By Pam Martens and Russ Martens: January 27, 2022 ~

The last thing a volatile stock market needs right now is more surprises from the dark corners of Wall Street. Unfortunately, we can guarantee you that more surprises are coming in the way of uncleared derivatives blowing up on the balance sheets of publicly-traded corporations.

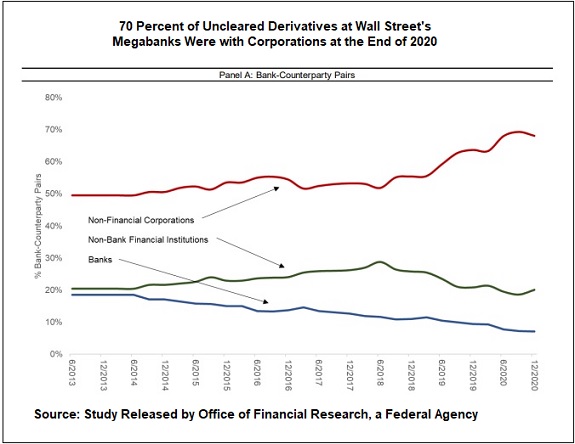

How do we know this? The information in the chart above comes from a study quietly released last July by the Office of Financial Research (OFR). That’s the federal agency that provides research to bank regulators to prevent systemic financial contagion from taking down the Wall Street megabanks and the U.S. economy in another replay of 2008.

What the study actually shows, however, is that neither Congress nor bank regulators have done anything meaningful to prevent derivatives from once again blowing up the world’s largest economy. Instead, the watchdogs have simply allowed a rearrangement of the deck shares on the Titanic. While Wall Street megabanks previously concentrated their counterparty risk with each other and foreign global banks, necessitating that the Fed had to bail out dodgy banks on foreign shores, they’ve now shifted their counterparty risk to corporations.

The study is silent on the names of these corporations. We contacted the lead author of the study yesterday asking for the industries these corporations were concentrated in and he chose to remain silent. The study is also silent on the names of the megabanks, but we already know from the quarterly reports from the Office of the Comptroller of the Currency that JPMorgan Chase, Goldman Sachs, Citigroup, Bank of America and Morgan Stanley control over 80 percent of all derivatives at all bank holding companies in America.

According to the OFR study:

“Compositional breakdowns between bank, non-bank financial and non-financial corporate counterparties in OTC derivative markets has dramatically changed since the financial crisis. Publicly available data indicate that the share of financial firms in aggregate bank exposures has decreased while the share of non-financial corporations has increased….”

Corporations on the hook for losses as counterparties to the Wall Street megabanks’ derivative trades didn’t just “increase.” It skyrocketed according to the red line in the above chart. And it skyrocketed in the most dangerous area of derivatives – those bilateral trades that are secret contracts between the bank and the corporation and are not cleared on any central clearinghouse. The OFR study confirms that there is no sunshine on these derivative trades, writing that they contributed to systemic risks during the 2008 financial crisis and “remain an area of limited visibility for regulators and policymakers.”

The OFR study puts the net credit exposure of these corporations to derivatives at more than $700 billion as of June 2020. And there is good reason to suspect that these are not plain-vanilla interest rate swaps. Those swaps are typically centrally-cleared. It’s the murkier derivatives like credit default swaps that remain uncleared at central clearinghouses and that’s what the OFR study is looking at.

When a century-old conservative corporation has to report a big loss from a stupid derivatives trade with a big Wall Street bank – which always has an informational advantage on who’s going to lose on the trade (think Goldman Sachs shorting their own subprime debt bombs) – it harms the corporation’s reputation and share price. Investors don’t know how many more secret derivative trades are hiding out on the corporation’s balance sheet and just how stupid management is when it comes to entering into derivative contracts with Wall Street.

One of the biggest embarrassments along these lines came in 1994 when Procter & Gamble, the maker of century-old household product brands like Ivory soap, announced it had lost more than $100 million from derivatives sold to it by Bankers Trust. Procter & Gamble took Bankers Trust to court, charging that Bankers Trust had lied to it and never revealed the magnitude of the losses it could suffer from the derivatives contract.

In the same year, Gibson Greetings, the greeting card and wrapping paper company, also announced losses on derivatives sold to it by Bankers Trust. A tape recording from inside Bankers Trust revealed how executives were strategizing on how to lie to Gibson Greetings on the extent of their losses. That case also went to court.

The Securities and Exchange Commission brought charges against both Bankers Trust and Gibson Greetings over the derivatives. In the case against Bankers Trust the SEC wrote:

“During the period from October 1992 to March 1994, BT Securities’ [Bankers Trust Securities] representatives misled Gibson about the value of the company’s derivatives positions by providing Gibson with values that significantly understated the magnitude of Gibson’s losses. As a result, Gibson remained unaware of the actual extent of its losses from derivatives transactions and continued to purchase derivatives from BT Securities. In addition, the valuations provided by BT Securities’ representatives caused Gibson to make material understatements of the company’s unrealized losses from derivatives transactions in its 1992 and 1993 notes to financial statements filed with the Commission.”

Just how many other corporations lost money in derivatives that year and kept their mouths shut will likely never be known. But what is known is that in the same year of 1994 Merrill Lynch had managed to sell enough dodgy derivatives and other securities to Orange County, California that it had to file for bankruptcy, resulting in tens of thousands of teachers, firefighters and other public workers losing their jobs.

And yet, here we are in 2022 with the news that Wall Street megabanks have once again moved their counterparty risk in derivatives to the balance sheets of corporations receiving no attention from the Senate Banking or House Financial Services Committees. (We’ll be sending this article along to them today, as well as to the SEC.)

It’s also time for the authors of that OFR study to fill in the many blanks they left in their report – beginning with the names of the corporations.