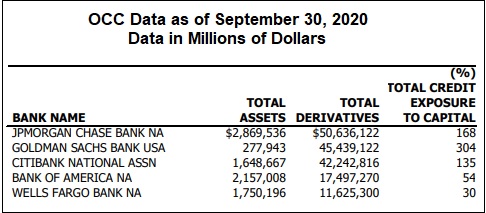

According to the Office of the Comptroller of the Currency’s most recent quarterly report on derivatives for the quarter ending September 30, 2020, the federally insured banking units of JPMorgan Chase, Goldman and Citigroup’s Citibank held the following amounts of notional derivatives (face amount): $50.6 trillion; $45.4 trillion; and $42.2 trillion, respectively. The number, however, that is a screaming red flag for Goldman’s federally-insured bank known as Goldman Sachs Bank USA is that its credit exposure to its capital stands at 304 percent. (See chart below.)

Following the financial crash of 2008, Phil Angelides, the Chair of the Financial Crisis Inquiry Commission (FCIC), had this to say on June 30, 2010 at a hearing convened specifically to examine “The Role of Derivatives in the Financial Crisis”:

“I must say that despite 30 years in housing, finance, and investment — in both the public and private sectors — I had little appreciation of the tremendous leverage, risk, and speculation that was growing in the dark world of derivatives. Neither, apparently, did the captains of finance nor our leaders in Washington.

“The sheer size of the derivatives market is as stunning as its growth. The notional value of over the-counter derivatives grew from $88 trillion in 1999 to $684 trillion in 2008. That’s more than ten times the size of the Gross Domestic Product of all nations. Credit derivatives grew from less than a trillion dollars at the beginning of this decade to a peak of $58 trillion in 2007. These derivatives multiplied throughout our financial markets, unseen and unregulated…

“In June 2008, Goldman’s derivative book had a stunning notional value of $53 trillion.”

Well, guess what. Goldman’s derivatives book, almost 13 years and two financial crises later, still stands at $45.4 trillion. And it is highly likely that it’s the counterparties that are on the other side of those derivative trades that are concerning Senators Brown and Warren. For a peek at what Goldman’s counterparty exposure might look like today, below is a graph released by the Financial Crisis Inquiry Commission after the 2008 crash. If this chart suggests the likelihood of systemic contagion in the next financial crisis, you’re thinking along the right lines.

Source: Financial Crisis Inquiry Commission

On top of these concerns, there is also this: Wall Street Banks Are Dangerously Evading U.S. Derivatives Rules by Making Trades at Foreign Subsidiaries.

This is not the first time that Senators Brown and Warren have expressed concerns about the weakened SLR capital rule. They sent a letter to federal regulators on June 19 of last year, urging them to reverse this weakened rule, explaining as follows:

“To the families who were affected by the last financial crisis, capital requirements were not some abstract ratio found in the pages of the Federal Register: they represented the difference between families and workers losing their homes, jobs, and livelihoods. The same is true as the country faces a new economic crisis caused by the COVID-19 pandemic. You should reverse this rule and immediately take action to preserve capital at financial institutions to ensure that these institutions are stable and can provide the needed assistance to their customers and to the economy as a whole.”