By Pam Martens and Russ Martens: August 30, 2017

The Consumer Financial Protection Bureau (CFPB), the Federal agency created after the 2008 financial crash to protect consumers from predator banks, has issued a warning on what smells like the latest financial blood sport: bank employees selling reverse mortgages to seniors under the guise that it will allow them to reap a larger Social Security benefit down the road by delaying Social Security payments to a later age.

Reading through the CFPB report that accompanied the warning, it reminded us of how the tobacco industry had secretly targeted young people as “replacement smokers” while intentionally hiding the deadly effects of smoking from the public.

The CFPB report advises that “nearly five million homeowners will turn age 62 by 2020.” That’s the earliest age at which one can collect Social Security retirement benefits as well as the earliest age to apply for a reverse mortgage. That creates a big pool of potential new customers to whom banks can peddle reverse mortgages.

The problems with this marketing strategy are multiple explains the report:

“The CFPB examined different scenarios and found that, in general, the reverse mortgage loan costs exceed the cumulative increase in Social Security that homeowners would receive in their lifetime by delaying Social Security benefits. Furthermore, using this strategy will likely diminish the amount of home equity available to borrowers later in life. As a result of the diminished equity, borrowers that seek to sell their homes after using this strategy may have limited options for moving to a new location or handling a financial shock.”

It’s understandable why financial predators would want to tap into the home equity in the homes of seniors. According to the CFPB report, it’s where the largest single pool of wealth resides for people 65 and older. As of 2015, according to the report, “80 percent of consumers 65 and older owned their homes– 30 percent of them with a mortgage and 70 percent without.”

The report explains how the reverse mortgage works:

“A homeowner that borrows a reverse mortgage loan to delay collecting Social Security benefits receives loan proceeds secured by the equity in their home during the period of the delay. In doing so, they assume debt for the principal loan amount, as well as for interest, mortgage insurance premiums (MIP), and monthly servicing fees, which are added to the principal every month. In addition, origination and closing costs are often added to the loan balance since most consumers choose to finance these costs using the reverse mortgage proceeds. Over time, the balance of the loan increases as a result of compounding interest and MIP, and fees. The increasing loan balance will slowly reduce the available home equity to homeowners who wish to sell and move.”

Compounding interest on your own money is a winning strategy for building wealth. Compounding interest on debt and/or fees is a very bad thing. The CFPB report puts the numbers into perspective:

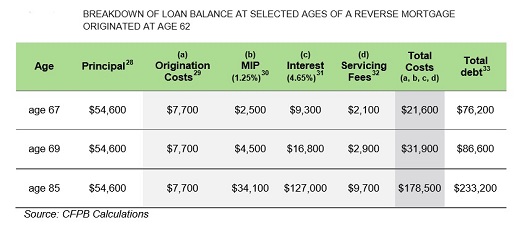

“Based on a study of reverse mortgage loans issued before 2006, the average borrower holds a reverse mortgage for seven years. In seven years, when the borrower turns 69 and terminates the loan, the reverse mortgage loan costs will be $31,900, approximately $2,300 more than the lifetime amount of money gained from an increased Social Security benefit if the consumer lives to age 85 ($29,640).”

Now look at the stunning impact of the debt/fees compounding over a longer time period:

“By age 85, approximately the average life expectancy of a 62 year old, the reverse mortgage loan costs will be $178,000, approximately $149,000 more than the lifetime amount of money gained from an increased Social Security benefit if the consumer lives to age 85 ($29,640).” (See chart above.)

The CFPB report also offers this example of how the equity is stripped from the home as a result of the debt/fees compounding:

“Consider the following example for a typical 62-year-old homeowner with a home worth $175,000. Assume the home appreciates in value at a rate of 4 percent per year and that the homeowner borrows a reverse mortgage with an interest rate of 5.9 percent. At age 67, this homeowner will have a home valued approximately at $212,914, and at age 85, the home will be valued at $431,325.38. At age 67, the homeowner who borrowed $54,600 from a reverse mortgage to delay collecting Social Security will have only 64 percent of the total value of his home available if he decides to sell the home and move. By age 85, this homeowner will have only 46 percent of his home value available as equity.”

The CFPB report offers a much more prudent path for seniors who want to collect a larger Social Security retirement benefit: keep working past age 62. The report notes:

“The extra years of work often provide people more time to save for retirement and pay off debts. The extra years of work may also result in an increase in Social Security benefits—separate from the increase that arises from deferring the start of benefits—by replacing years with low or no earnings from the person’s earnings record.”

This bold report that again takes on the wealth-stripping techniques of the financial industry is just one more example of why the CFPB and its Director, Richard Cordray, are under a concerted congressional assault to silence their courageous voices. The public must be vigilant to prevent that from happening.