![]()

By Pam Martens and Russ Martens: September 7, 2023 ~

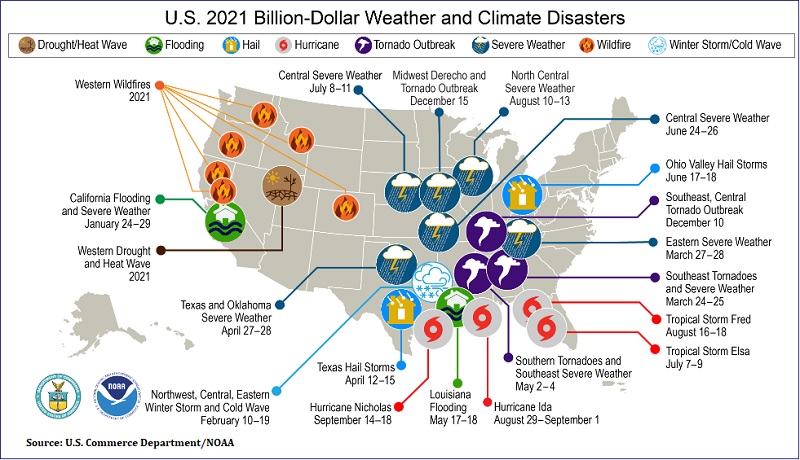

As climate-related disasters in the United States have taken on the look and feel of sci-fi films, the U.S. Senate Banking Committee will hold a hearing this morning on the dramatic impact this is having on the ability of homeowners to find and keep affordable homeowners insurance policies.

As a backdrop to the hearing, four days ago Jacob Bogage, a business reporter at the Washington Post, shared these revelations with readers:

“At least five large U.S. property insurers — including Allstate, American Family, Nationwide, Erie Insurance Group and Berkshire Hathaway — have told regulators that extreme weather patterns caused by climate change have led them to stop writing coverages in some regions, exclude protections from various weather events and raise monthly premiums and deductibles.

“Major insurers say they will cut out damage caused by hurricanes, wind and hail from policies underwriting property along coastlines and in wildfire country, according to a voluntary survey conducted by the National Association of Insurance Commissioners, a group of state officials who regulate rates and policy forms.”

Translating these actions into the underlying dollars and cents, the Washington Post reports:

“U.S. insurers have disbursed $295.8 billion in natural disaster claims over the past three years, according to international risk management firm Aon. That’s a record for a three-year period, according to the American Property Casualty Insurance Association.

“Natural catastrophes in the first six months of 2023 in the United States caused $40 billion in insured losses, the third costliest first-half on record, Aon found.”

The Senate Banking Committee hearing will take testimony from three witnesses: Douglas Heller, Director of Insurance at the Consumer Federation of America; Michelle Norris, Executive Vice President of External Affairs and Strategic Partnerships at National Church Residences; and Jerry Theodorou, Policy Director for Finance, Insurance and Trade at the R Street Institute.

We have reviewed the written testimony of the witnesses and the reality is that homeowners are facing – and will continue to face – serious headwinds in obtaining affordable homeowners insurance that covers the greatest perils that they face.

Douglas Heller of the Consumer Federation of America provided these details in his written remarks:

“In 2022, Americans paid $125 billion for homeowners insurance, according to the National Association of Insurance Commissioners (NAIC). That is 9.6% more than 2021 and 35%, or $32.6 billion, more than just five years prior. After accounting for the estimated increase to the number of insured houses in 2022 compared with 2017, the increase in home insurance premiums rose about 40% faster than inflation as measured by the Consumer Price Index.”

While costs for protecting one’s home have skyrocketed for tens of millions of Americans, coverage has also been hollowed out. Heller notes the following:

“Even when insurers continue to sell coverage, they are slashing the value of the protection, hollowing it out, and increasing the deductibles homeowners face such that consumers are forced to retain more and more of the catastrophic risk associated with owning a home. It means that even for homeowners who can meet their lenders’ requirements for coverage, their insurance policies are not meeting what the family relies on to protect their most valuable asset.”

Michelle Norris of National Church Residences, which provides affordable housing to senior citizens (“who earn on average just $15,000 a year”) included in her written testimony that “As of the first quarter of 2023, property insurance rates in the United States have increased for 22 consecutive quarters.”

Jerry Theodorou, of the R Street Institute, a free market think tank, was on hand to warn against government interventions, arguing that fostering competition will take care of the problem. (Mr. Theodorou, one suspects, has not studied the above maps.) Theodorou, did, however, cite one government intervention in Florida that was clearly needed. He wrote in his testimony:

“Prior to March 24, 2023, when comprehensive tort reform was signed into law in Florida, the homeowners insurance market was plagued by out-of-control meritless litigation. The magnitude of the litigation abuse problem is starkly visible in the statistic that Florida accounts for 9 percent of the nation’s homeowners insurance policies, but is responsible for 79 percent of the entire country’s homeowner insurance litigation. The tort reform measures are expected to restore the Florida market to a healthier position. However, the improvements will take time to materialize into rate reductions because in the days prior to Florida Governor Ron DeSantis signing tort reform into law, Florida plaintiff attorneys filed approximately 280,000 property insurance lawsuits — an action that will cause severe delays in normal court functioning.”

The Senate Banking Committee hearing can be watched live at this link, beginning at 10:00 a.m. today. You can watch it as an archived video anytime thereafter.